How to Get Commercial Hazmat Truck Insurance

Transporting hazardous materials requires specialized commercial hazmat truck insurance that goes far beyond standard trucking coverage. The stakes are higher, regulations are stricter, and one accident can cost millions.

We at Insurance Brokers of Arizona® see trucking companies struggle with complex federal requirements and sky-high premiums. The right coverage protects your business while meeting DOT mandates.

What Are the Legal Requirements for Hazmat Truck Insurance?

Federal Coverage Minimums You Cannot Ignore

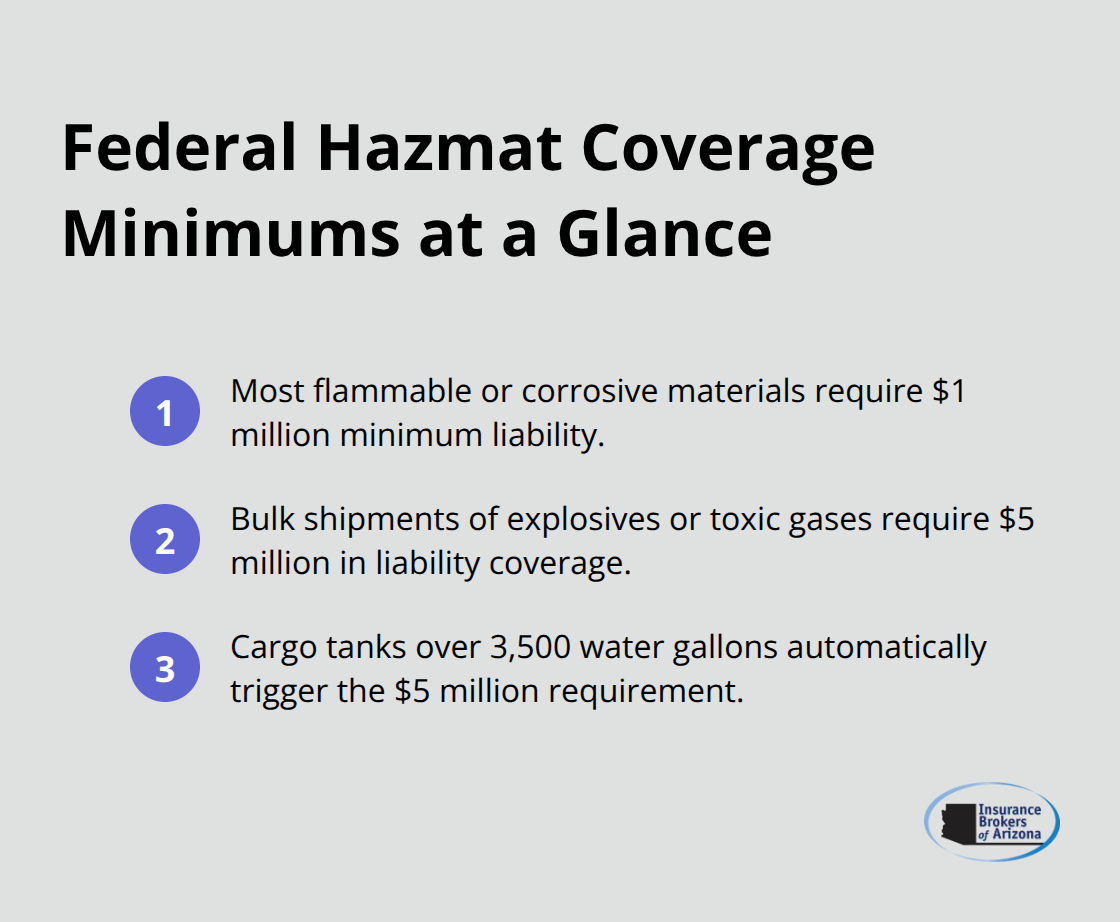

The Federal Motor Carrier Safety Administration sets specific insurance amounts based on hazardous material classifications. Most flammable or corrosive materials require $1 million minimum coverage, while bulk shipments of explosives or toxic gases demand $5 million. Cargo tanks that exceed 3,500 water gallons capacity automatically trigger the $5 million requirement, regardless of material type.

These amounts represent absolute minimums. Actual claims from hazmat incidents routinely exceed these thresholds by substantial margins (often reaching tens of millions in environmental cleanup costs).

