Hard-to-Place Commercial Property Insurance Solutions

At Insurance Brokers of Arizona®, we understand the challenges property owners face when seeking hard-to-place commercial property insurance.

These high-risk properties often struggle to secure adequate coverage due to various factors, leaving owners vulnerable to significant financial risks.

Our team specializes in finding solutions for even the most complex insurance needs, ensuring that your valuable assets are protected.

In this post, we’ll explore the intricacies of hard-to-place commercial property insurance and provide strategies to help you navigate this challenging landscape.

What Makes Commercial Property Insurance Hard to Place?

Defining Hard-to-Place Insurance

Hard-to-place commercial property insurance covers properties that standard insurers deem too risky. These properties possess unique characteristics or circumstances that challenge conventional underwriting methods.

High-Risk Factors

Several elements can label a property as hard to place:

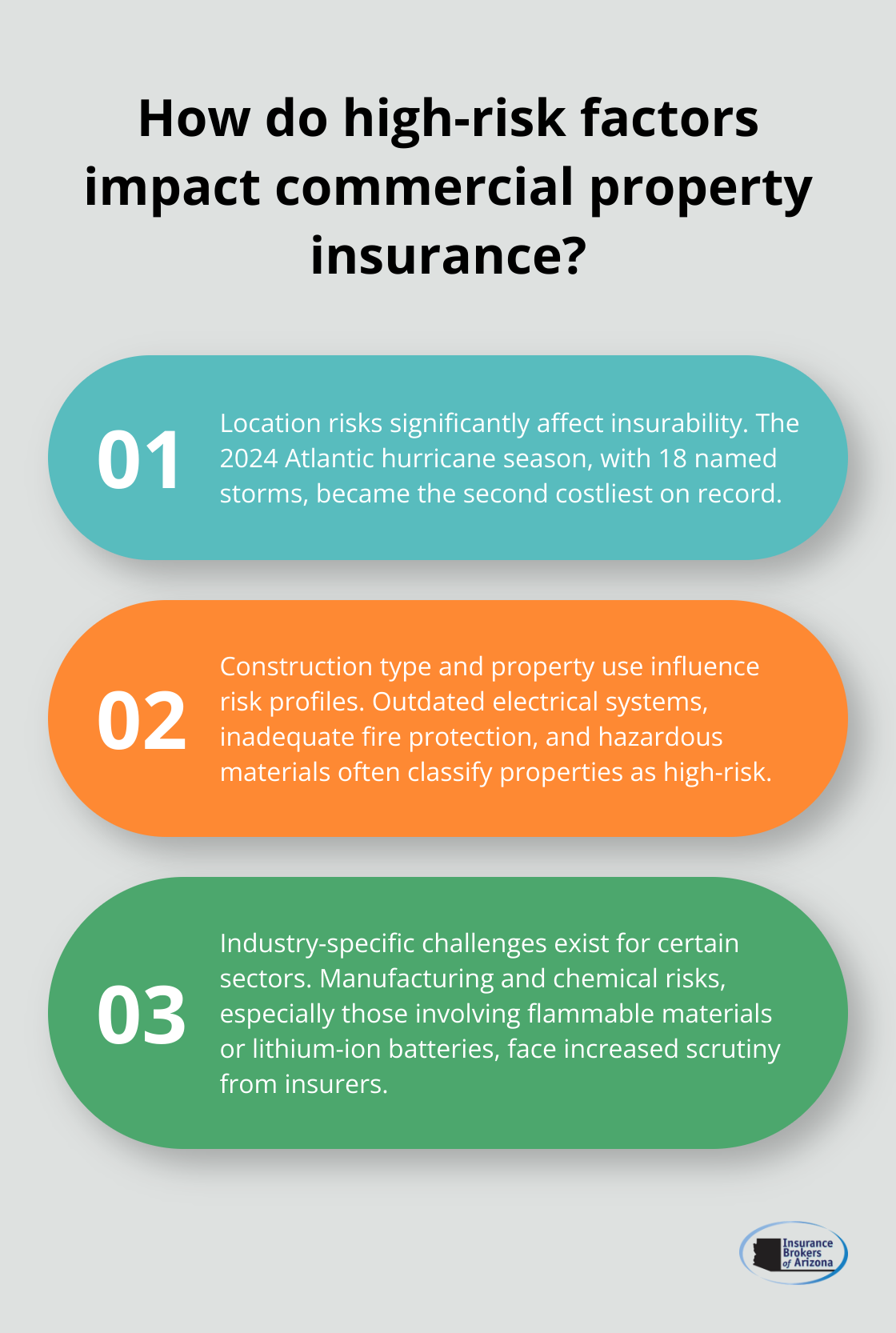

Location Risks

The property’s location significantly impacts its insurability. Areas prone to natural disasters (e.g., hurricanes, floods, wildfires) face higher risks. The 2024 Atlantic hurricane season (which recorded 18 named storms and became the second costliest on record) prompted insurers to reevaluate their exposure in coastal regions.

