At Insurance Brokers of Arizona®, we understand that businesses need protection without breaking the bank.

Low cost general liability insurance is a vital shield for companies of all sizes.

This guide will explore what it covers, factors affecting its cost, and how to find affordable options that don’t compromise on quality.

What Is General Liability Insurance?

Core Protection for Businesses

General liability insurance serves as a fundamental safeguard for businesses of all sizes. It protects companies from financial losses due to third-party claims of bodily injury, property damage, and advertising injury. This coverage acts as a lifeline for businesses facing unexpected legal challenges.

Key Coverage Areas

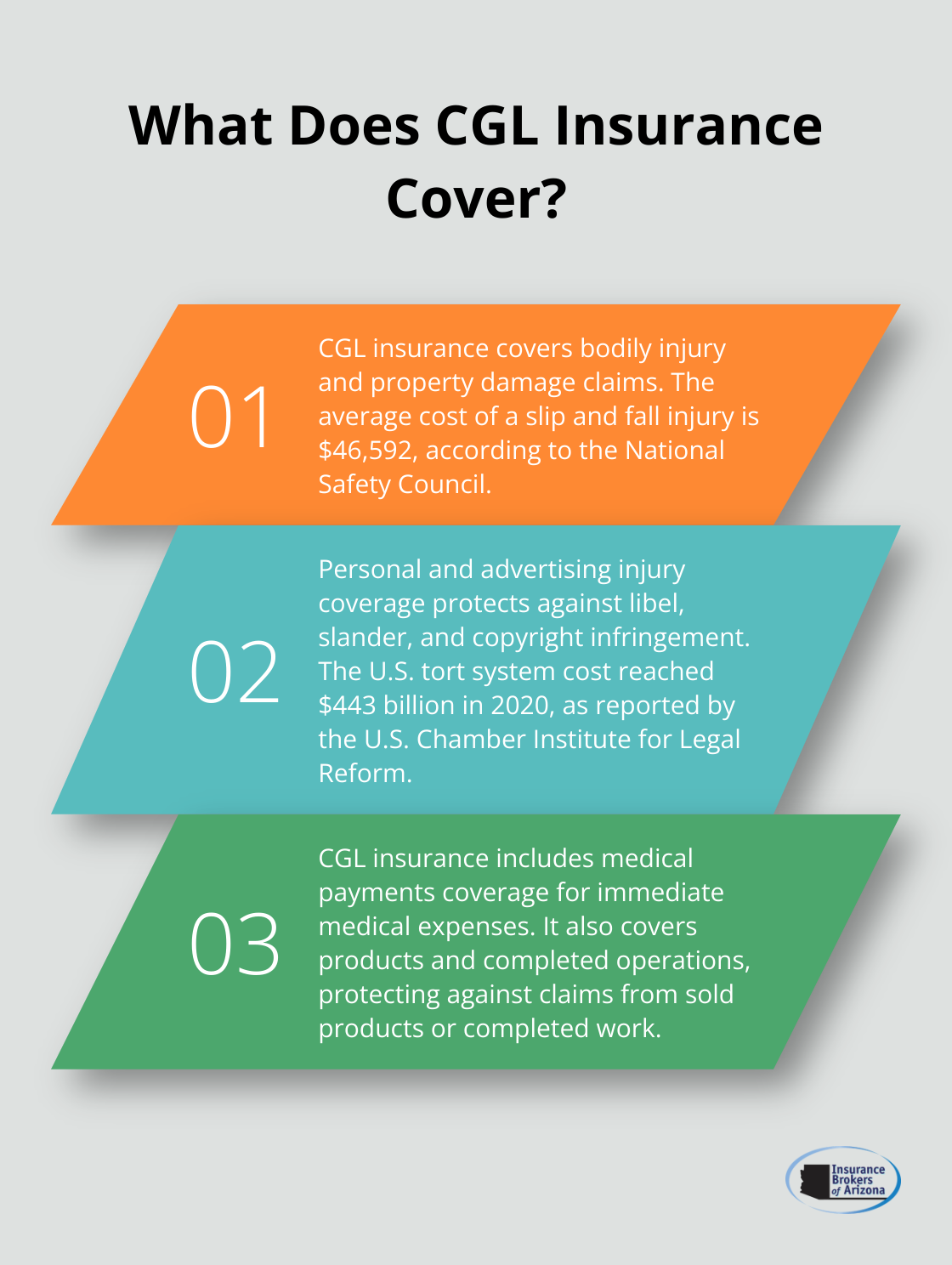

General liability insurance typically covers:

- Bodily Injury: This coverage helps pay for medical expenses and potential legal fees if a customer sustains an injury on your premises (e.g., a slip and fall in your store).

