At Insurance Brokers of Arizona®, we understand the importance of protecting your business assets. Hazard insurance for commercial property is a critical component of any comprehensive risk management strategy.

This coverage safeguards your property against a wide range of potential threats, from natural disasters to human-caused incidents. In this post, we’ll explore the key facts you need to know about hazard insurance for commercial properties, helping you make informed decisions to protect your business investments.

What Is Hazard Insurance for Commercial Property?

Definition and Purpose

Hazard insurance for commercial property protects your business assets against physical damage from specific perils. These perils typically include fire, windstorms, hail, explosions, and theft. The primary purpose of this insurance is to provide financial protection for your business in case of property damage or loss. Without adequate coverage, a single catastrophic event could potentially bankrupt your company. For example, the Federal Emergency Management Agency (FEMA) reports that 40% of businesses never reopen after a disaster, and another 25% fail within one year. Hazard insurance mitigates these risks by covering repair or replacement costs.

Hazard vs. Property Insurance

While often used interchangeably, hazard insurance and property insurance have subtle differences. Hazard insurance specifically focuses on damage from named perils, while property insurance is a broader term that may include additional coverages (like business interruption or liability protection). Many insurance professionals recommend a comprehensive commercial property policy that includes hazard coverage along with other essential protections.

Types of Commercial Properties Covered

Hazard insurance can protect a wide range of commercial properties, including:

- Office buildings

- Retail stores

- Warehouses

- Manufacturing facilities

- Apartment complexes

- Hotels

- Restaurants

- Medical facilities

The specific type of property you own or lease will impact the kind of hazard insurance you need. For instance, a warehouse storing valuable inventory might require higher coverage limits than a small office space. Similarly, a beachfront hotel in a hurricane-prone area would need different coverage than an inland retail store.

Tailoring Coverage to Your Needs

It’s important to work with an experienced insurance broker who understands the unique risks associated with your specific type of commercial property. They can help you identify potential gaps in coverage and ensure you have the right protection in place. Insurance Brokers of Arizona®, for example, offers personalized insurance products for businesses and can help tailor coverage to your specific needs.

As we move forward, let’s explore the common hazards covered in commercial property insurance and how they can affect your business.

What Hazards Does Commercial Property Insurance Cover?

Commercial property insurance protects businesses from a wide range of potential threats. This coverage can make the difference between a business recovering from a disaster or facing financial ruin.

Fire and Smoke Damage

Fire remains one of the most destructive forces for commercial properties. The National Fire Protection Association reports that U.S. fire departments responded to an estimated 96,800 fires in non-residential properties in 2021, resulting in $2.7 billion in direct property damage. Commercial property insurance typically covers damage from fires, including smoke damage (which can be extensive even if flames don’t reach certain areas of the building).

Weather-Related Perils

Severe weather events have become increasingly common and costly. The National Oceanic and Atmospheric Administration (NOAA) reported 18 weather and climate disaster events with losses exceeding $1 billion each in the United States in 2022. Commercial property insurance usually covers damage from wind, hail, and storms. However, it’s important to understand the specifics of your policy, as some may have limitations or exclusions for certain types of weather events.

Water Damage and Flooding

Water damage can result from various sources, such as burst pipes, roof leaks, or backed-up sewers. Most commercial property policies cover water damage from internal sources, but flood damage from external sources often requires separate coverage. The Federal Emergency Management Agency (FEMA) states that just one inch of floodwater can cause up to $25,000 in damage. Businesses in flood-prone areas should consider additional flood insurance.

Theft and Vandalism

Property crimes significantly impact businesses. The FBI’s Uniform Crime Reporting (UCR) Program estimated that in 2019, burglaries of non-residential properties resulted in $1.4 billion in property losses. Commercial property insurance typically covers losses from theft and vandalism, including damage to the building and stolen inventory or equipment.