FMCSA Documentation That Carriers Must Submit

Your insurance provider must file Form BMC-91 or BMC-91X directly with the FMCSA to validate your coverage. The MCS-90 endorsement remains non-negotiable – carriers who miss this single document during an audit face immediate operating authority suspension.

Many carriers assume their broker handles these filings automatically, but verification remains your responsibility. The FMCSA database updates can lag by several weeks, so submit documentation at least 45 days before you need active coverage.

State Requirements That Exceed Federal Standards

State requirements often exceed federal minimums, particularly in California where environmental regulations push coverage needs higher. Texas and Florida impose additional documentation requirements that many out-of-state carriers overlook until they face compliance violations.

Pennsylvania requires additional pollution liability coverage for certain hazmat classes (beyond federal mandates). These state-specific requirements can significantly impact your total insurance costs and compliance timeline.

Understanding these complex requirements sets the foundation for the next critical step: identifying the factors that will determine your actual premium costs.

What Drives Your Hazmat Insurance Premiums

Driver Records Control Your Insurance Costs

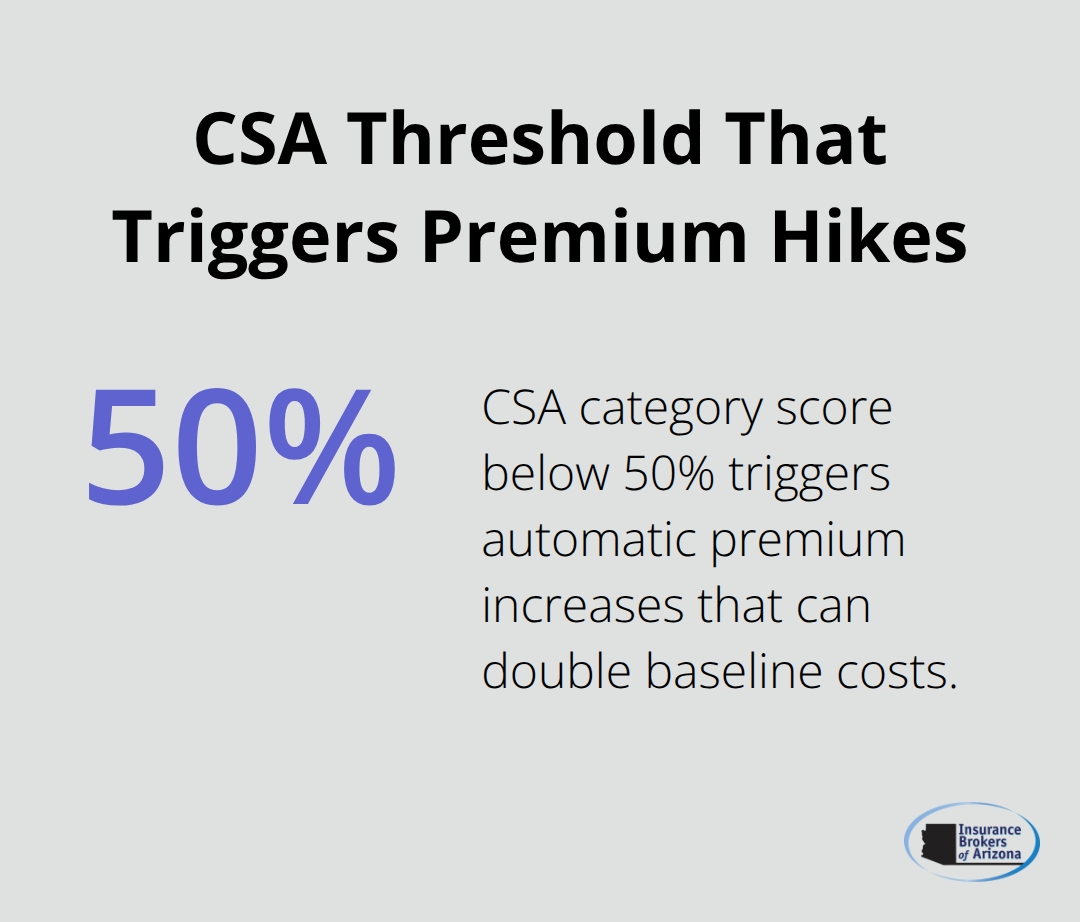

Driver experience and safety records directly control your hazmat insurance costs more than any other factor. Carriers with drivers who maintain clean records for three consecutive years see premium reductions of 10-30%, while a single hazmat-related accident increases rates by 20-50% according to industry data. The Compliance, Safety, Accountability score from FMCSA audits becomes your foundation for rates – scores below 50% in any category trigger automatic premium increases that can double your baseline costs.