- Property Damage: When an employee accidentally damages a client’s property while on a job, general liability can cover the repair or replacement costs.

- Advertising Injury: This protects against claims of copyright infringement, libel, or slander in your marketing materials.

Importance for Businesses

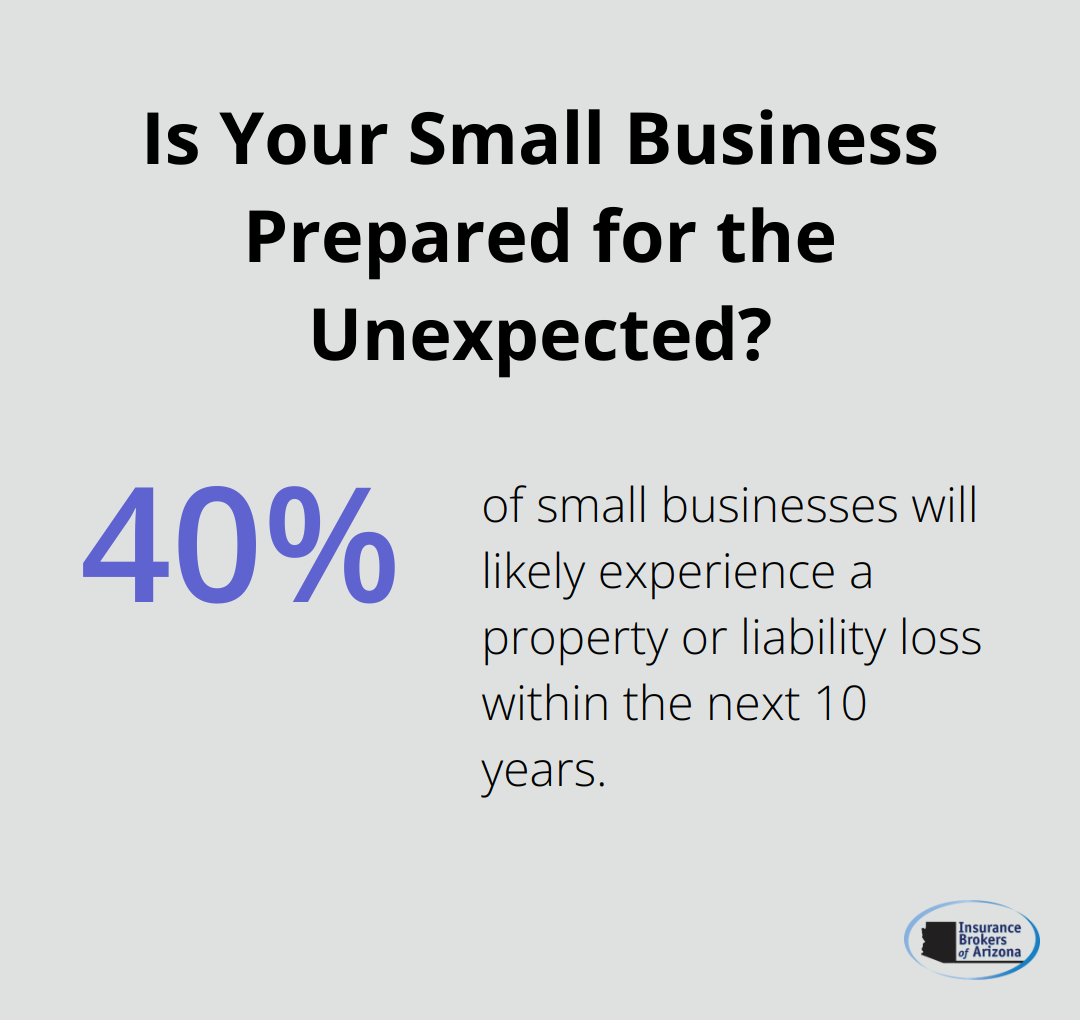

The significance of general liability insurance cannot be overstated. A study by The Hartford reveals that 40% of small businesses will experience a property or liability loss within the next 10 years. Without proper coverage, these losses could lead to financial ruin.

