Small businesses face numerous risks, and protecting your company’s assets is paramount. At Insurance Brokers of Arizona®, we understand the importance of finding affordable coverage that doesn’t compromise on quality.

This guide will help you navigate the world of cheap general liability insurance for small businesses, ensuring you get the protection you need without breaking the bank.

What Is General Liability Insurance?

The Basics of General Liability Coverage

General liability insurance protects small businesses against common risks that could lead to financial ruin. This coverage typically includes bodily injury, property damage, and personal and advertising injury claims. For instance, if a customer slips in your store or an employee damages a client’s property, your general liability policy covers legal fees and potential settlements.

The Necessity for Small Businesses

Accidents happen, and lawsuits can be incredibly costly. A report by the U.S. Chamber Institute for Legal Reform reveals that a simple slip-and-fall claim can cost around $20,000. Without proper coverage, such an incident could force a small business to close its doors.

Risks Covered by General Liability Insurance

General liability insurance proves invaluable in several scenarios:

- Physical injuries on your premises

- Damage to someone else’s property

- Copyright infringement claims

- Reputational harm from advertising

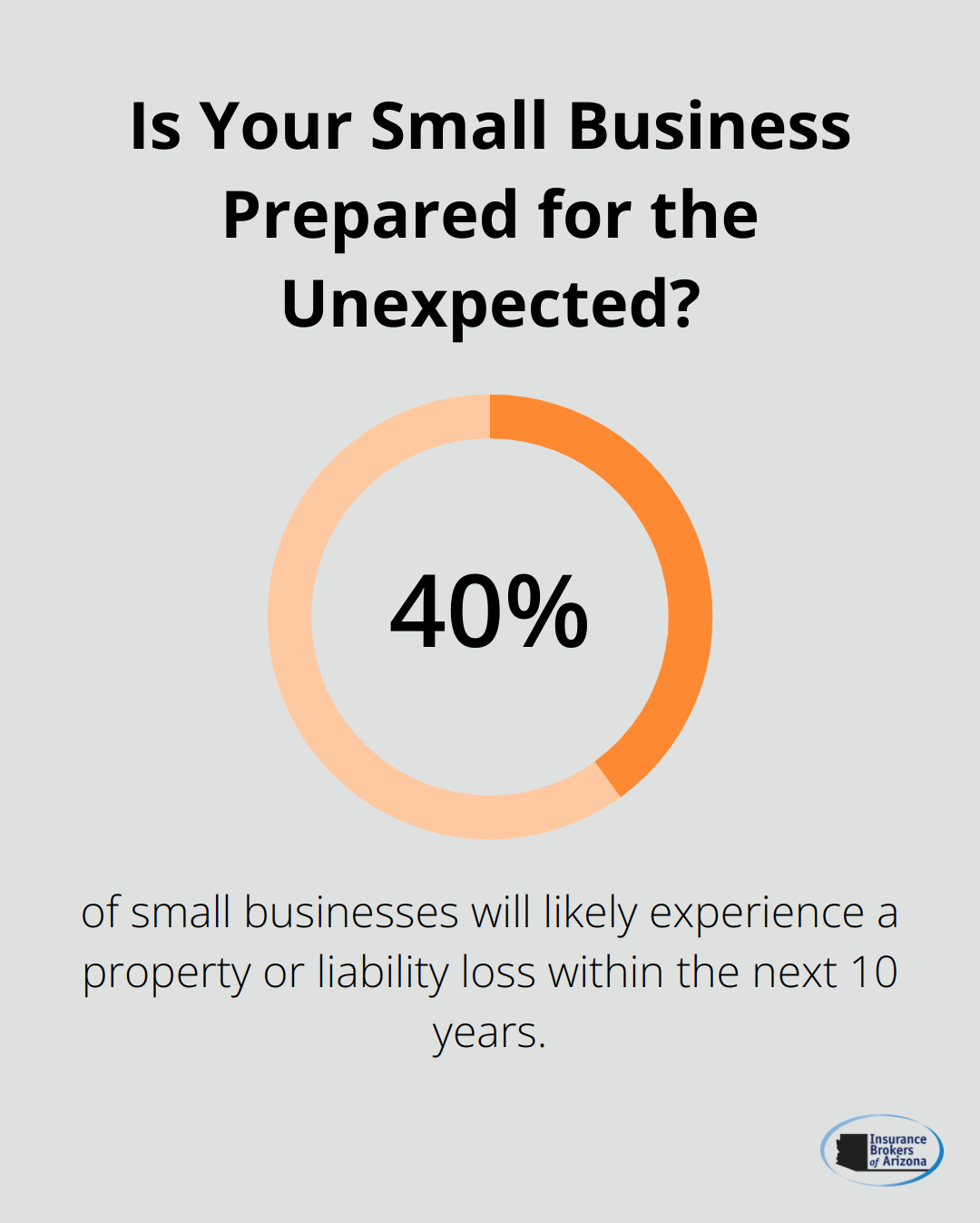

A study by The Hartford found that 40% of small businesses will likely experience a property or liability loss within the next 10 years. This statistic highlights the importance of preparation.

Industry-Specific Considerations