Construction and Occupancy Concerns

A property’s construction type and use affect its risk profile. Buildings with outdated electrical systems, inadequate fire protection, or those housing hazardous materials often fall into the high-risk category. Vacant or abandoned properties present unique challenges due to increased risks of vandalism, theft, or undetected damage.

Industry-Specific Challenges

Certain industries struggle more to secure property insurance:

Manufacturing and Chemical Risks

Manufacturers using flammable materials, chemical plants, and recycling facilities often classify as hard-to-place due to inherent fire risks. The presence of lithium-ion batteries in commercial properties has become a significant concern for insurers, necessitating thorough risk assessments and potentially increasing insurance costs.

Financial Considerations

A property’s claims history significantly impacts its insurability. Multiple past claims or a recent major loss can deter standard insurers from offering coverage. The property owner’s financial instability or a history of late premium payments can also contribute to a hard-to-place classification.

The Role of Specialized Brokers

Navigating the complex landscape of hard-to-place insurance requires expertise. Specialized brokers possess the knowledge and industry connections to find solutions for even the most challenging properties. These professionals understand the nuances of high-risk insurance markets and can often secure coverage where others might fail.

As we explore the challenges of obtaining hard-to-place commercial property insurance, it becomes clear that property owners face significant hurdles in protecting their assets. The next section will examine these obstacles in detail and provide insights into overcoming them.

Navigating the Challenges of Hard-to-Place Insurance

Limited Carrier Options

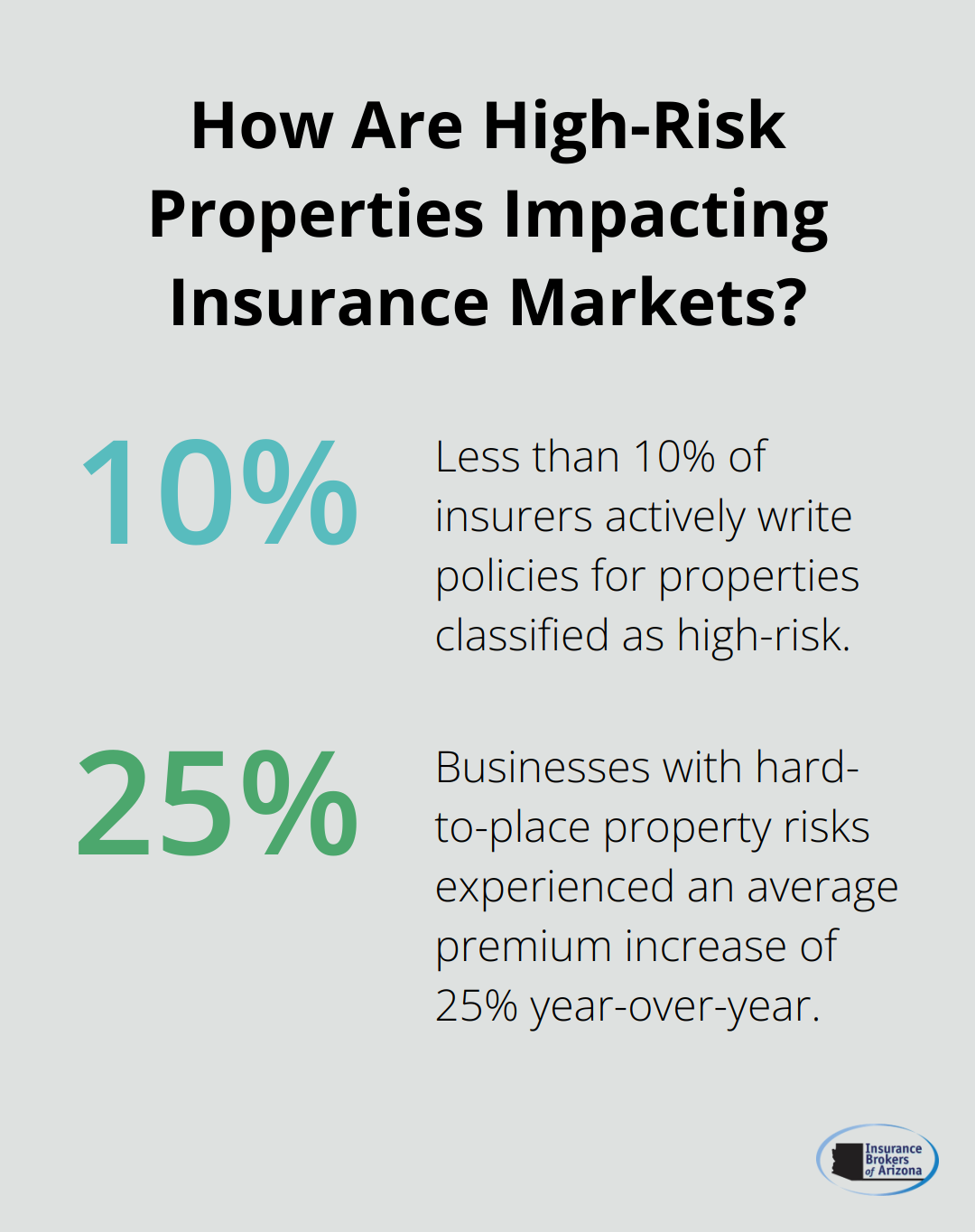

The scarcity of insurers willing to underwrite high-risk properties presents a significant obstacle in hard-to-place insurance. Standard insurance companies often avoid these risks, leaving property owners with few choices. A 2024 report by the National Association of Insurance Commissioners revealed that less than 10% of insurers actively write policies for properties classified as high-risk.