The National Safety Council reports that the average cost of a slip and fall claim is $20,000. A single lawsuit could easily bankrupt a small business without insurance. Additionally, many clients and landlords require proof of general liability insurance before entering into contracts or leases.

Real-World Applications

Consider these common situations where general liability insurance proves invaluable:

- A plumber accidentally floods a customer’s home while fixing a pipe. General liability covers the property damage.

- A marketing agency faces a lawsuit for using a copyrighted image in a client’s campaign. The policy covers legal defense costs and potential settlements.

- A delivery driver injures themselves while dropping off a package at a client’s office. General liability helps cover medical expenses and potential legal fees if the client faces a lawsuit.

These scenarios highlight why general liability insurance is not just a legal requirement in many cases, but a smart business decision. It provides peace of mind and financial protection, allowing you to focus on growing your business rather than worrying about potential lawsuits.

Finding the Right Coverage

As we move forward, it’s essential to understand the factors that influence the cost of general liability insurance. This knowledge will help you find affordable coverage that meets your specific business needs without compromising on quality.

What Drives General Liability Insurance Costs?

Business Size and Industry Impact

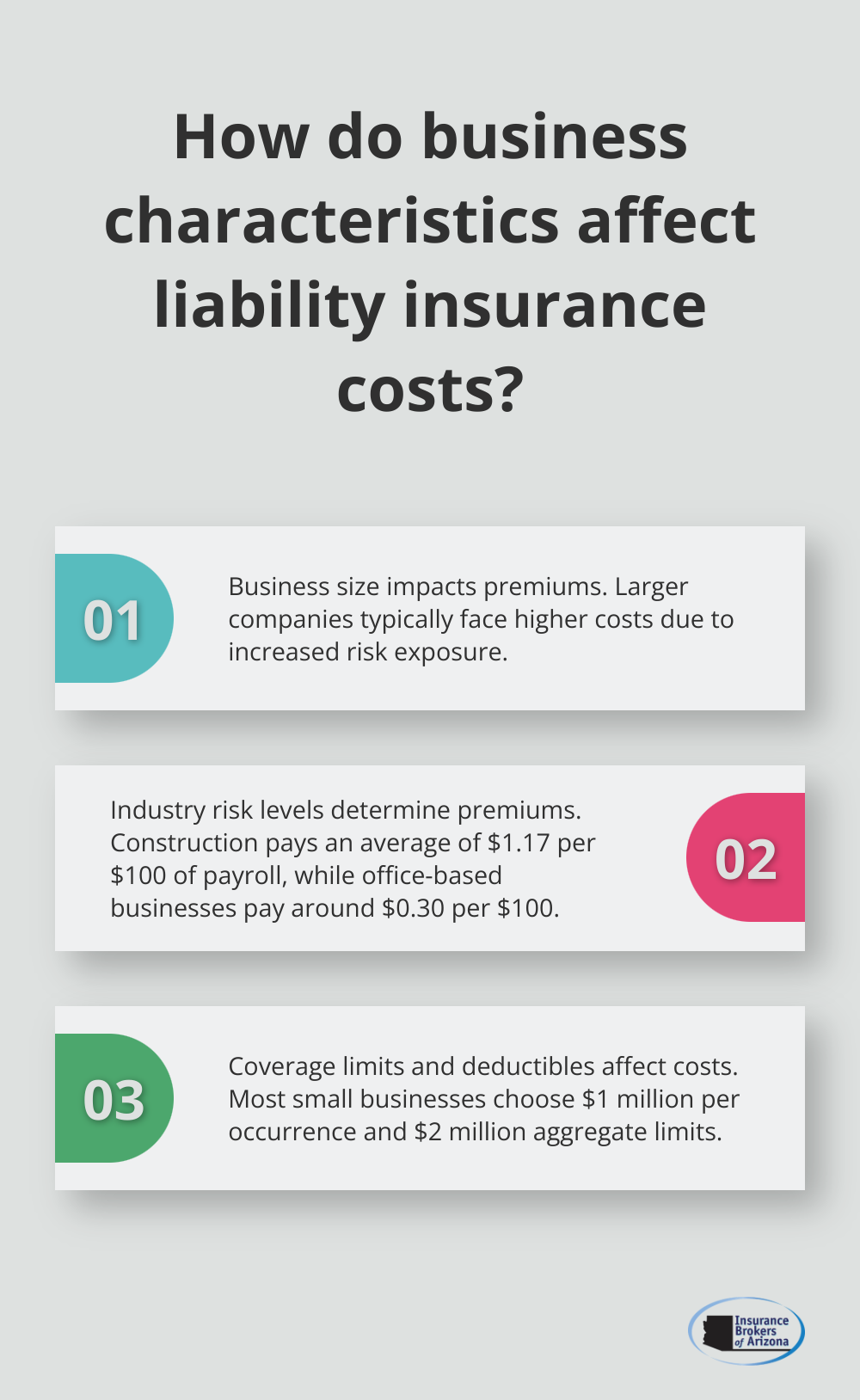

The size and nature of your business significantly impact your insurance costs. Larger companies typically face higher premiums due to increased exposure to risks. A construction company with 50 employees will likely pay more than a small accounting firm with five staff members.

Industry risk levels play a crucial role in determining premiums. High-risk industries such as construction or manufacturing face steeper costs compared to low-risk sectors like consulting or IT services. The National Association of Insurance Commissioners reports that the construction industry pays an average of $1.17 per $100 of payroll for general liability insurance, while office-based businesses might pay as little as $0.30 per $100.

Coverage Limits and Deductibles Matter

Your chosen coverage limits directly affect your premiums. Higher limits provide more protection but come at a higher cost. Most small businesses opt for a $1 million per occurrence limit with a $2 million aggregate limit. However, some industries or contracts may require higher limits.

