At Insurance Brokers of Arizona®, we often field questions about the differences between general liability insurance and workers’ compensation. These two types of coverage are essential for businesses, but they serve distinct purposes.

Understanding the nuances of general liability insurance and workers’ compensation is vital for protecting your company, employees, and customers. Let’s explore these two crucial forms of business insurance and how they work together to safeguard your enterprise.

What Is General Liability Insurance?

A Fundamental Business Safeguard

General liability insurance protects businesses against common risks. This type of insurance shields companies from financial losses due to third-party claims of bodily injury, property damage, and advertising injury.

Protection Against Third-Party Claims

When a customer slips and falls in your store, or your employee accidentally damages a client’s property while on a job, general liability insurance activates. It covers medical expenses for injuries and repair costs for damaged property. This protection includes legal defense costs if a lawsuit results from these incidents.

Advertising Injury Coverage

Businesses face risks beyond physical damages in today’s digital landscape. General liability insurance covers advertising injuries, which include claims of copyright infringement, libel, or slander. For example, if your marketing campaign unintentionally uses a trademarked slogan, this coverage helps with legal fees and settlements.

Real-World Applications

A construction company working on a residential project illustrates the importance of this coverage. If falling debris injures a passerby, general liability insurance would cover their medical expenses and any potential lawsuit. Similarly, for a retail store, if a customer’s expensive smartphone breaks due to a faulty display stand, this insurance would cover the replacement costs.

The Insurance Information Institute reports that 40% of small businesses will likely experience a property or general liability claim in the next 10 years. This statistic highlights the necessity of adequate coverage.

Customizing Coverage for Your Business

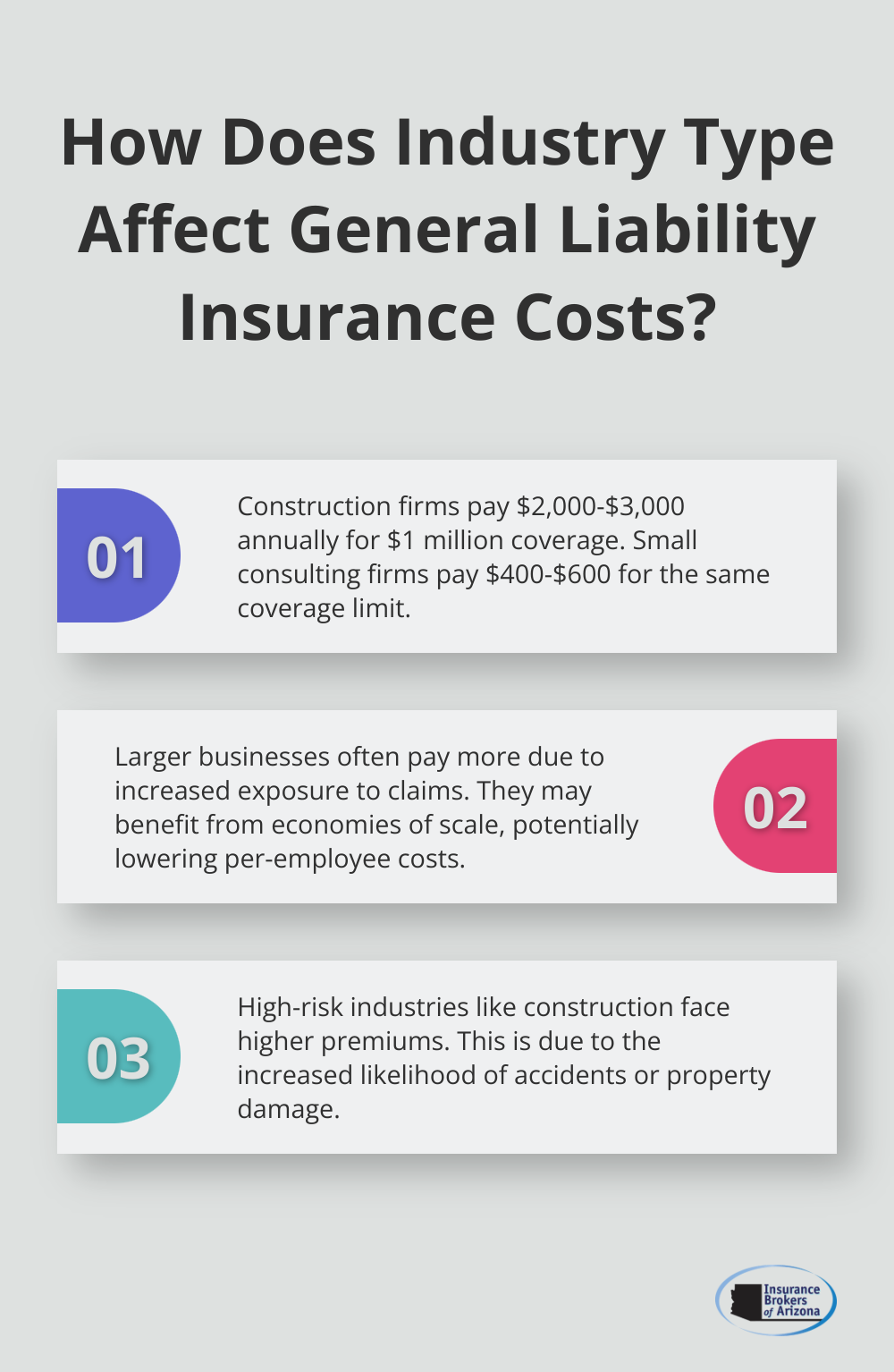

General liability insurance isn’t one-size-fits-all. The coverage needs of a small café differ significantly from those of a large manufacturing plant. Insurance professionals assess each business’s unique risks to recommend appropriate coverage limits and additional endorsements if necessary.