This restricted market creates a seller’s environment where insurers can be highly selective about the risks they choose to underwrite. Property owners may face rejection from multiple carriers before finding one willing to consider their application.

Financial Implications of High-Risk Coverage

When coverage is available, it often comes with a hefty price tag. Premiums for hard-to-place commercial property insurance can cost two to five times more than those for standard risks. Deductibles also tend to increase significantly, sometimes reaching $100,000 or more for certain perils.

A 2024 survey by the Risk and Insurance Management Society highlighted that businesses with hard-to-place property risks experienced an average premium increase of 25% year-over-year (compared to just 7% for standard risks). This financial burden can strain budgets and impact a company’s bottom line.

Strict Underwriting Requirements

Insurers that offer coverage for high-risk properties implement rigorous underwriting guidelines and demand extensive documentation. Property owners must provide detailed information on:

- Building construction and materials

- Fire protection systems and their maintenance records

- Security measures and protocols

- Historical loss data and risk management practices

- Financial statements and business continuity plans

The level of scrutiny can overwhelm property owners, and any gaps in information or perceived weaknesses in risk management can result in denial of coverage or unfavorable terms.

Complex Application Processes

The application process for hard-to-place commercial property insurance often proves lengthy and intricate. It may involve multiple rounds of questions, site inspections, and risk assessments. Insurers frequently require specialized reports such as engineering evaluations or environmental impact studies.

This complexity can cause delays in securing coverage, leaving properties exposed to risks during the application period. A 2024 study by the Insurance Information Institute found that the average time to secure coverage for hard-to-place risks was 45 days (compared to just 7 days for standard risks).

Property owners must prepare for a time-consuming and potentially frustrating process. Working with experienced brokers who understand the nuances of the hard-to-place market can improve the chances of a successful outcome.

While these challenges may seem daunting, solutions exist for hard-to-place commercial property insurance. The next section will explore strategies to overcome these obstacles and secure the necessary coverage for high-risk properties.

Securing Coverage for High-Risk Properties

Leverage Specialized Broker Expertise

Partnering with brokers who specialize in high-risk properties significantly improves your chances of securing coverage. These professionals have extensive networks and in-depth knowledge of niche markets. A 2024 study by the Independent Insurance Agents & Brokers of America found that 78% of hard-to-place risks successfully obtained coverage when working with specialized brokers (compared to only 32% who attempted to secure coverage independently).

Enhance Risk Management Practices

Implementing robust risk management strategies makes your property more attractive to insurers. This includes:

- Upgrading fire protection systems

- Improving security measures

- Developing comprehensive disaster recovery plans

- Conducting regular property maintenance and inspections

A 2024 report by FM Global revealed that properties with strong risk management practices experienced 66% fewer losses compared to those without such measures.

Explore Excess and Surplus Lines Markets

When standard markets reject a property, excess and surplus (E&S) lines offer viable alternatives. These specialized insurers have more flexibility in underwriting high-risk properties. The Wholesale & Specialty Insurance Association reported a 12% growth in E&S premiums for commercial property in 2024, indicating increased reliance on this market for hard-to-place risks.

Consider Alternative Risk Transfer Methods

For some high-risk properties, traditional insurance may not be feasible. Alternative options include:

- Captive insurance companies

- Risk retention groups

- Parametric insurance solutions

These methods can provide tailored coverage for unique risks. A 2024 Marsh report noted a 22% increase in the use of alternative risk transfer methods for hard-to-place commercial properties.

Improve Property Documentation

Thorough and accurate property documentation strengthens your insurance application. This includes:

- Detailed property valuations

- Comprehensive loss history reports

- Engineering assessments

- Risk mitigation plans

Clients who provide comprehensive documentation are 40% more likely to secure favorable terms for hard-to-place risks.

Final Thoughts

Hard-to-place commercial property insurance presents unique challenges, but property owners can overcome them with the right approach. Specialized brokers possess the knowledge and connections to find solutions in this complex landscape. These professionals guide clients through excess and surplus lines markets, alternative risk transfer methods, and rigorous documentation requirements.

Property owners must improve risk management practices to make high-risk properties more attractive to insurers. Upgrading safety systems, enhancing security measures, and implementing disaster recovery plans can reduce risks and improve insurability. These efforts increase the chances of securing coverage and can lead to more favorable terms and premiums.

Insurance Brokers of Arizona® specializes in finding tailored solutions for complex insurance needs. Our team’s expertise and extensive network of reputable carriers enable us to secure competitive options for high-risk properties. Don’t let the complexities of hard-to-place insurance leave your valuable assets unprotected (take action today to safeguard your property and business).