Different industries face varying levels of risk. According to data from Insureon, a construction company might pay around $80 per month for general liability insurance, while an accounting firm might pay only $29 per month. Insurance Brokers of Arizona® can help you understand the specific risks your business faces and tailor your coverage accordingly.

Beyond Protection: Building Credibility

General liability insurance isn’t just about protection-it’s also about credibility. Many clients and partners require proof of insurance before doing business with you. It signals that you’re a responsible and trustworthy professional.

As we move forward, we’ll explore the factors that influence the cost of general liability insurance (such as business type, revenue, and claims history). This information will help you find affordable options without compromising on necessary coverage.

What Impacts Your General Liability Insurance Costs?

Industry and Business Type

Your line of work significantly influences insurance costs. High-risk industries like construction or manufacturing typically face higher premiums due to increased chances of accidents or property damage. Insureon reports that construction businesses pay an average of $80 per month for general liability insurance, while low-risk industries (such as accounting) might pay only $29 per month.

Company Size and Revenue

The size of your business and its annual revenue directly impact your insurance costs. Larger companies with more employees and higher revenues generally pay more for coverage. This stems from their greater exposure to potential claims. A study by the National Association of Insurance Commissioners found that businesses with annual revenues under $500,000 paid an average of $500 per year for general liability insurance, while those with revenues over $1 million paid closer to $1,500 annually.