A technology company might need enhanced coverage for intellectual property disputes, while a food service business might require higher limits for potential food-borne illness claims. This tailored approach ensures businesses receive the most effective protection for their specific operations.

As we move forward, it’s important to understand how general liability insurance compares to other forms of business protection, such as workers’ compensation insurance. Let’s explore this essential coverage next.

What Is Workers Compensation Insurance?

A Vital Safety Net for Employees and Employers

Workers compensation insurance provides financial protection and medical care for employees who suffer job-related injuries or illnesses. It’s not just a benefit; it’s a legal requirement in most states.

Comprehensive Coverage Benefits

This insurance covers medical expenses, rehabilitation costs, and a portion of lost wages for employees injured or ill due to their job. For example, if a warehouse worker strains their back while lifting heavy boxes, workers comp would cover their medical treatment and provide income during recovery.

The National Safety Council reports that a worker is injured on the job every 7 seconds in the United States. This statistic highlights the necessity of robust workers compensation coverage.

State-Specific Mandates

Each state enforces its own workers compensation laws and requirements. In Arizona, all employers with one or more employees must carry workers compensation insurance. However, some states exempt very small businesses or certain types of workers.

The National Academy of Social Insurance found that workers compensation covered an estimated 142.6 million workers across the United States in 2022 (a testament to its widespread implementation in the American workplace).

Factors Influencing Insurance Costs

The cost of workers compensation insurance varies based on several factors:

- Industry risk level

- Payroll size

- Claims history

- State regulations

A construction company typically pays higher premiums than an accounting firm due to the increased risk of workplace injuries in construction.

Employer Obligations

Employers must not only purchase workers compensation insurance but also maintain a safe work environment. This includes providing safety training, implementing safety protocols, and promptly reporting workplace injuries.

The Occupational Safety and Health Administration (OSHA) reports that businesses can reduce their injury and illness costs by 20% to 40% by implementing effective safety and health programs (a significant incentive for prioritizing workplace safety).

Workers compensation insurance plays a pivotal role in protecting both employees and businesses from the financial and legal risks associated with workplace injuries. However, it’s essential to understand how this coverage differs from other forms of business insurance, such as general liability. Let’s explore these key differences in the next section.

How General Liability and Workers Compensation Differ

Protection Focus: Third Parties vs. Employees

General liability insurance protects businesses against claims from third parties, such as customers, vendors, or passersby. For example, it covers incidents where a customer slips and falls in a retail store. Workers compensation insurance, however, exclusively protects employees who suffer work-related injuries or illnesses. The National Safety Council reports that a worker suffers an injury on the job every 7 seconds in the United States (a statistic that underscores the importance of workers compensation coverage).

Incident Coverage: External vs. Internal

General liability insurance covers a wide range of incidents involving third parties, including bodily injury, property damage, and advertising injury. It would cover damages if a business’s advertising campaign unintentionally used copyrighted material. Workers compensation focuses solely on work-related injuries and illnesses affecting employees. This includes medical expenses, rehabilitation costs, and a portion of lost wages. The National Academy of Social Insurance found that workers compensation covered an estimated 142.6 million workers across the United States in 2022 (highlighting its widespread implementation).

Legal Requirements: Optional vs. Mandatory

While experts highly recommend general liability insurance for all businesses, most states do not legally require it. However, many contracts and leases may require businesses to carry this coverage. Workers compensation, on the other hand, is mandatory in most states for businesses with employees. In Arizona, all employers with one or more employees must carry workers compensation insurance. The specific requirements vary by state, so businesses must know their local regulations.

Cost Factors: Risk Assessment vs. Payroll-Based

The cost of general liability insurance depends primarily on the nature of the business, its size, location, and claims history. High-risk industries or businesses with a history of claims typically face higher premiums. Workers compensation premiums, however, largely depend on payroll size and the specific job classifications of employees. The Occupational Safety and Health Administration (OSHA) reports that businesses can reduce their injury and illness costs by 20% to 40% through effective safety and health programs, which can lead to lower workers compensation premiums.

Coverage Limits and Policy Structure

General liability policies often have per-occurrence and aggregate limits, which cap the amount the insurer will pay for a single claim and the total amount for all claims during the policy period. Workers compensation policies typically do not have such limits for medical benefits, ensuring that injured workers receive necessary care regardless of cost. However, wage replacement benefits often have caps based on state laws.

Final Thoughts

General liability insurance and workers’ compensation protect businesses in different ways. General liability shields against third-party claims, while workers’ compensation focuses on employee well-being. Legal requirements differ: general liability is often optional, but workers’ compensation is mandatory in most states, including Arizona, for businesses with employees.

Insurance costs vary based on different factors for each type of coverage. General liability premiums depend on business type and claims history, while workers’ compensation costs relate to payroll and job classifications. Both types of insurance create a comprehensive safety net that covers various risks and potential liabilities.

Insurance Brokers of Arizona® helps businesses navigate the complexities of general liability insurance and workers’ compensation. Our team assesses unique needs and risks to ensure the right coverage mix. We offer competitive options from over 40 reputable carriers, tailored to each business’s specific requirements (providing peace of mind and allowing you to focus on growth and success).