Natural Disasters

Coverage for natural disasters like earthquakes and hurricanes can vary significantly between policies. In earthquake-prone regions like California, separate earthquake insurance is often necessary. Similarly, businesses in hurricane-prone areas may need additional windstorm coverage. The Insurance Information Institute reports that insured losses from natural catastrophes in the U.S. reached $92 billion in 2022, highlighting the importance of comprehensive disaster coverage.

To ensure your policy addresses all potential hazards relevant to your business and location, work with an experienced insurance broker. They can help tailor coverage to meet the unique needs of your business and protect against a wide array of potential threats. As we move forward, let’s examine the factors that affect hazard insurance premiums for commercial properties.

What Impacts Your Hazard Insurance Premiums?

Location Influences Risk Assessment

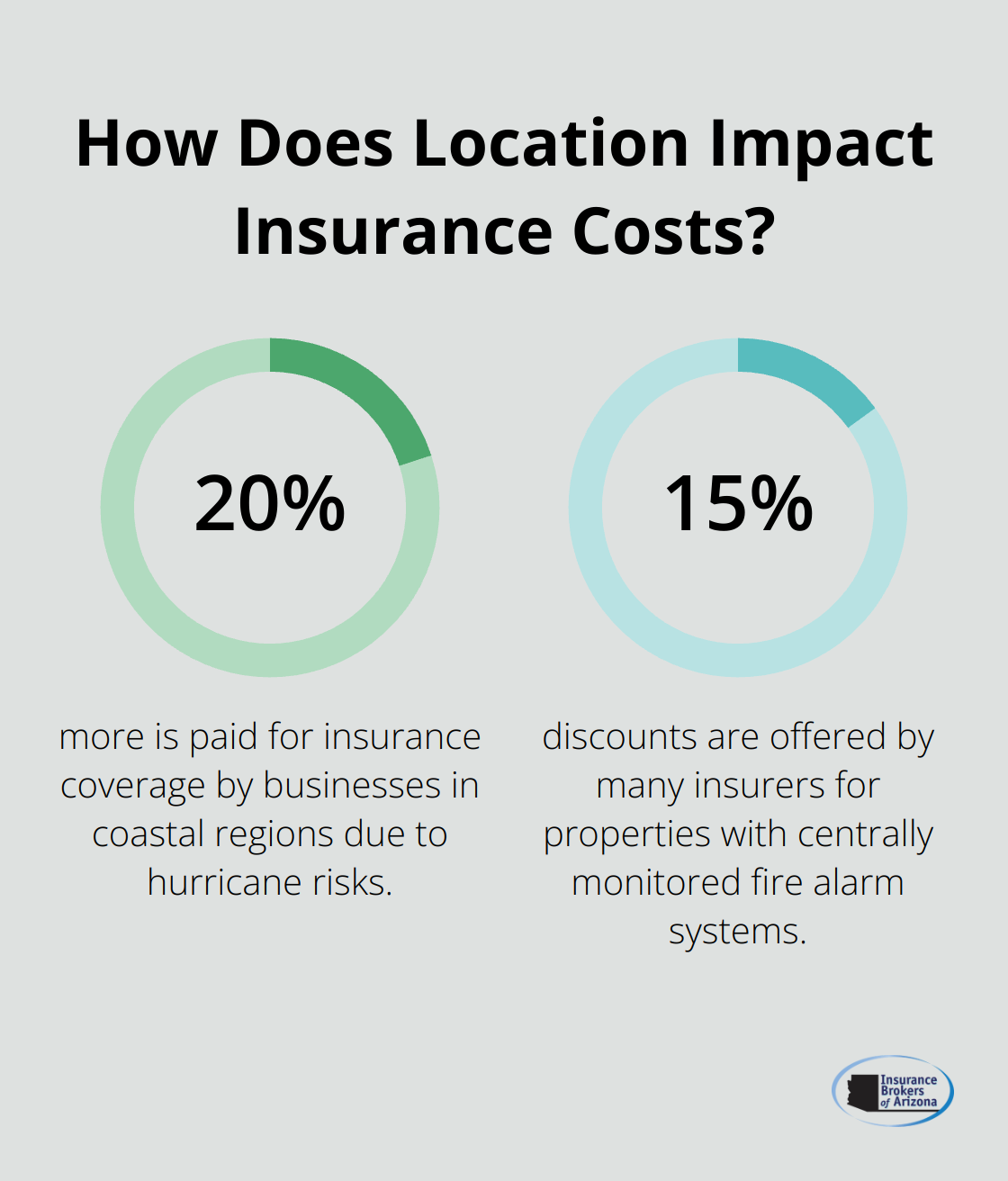

The geographical location of your commercial property significantly affects your hazard insurance premiums. Properties in areas prone to natural disasters (such as coastal regions vulnerable to hurricanes or zones with high earthquake risk) typically face higher premiums. The Insurance Information Institute reports that Florida, frequently affected by hurricanes, has some of the highest commercial property insurance rates in the United States.

Urban areas with higher crime rates may also see increased premiums due to the elevated risk of theft and vandalism. Properties near fire stations or in areas with robust emergency services might benefit from lower rates.