Claims History and Risk Management

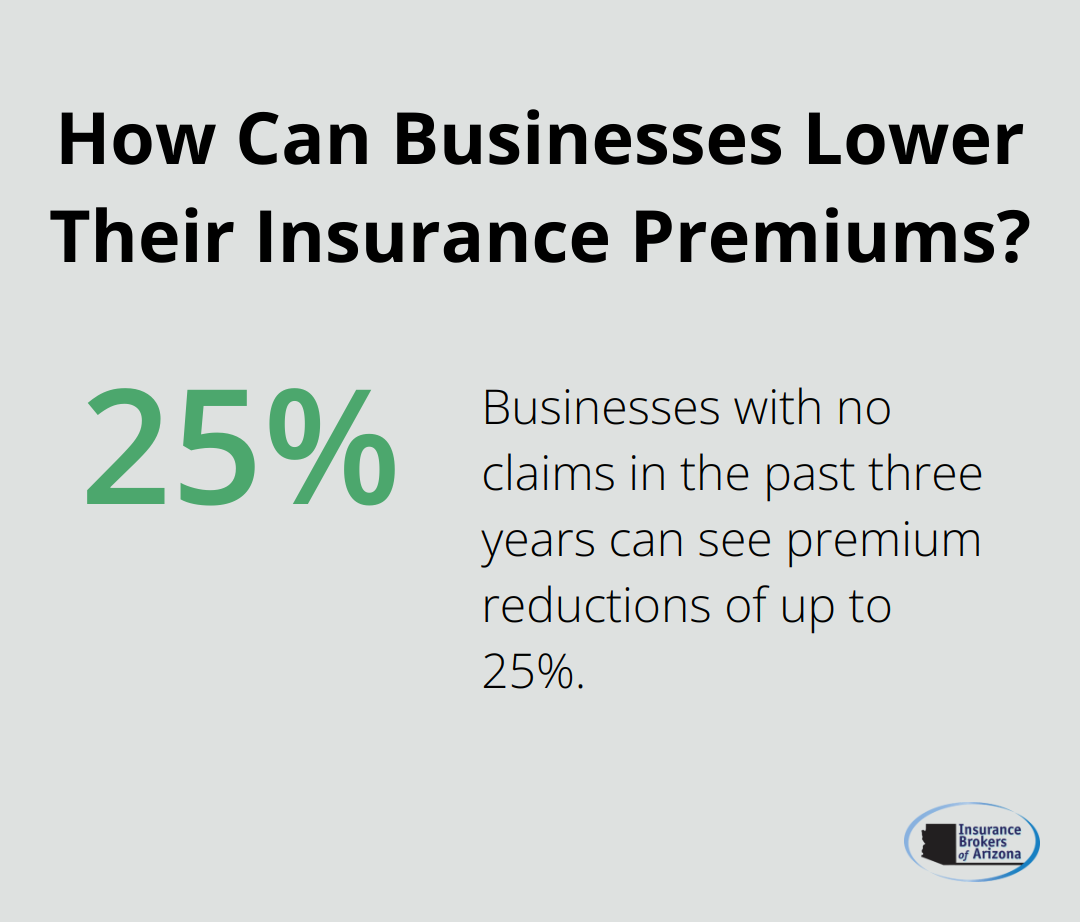

Your past claims history is a significant factor in determining future premiums. Insurers view businesses with a history of frequent claims as higher risk and may increase their costs. However, strong risk management practices can lead to lower premiums. The Insurance Information Institute reports that businesses with no claims in the past three years can see premium reductions of up to 25%.

Coverage Limits and Deductibles

The amount of coverage you choose and your deductible level also affect your costs. Higher coverage limits provide more protection but come with higher premiums. Opting for a higher deductible can lower your monthly payments, but it means you’ll pay more out-of-pocket if a claim occurs. For instance, raising your deductible from $500 to $2,500 could potentially reduce your premium by 10-20%.

Location and Local Regulations

Your business location plays a role in determining insurance costs. Areas prone to natural disasters or with higher crime rates may see increased premiums. Additionally, local regulations and legal environments can impact insurance costs. Some states have more stringent requirements or higher lawsuit frequencies, which can drive up premiums.

Understanding these factors helps you find affordable general liability insurance that meets your needs. Analyzing these elements allows you to find the right balance of coverage and cost. Working with an experienced insurance broker (like Insurance Brokers of Arizona®) can provide access to multiple carriers, enabling you to compare options and secure competitive rates tailored to your specific business situation. Now, let’s explore some practical strategies to find cheap general liability insurance without compromising on quality coverage.

How to Reduce Your General Liability Insurance Costs

Finding affordable general liability insurance doesn’t mean you must sacrifice quality coverage. Here are proven strategies to reduce your premiums while maintaining essential protection:

Compare Multiple Quotes

The insurance market is highly competitive, and rates can vary significantly between providers. A study by the National Association of Insurance Commissioners found that premiums for identical coverage can differ by as much as 300% between insurers. Don’t accept the first quote you receive. Instead, obtain quotes from at least three to five different insurance companies to ensure you get the best deal.

Bundle Your Policies

Many insurers offer substantial discounts when you combine multiple policies. For example, pairing your general liability coverage with a Business Owner’s Policy (BOP) or commercial property insurance can lead to savings of up to 15-20% on your overall premium costs. The Insurance Information Institute reports that bundling can result in average savings of $1,000 or more annually for small businesses.