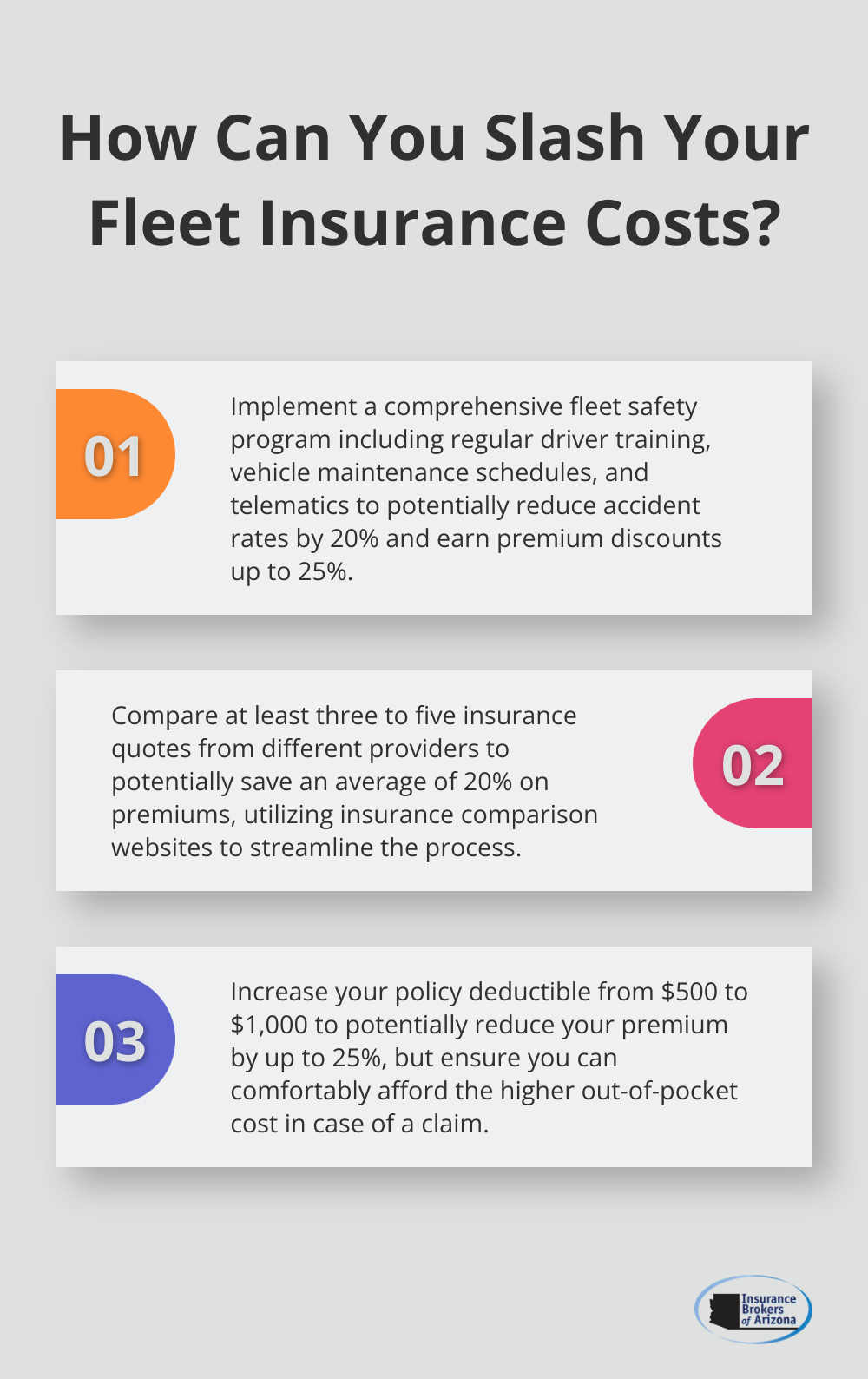

Deductibles also influence your insurance costs. A higher deductible can lower your premiums, but it means you’ll pay more out-of-pocket if a claim occurs. For instance, raising your deductible from $500 to $2,500 could potentially reduce your premium by 10-20%.

Claims History and Risk Management Strategies

Your claims history is a significant factor in determining your insurance costs. Businesses with a history of frequent claims are seen as higher risk and face higher premiums. According to industry data, even a single claim can increase your premium by 10-30% (depending on its severity).

Implementing effective risk management strategies can help lower your insurance costs over time. This includes employee safety training, regular maintenance of equipment, and clear customer communication policies. Insurance providers often offer discounts for businesses that demonstrate strong risk management practices.