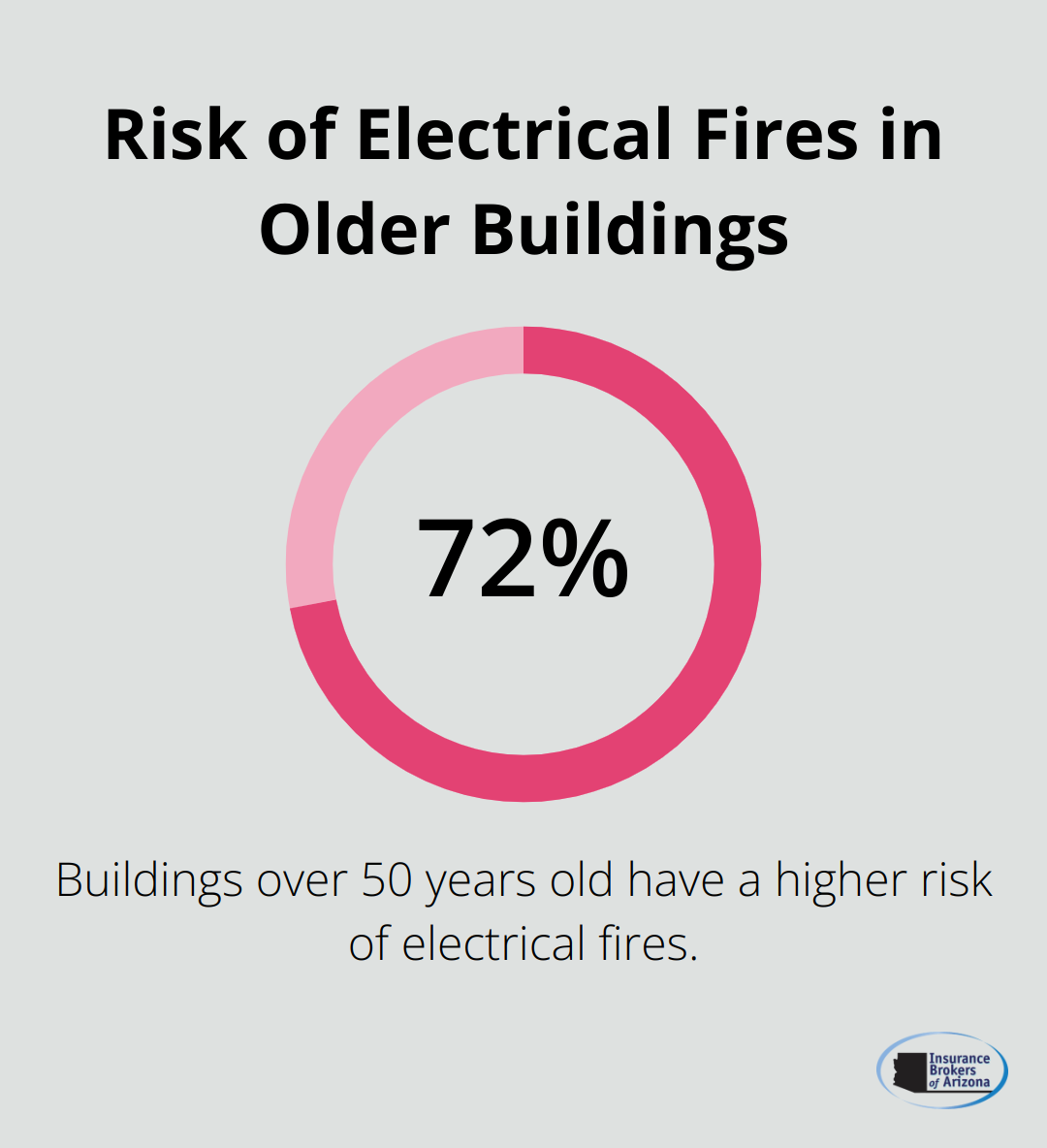

Building Characteristics and Condition Matter

The age, construction materials, and overall condition of your commercial property influence insurance premiums. Older buildings often come with higher premiums due to outdated electrical systems, plumbing, or structural components that may be more susceptible to damage. A study by FM Global found that buildings constructed with fire-resistant materials like concrete or steel can reduce fire-related losses by up to 70% compared to wood-frame structures.

Regular maintenance and upgrades can help lower your premiums. Replacing an old roof, updating electrical systems, or installing modern plumbing can demonstrate to insurers that you actively reduce risks, potentially leading to more favorable rates.