Improve Your Risk Management

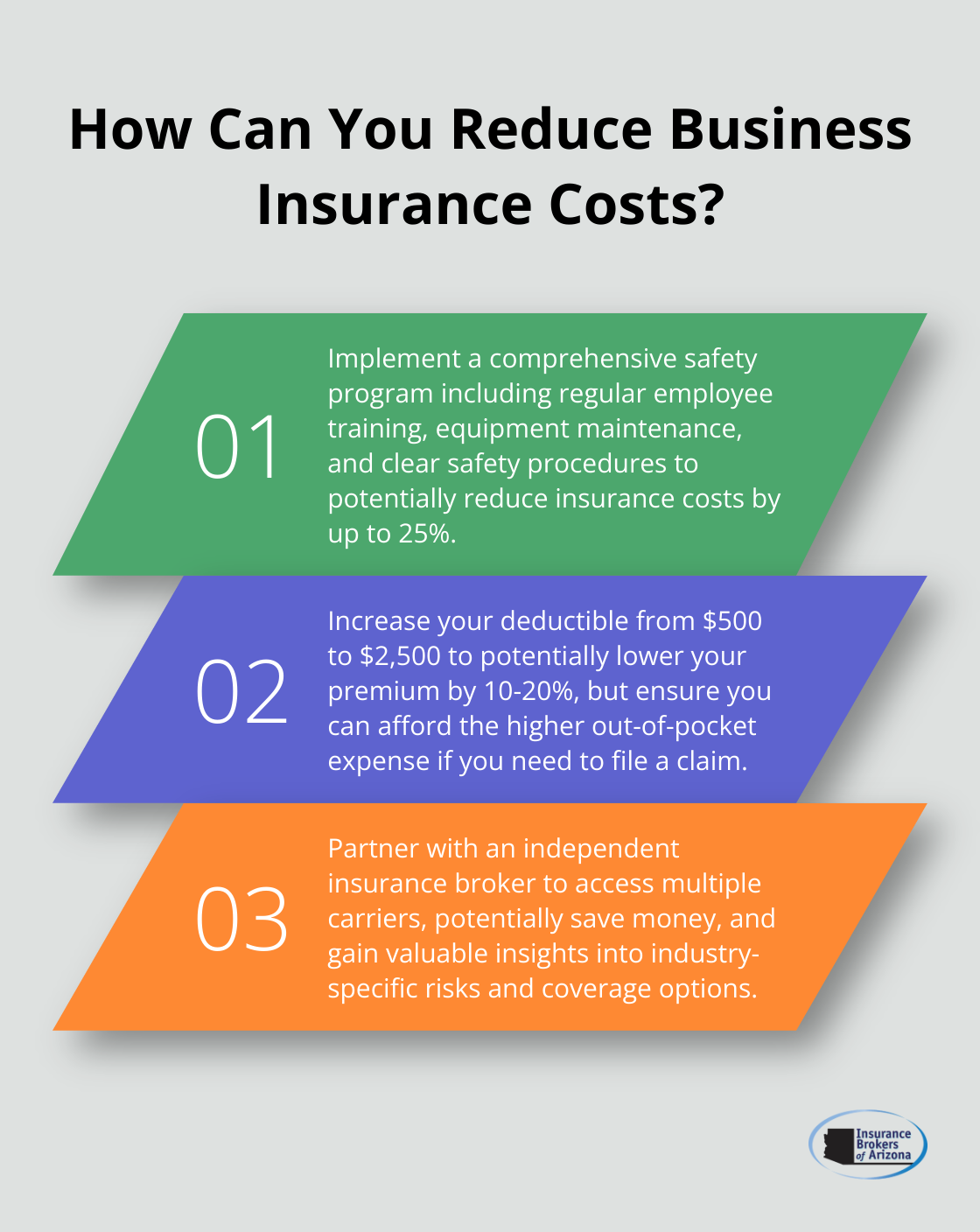

Implementing robust risk management practices not only protects your business but can also lead to lower insurance premiums. The Small Business Administration reports that companies with comprehensive safety programs can reduce their insurance costs by up to 25%. Consider measures such as:

- Regular employee safety training

- Proper maintenance of equipment and facilities

- Clear documentation of safety procedures

- Prompt addressing of potential hazards

Insurance companies often reward businesses that demonstrate a commitment to risk reduction with lower premiums.

Adjust Your Deductible

Selecting a higher deductible can significantly lower your monthly premiums. For instance, increasing your deductible from $500 to $2,500 could potentially reduce your premium by 10-20%. However, it’s important to ensure you can comfortably afford the higher out-of-pocket expense if you need to file a claim. Analyze your financial situation and risk tolerance to find the right balance.