Hazmat drivers need specialized training beyond standard CDL requirements, and insurers reward comprehensive safety programs with measurable discounts. Companies that invest in collision avoidance systems, telematics monitoring, and dash cam technology typically receive 5-15% premium reductions. The key lies in documentation – insurers want proof of ongoing safety investments, not just initial training certificates.

Material Classification Determines Your Risk Tier

The nine DOT hazmat classes create distinct insurance tiers that vary dramatically in cost. Class 1 explosives command the highest premiums, often 40-60% above baseline rates, while Class 9 miscellaneous dangerous goods represent the most affordable hazmat category. Bulk liquid transportation in cargo tanks that exceed 3,500 gallons automatically pushes you into the $5 million coverage requirement, regardless of material type.

Carriers who transport multiple hazmat classes face complex underwriting that examines your worst-case scenario materials. Insurers calculate premiums based on your highest-risk cargo, even if you only transport it occasionally.

Geographic Routes Add Premium Complexity

Routes through high-density population areas or environmentally sensitive zones add another 15-25% to your base premium. California and Texas routes show the steepest increases due to strict state regulations and higher claim frequencies (with California premiums averaging $18,500-$28,000 annually). Urban areas generally cost more than rural routes because of increased accident risks and higher property values.

Weather patterns and seasonal hazards also impact your rates. Routes through areas prone to severe weather conditions or natural disasters face additional surcharges that can fluctuate throughout the year.

These premium factors work together to create your final insurance costs, but smart carriers know that choosing the right insurance provider can significantly impact both rates and coverage quality.

Where Should You Shop for Hazmat Truck Insurance

Target Specialized Hazmat Insurance Providers Only

Standard commercial truckers insurers often lack the expertise and appetite for hazmat risks, which leads to coverage gaps and inflated premiums. Progressive Commercial, CNA, and Great West Casualty specialize in hazmat operations and understand the unique regulatory landscape that general insurers avoid. These carriers maintain dedicated teams who evaluate hazmat risks properly instead of they apply generic formulas that penalize specialized operations.

Regional insurers with strong hazmat programs often provide better service and competitive rates compared to national carriers who view hazmat as a secondary market. The key lies in you find insurers with A-rated financial strength from AM Best – anything below A- rating puts your claims payments at risk during major incidents.