Safety and Security Measures Impact Costs

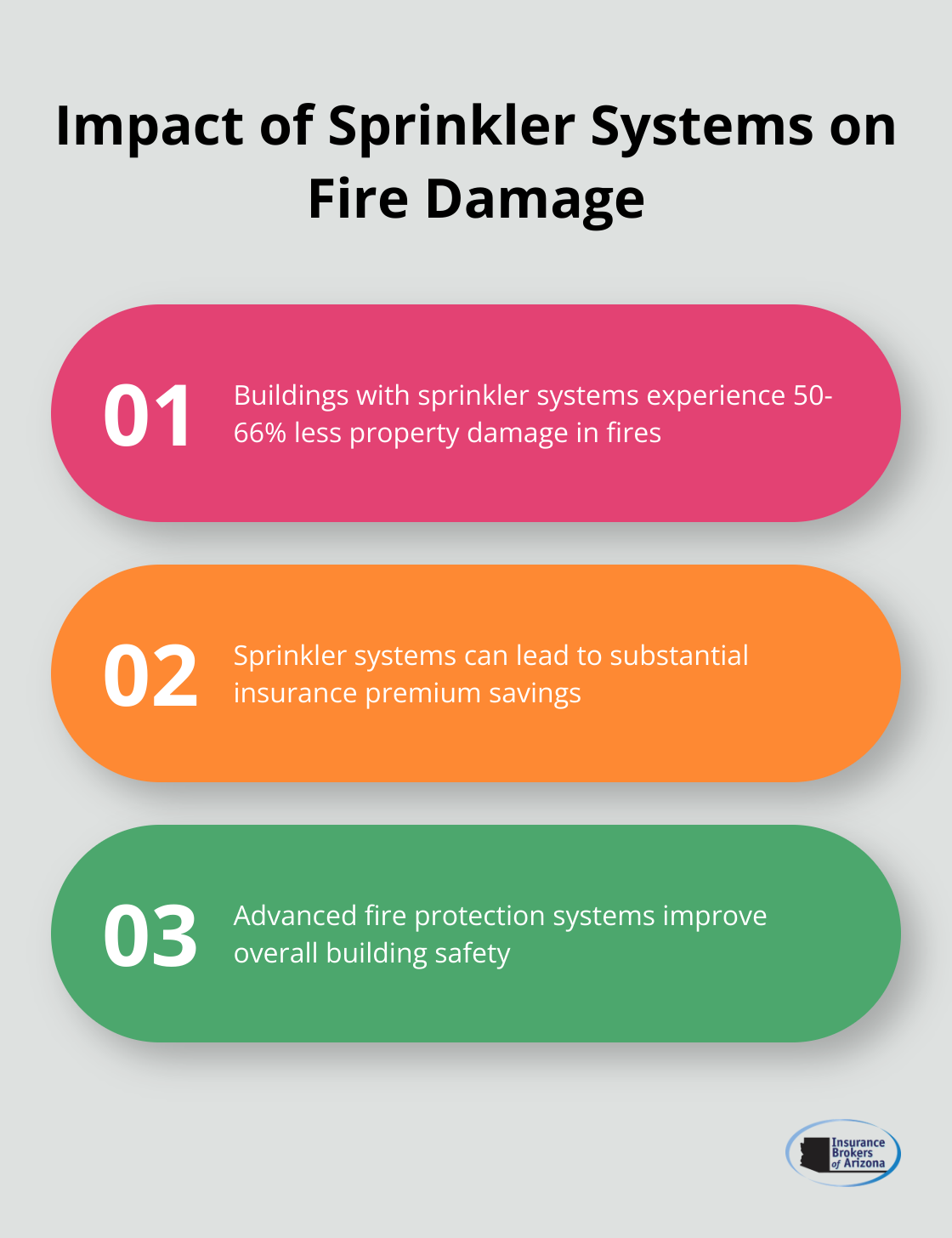

Implementing robust safety and security measures can substantially impact your hazard insurance premiums. The National Fire Protection Association states that buildings with sprinkler systems experience 50-66% less property damage in the event of a fire compared to those without. Advanced security systems, surveillance cameras, and access control measures can deter theft and vandalism, potentially lowering your insurance costs.

While there may be upfront costs, the long-term savings on insurance premiums and the added protection for your business assets can provide significant returns on investment.

Claims History and Risk Assessment Affect Rates

Your business’s claims history is a critical factor in determining insurance premiums. A history of frequent claims suggests to insurers that your property may be high-risk, leading to increased premiums. A clean claims record can work in your favor.

Insurance companies also conduct comprehensive risk assessments of your property and business operations. This evaluation considers factors such as the type of business you operate, the equipment you use, and any hazardous materials on-site. For example, a restaurant with multiple deep fryers may face higher premiums due to the increased fire risk compared to a standard office space.

To optimize your premiums, you can develop a robust risk management plan. This approach not only helps prevent incidents but also demonstrates to insurers your commitment to minimizing risks, potentially leading to more favorable rates.

Final Thoughts

Hazard insurance for commercial property protects businesses against various threats, from natural disasters to human-caused incidents. Without proper coverage, a single catastrophic event could lead to significant financial losses or business failure. We at Insurance Brokers of Arizona® offer personalized insurance products tailored to the unique needs of businesses in Arizona.

To secure the right coverage, conduct a thorough risk assessment of your property, considering factors such as location, building characteristics, and industry-specific hazards. Evaluate your current coverage limits and deductibles to ensure they align with your risk tolerance and financial capabilities. Review any exclusions in your policy and consider additional coverage for risks not included in standard policies (such as flood or earthquake insurance).

Update your insurance coverage regularly as your business grows and evolves. Inform your insurance provider about improvements to your property or new safety measures implemented. These updates may result in more favorable premiums and ensure your coverage remains adequate for your commercial property needs.