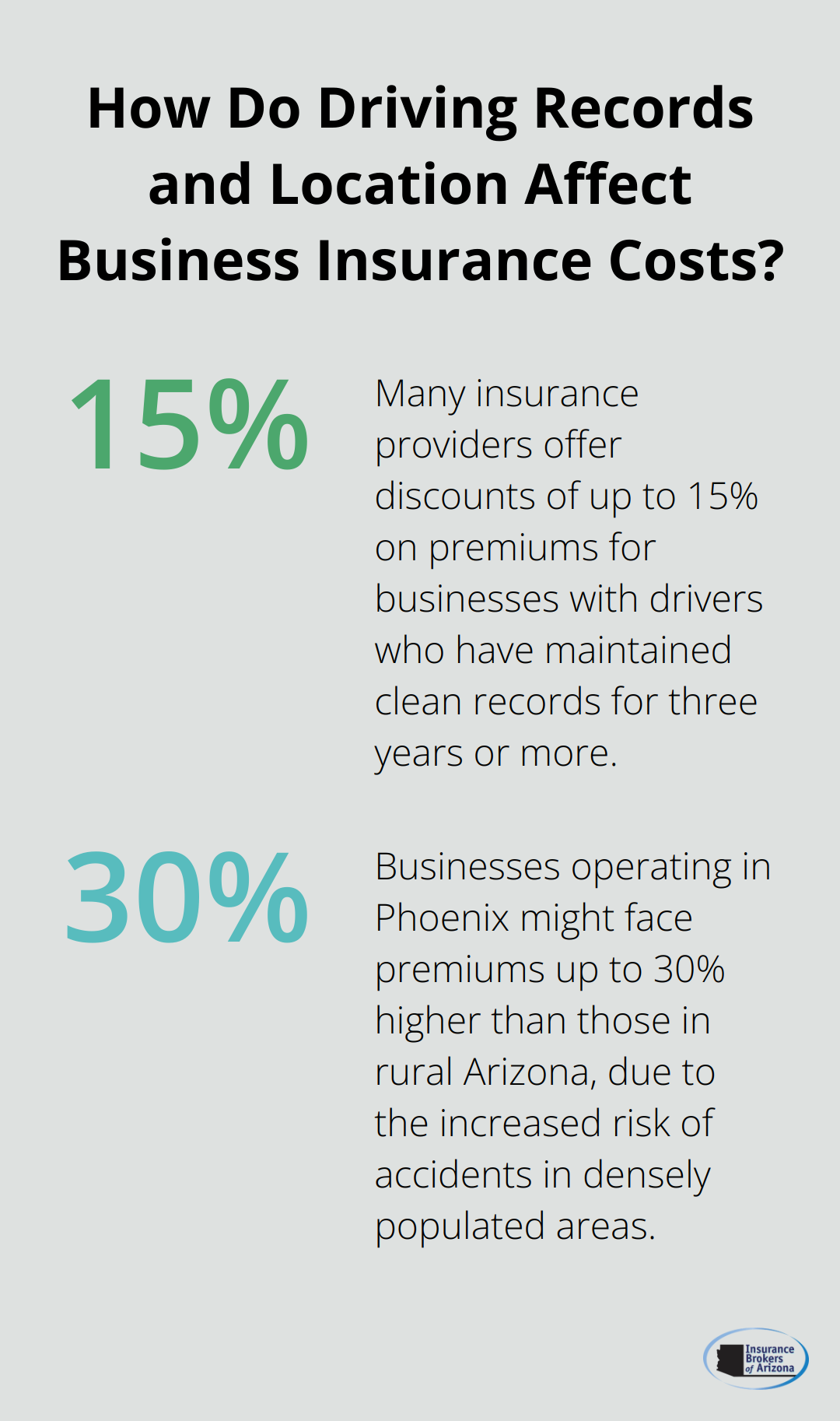

Location and Property Considerations

The location of your business can also affect your general liability insurance costs. Areas prone to natural disasters or with high crime rates may result in higher premiums. Additionally, the type and condition of your business property can impact costs. Well-maintained properties with up-to-date safety features may qualify for lower rates.

Industry Trends and Market Conditions

Insurance costs can fluctuate based on broader industry trends and market conditions. Economic factors, changes in regulations, and shifts in the insurance market can all influence premiums. Staying informed about these trends can help you anticipate potential changes in your insurance costs and plan accordingly.

Understanding these factors that drive general liability insurance costs empowers you to make informed decisions about your coverage. The next section will explore practical strategies to find low-cost general liability insurance without compromising on the quality of your protection.