Partner with an Independent Insurance Broker

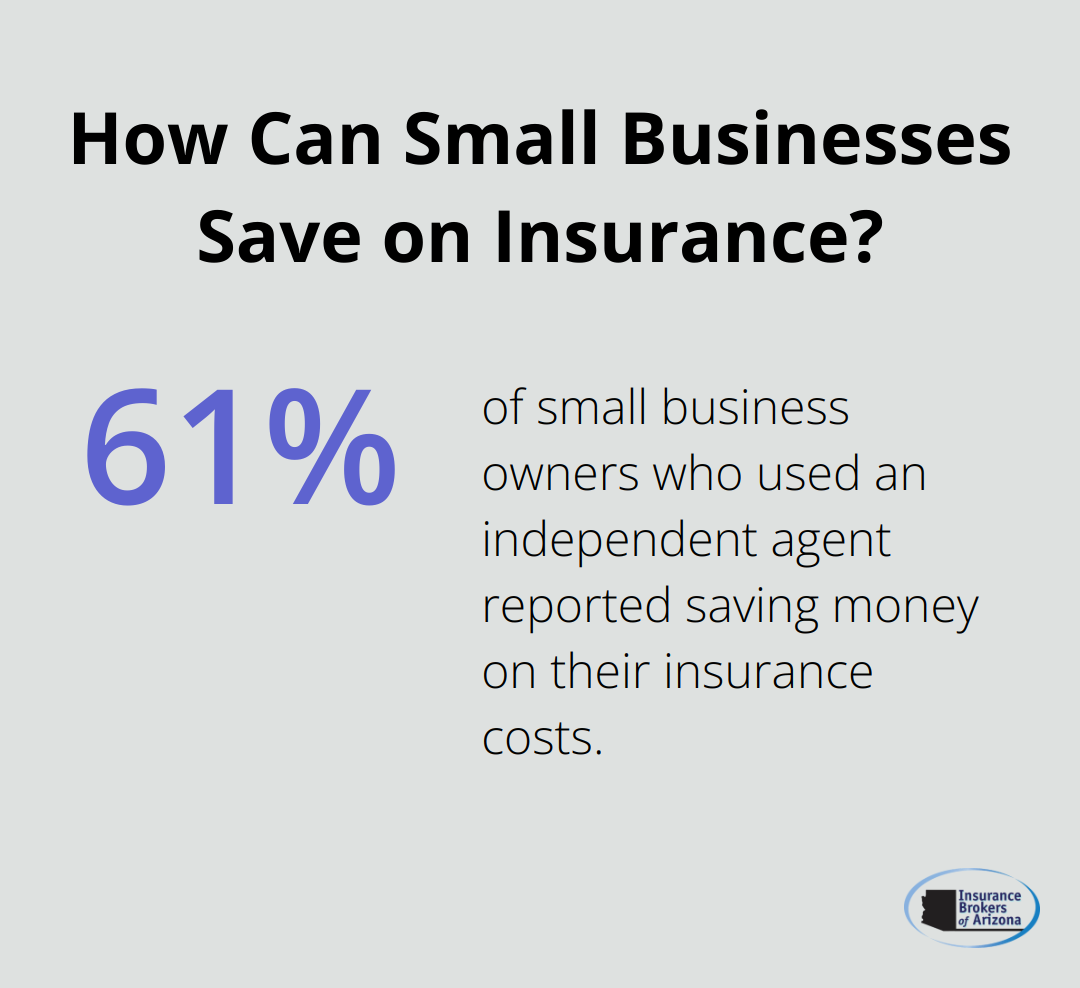

Independent insurance brokers (such as Insurance Brokers of Arizona®) have access to multiple carriers and can often secure better rates than you’d find on your own. A survey by the Independent Insurance Agents & Brokers of America found that 61% of small business owners who used an independent agent reported saving money on their insurance costs. These professionals can also provide valuable insights into industry-specific risks and coverage options, ensuring you’re not overpaying for unnecessary coverage or underinsured in critical areas.

Final Thoughts

General liability insurance protects small businesses from potentially devastating financial losses. The costs of this essential coverage vary based on factors like industry, business size, and claims history. Small business owners can secure cheap general liability insurance without compromising on quality coverage through strategic planning and informed decision-making.

Insurance Brokers of Arizona® specializes in helping small businesses navigate the complex world of insurance. Our team works with over 40 reputable carriers to provide personalized, competitive options tailored to your specific needs. We understand the unique challenges faced by small businesses in Arizona and strive to find the most cost-effective general liability insurance solutions.

Don’t let high premiums deter you from securing essential coverage. With the right approach and expert assistance, affordable general liability insurance for your small business is within reach. Take the first step towards protecting your business today by reaching out to Insurance Brokers of Arizona® for a personalized quote and expert advice on optimizing your coverage while minimizing costs.