Demand Comprehensive Coverage Comparisons

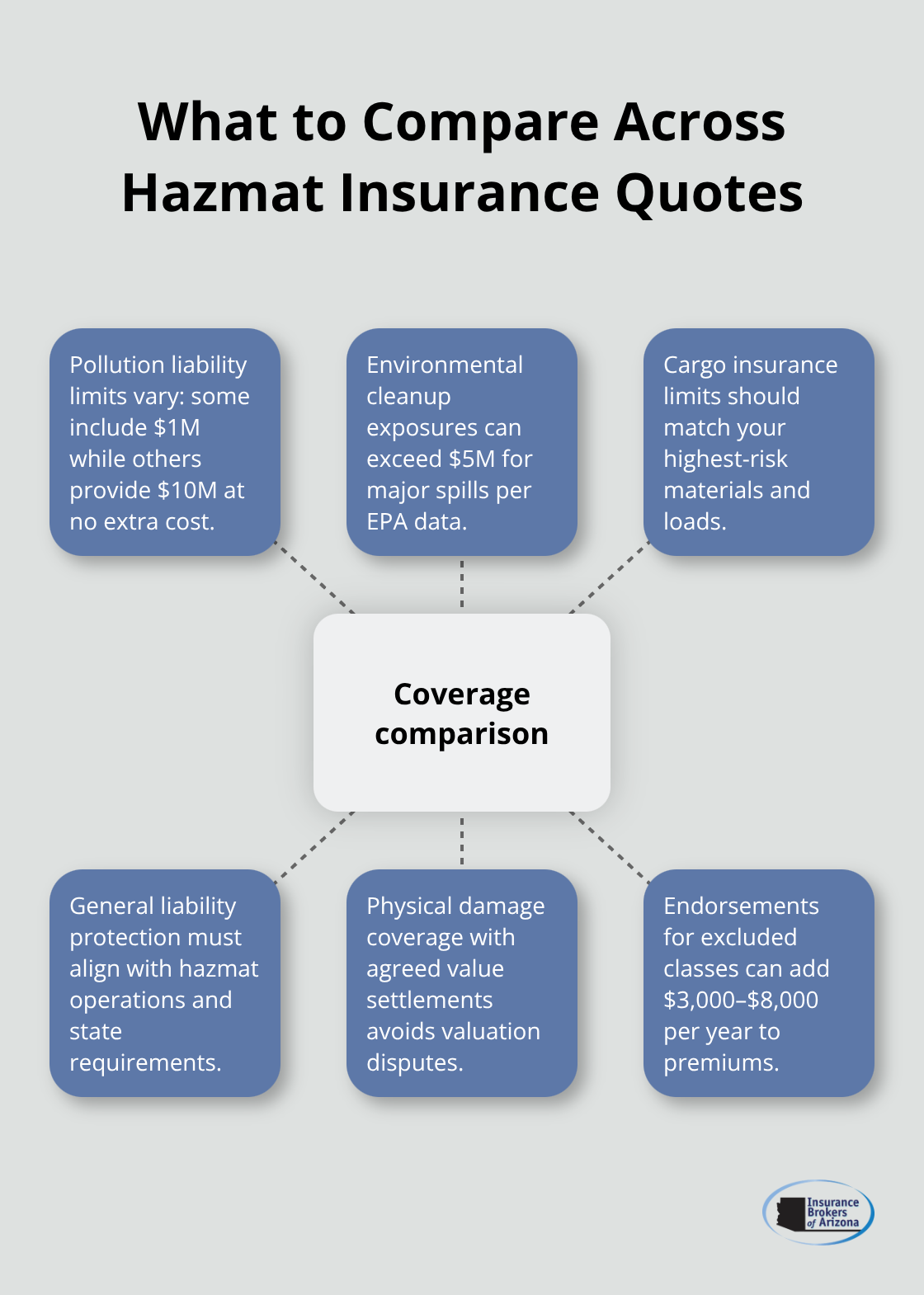

Premium quotes mean nothing without identical coverage specifications across providers. Pollution liability limits vary dramatically between insurers, with some that offer $1 million standard coverage while others provide $10 million without additional cost. Environmental cleanup costs from major spills routinely exceed $5 million according to EPA data (which makes higher pollution limits essential rather than optional).

Request detailed coverage comparisons that include cargo insurance limits, general liability protection, and physical damage coverage with agreed value settlements. Many carriers exclude certain hazmat classes from standard policies, which requires expensive endorsements that can add $3,000-$8,000 annually to your premium.

Verify Claims Response Speed and Expertise

Hazmat claims require immediate response capabilities that standard adjusters cannot provide. Insurers with dedicated hazmat claims teams resolve incidents 40-60% faster than those who use general commercial adjusters according to industry benchmarks. Ask potential providers about their average hazmat claim settlement timeframes and emergency response protocols – delays in hazmat incidents create exponentially higher costs and regulatory penalties.

Review actual claim examples from your potential insurer, and focus on environmental incidents similar to your cargo types. Insurers who handle hazmat claims poorly often face regulatory sanctions that can impact your authority during the claims process (which creates additional complications for your operations). Getting expert answers to your commercial truck insurance questions helps you make informed decisions during the selection process.

Final Thoughts

Commercial hazmat truck insurance demands precise planning and specialized expertise. Calculate your exact federal coverage requirements based on your specific hazmat classes and cargo tank capacities. Document all state-specific requirements for your territories, as these often exceed federal minimums and create compliance gaps.

Focus exclusively on specialized hazmat insurers with A-rated financial strength and proven claims expertise. Generic commercial trucking policies create dangerous coverage gaps that expose your operation to regulatory violations and catastrophic financial losses. Request detailed pollution liability comparisons and verify emergency response protocols before you make your final selection.

We at Insurance Brokers of Arizona® help trucking companies secure comprehensive coverage while meeting strict DOT compliance standards (through our network of specialized carriers). Gather your current safety records, hazmat classifications, and route documentation now. Contact Insurance Brokers of Arizona® to review your specific requirements and receive competitive quotes from specialized hazmat insurers.