How to Secure Affordable General Liability Insurance

Compare Multiple Quotes

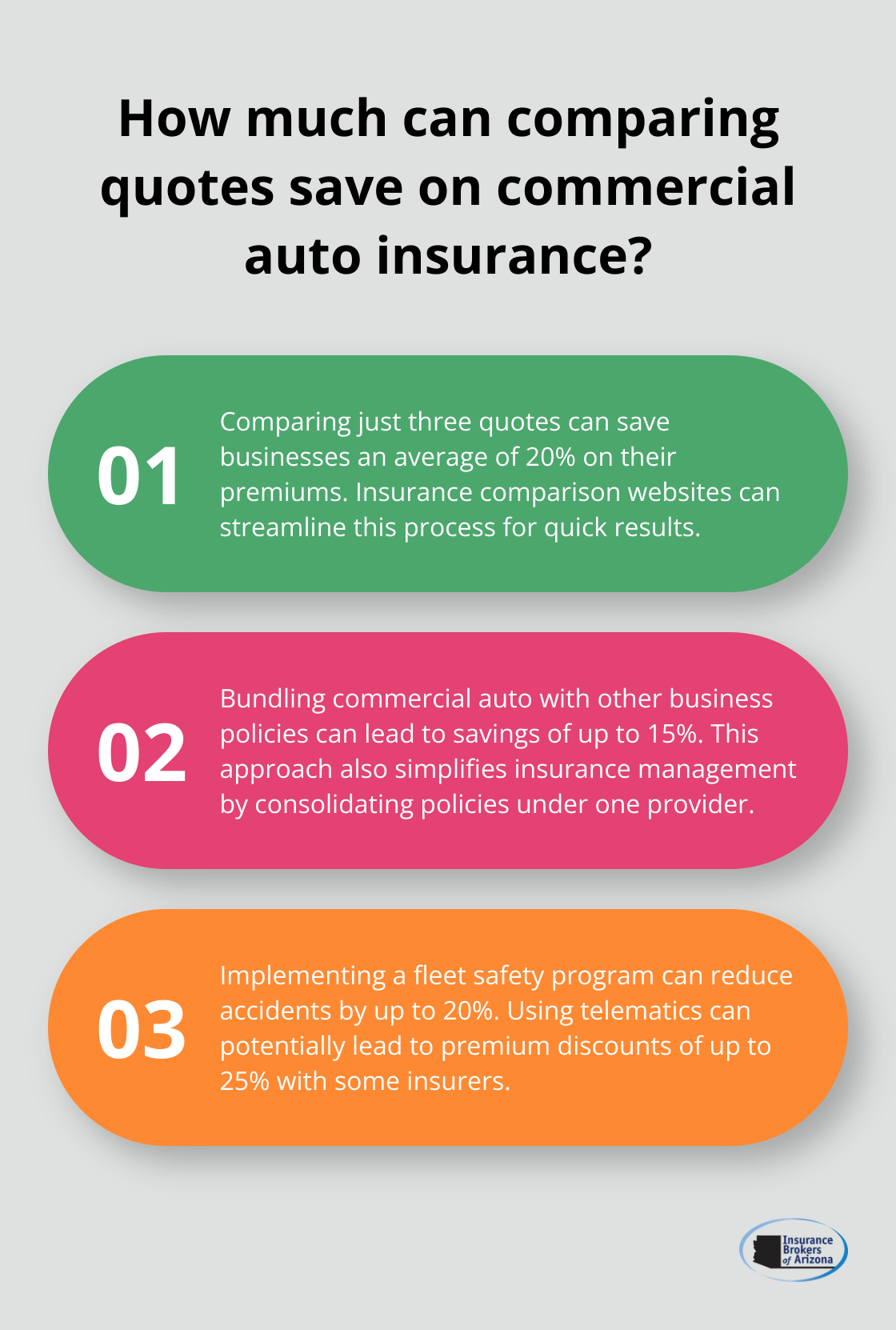

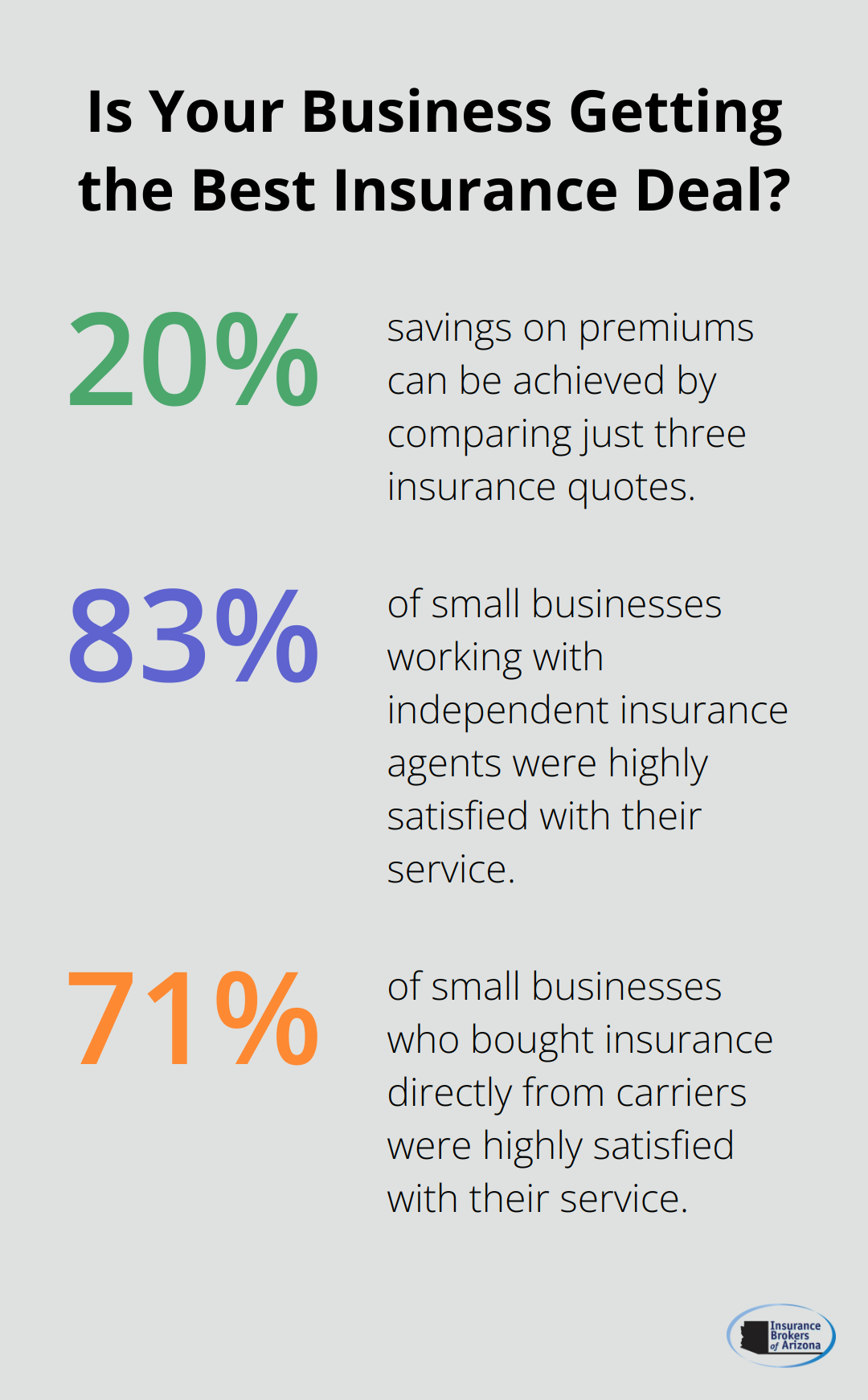

The insurance market offers competitive prices, with significant variations between providers. Use online comparison tools to obtain quotes from multiple insurers quickly. A study by the Insurance Information Institute revealed that comparing just three quotes can save up to 20% on premiums. Don’t limit yourself to online quotes. Speak directly with agents to understand each policy’s nuances and potentially negotiate better rates.

Optimize Your Coverage Limits

While high coverage limits seem attractive, they aren’t always necessary or cost-effective. Analyze your specific risks and select limits that adequately protect your business without overinsuring. For example, a small consulting firm might not need the same liability limits as a large construction company. The Small Business Administration recommends a $1 million per occurrence limit for most small businesses (adjusting as the company grows).

Implement Strong Risk Management Practices

Insurers prefer businesses that actively mitigate risks. Develop and document safety protocols, conduct regular employee training, and maintain your premises meticulously. The National Safety Council reports that businesses with strong safety programs can reduce injury rates by 50% or more. This approach not only protects employees and customers but can lead to significant premium reductions over time.

Bundle Your Policies

Many insurers offer discounts when you combine multiple policies. Combining your general liability with other coverages (like property insurance or workers’ compensation) can lead to savings of up to 15%, according to industry averages. Ensure that bundled policies still meet your specific needs and don’t compromise on essential coverage areas.

Work with an Independent Insurance Broker

Independent brokers have access to multiple carriers and can often find better rates than you would on your own. They understand the nuances of different industries and can tailor coverage to your specific needs. A survey by the Independent Insurance Agents & Brokers of America found that 83% of small businesses working with independent agents were highly satisfied with their service, compared to 71% who bought directly from carriers.

Final Thoughts

Low-cost general liability insurance protects businesses from financial losses due to third-party claims. Companies must balance affordability with adequate coverage to avoid leaving themselves vulnerable to significant risks. Comparing multiple quotes, implementing risk management strategies, and bundling policies can help secure cost-effective insurance without compromising quality.

At Insurance Brokers of Arizona®, we help businesses find the right balance between affordability and comprehensive coverage. Our partnerships with over 40 carriers allow us to offer a wide selection of personalized insurance products. We focus on understanding your unique requirements and securing the best rates for your business.

Let us help you safeguard your company’s future while keeping your insurance costs manageable. Our expertise and commitment to exceptional customer service will guide you through the process of obtaining low-cost general liability insurance that provides robust protection for your business. Contact us today to explore your options and secure the right coverage for your needs.