Arizona Commercial Truck Insurance: Protect Your Fleet the Right Way

Running a fleet in Arizona means navigating complex insurance requirements that protect both your business and your drivers. Arizona commercial truck insurance isn’t just a legal requirement-it’s your financial safeguard against accidents, cargo loss, and liability claims that could shut down operations.

We at Insurance Brokers of Arizona® help fleet owners understand what coverage they actually need and how to avoid overpaying. This guide walks you through state regulations, coverage types, and proven strategies to lower your premiums without cutting corners on protection.

Arizona and Federal Rules Require Specific Coverage for Commercial Trucks

Arizona law mandates that every commercial truck operating on public roads carry liability insurance with minimum coverage of $25,000 bodily injury per person, $50,000 per incident for multiple people, and $15,000 property damage liability according to the Arizona Department of Transportation. However, these state minimums fall short for most fleet operations. The Federal Motor Carrier Safety Administration sets a much higher baseline of $750,000 in combined single limit coverage for interstate motor carriers, though many insurers require $1,000,000 to account for actual claim costs in serious accidents. This gap between Arizona’s state minimum and federal requirements exposes operators who rely only on state minimums to catastrophic financial risk. Your insurer automatically reports all policy changes-cancellations, non-renewals, and new policies-to the Arizona Department of Motor Vehicles, so lapses in coverage are tracked immediately. If you fail to maintain continuous coverage, your vehicle registration and driver’s license face suspension, and police can seize your license plate without proof of insurance during stops or accidents.

Why State Minimums Leave You Vulnerable

State minimums cover bodily injury and property damage, but they ignore the exposures that actually drain fleet budgets. Cargo insurance protects goods in transit and becomes essential if you haul freight of any value. Physical damage coverage protects your vehicles themselves against collisions, theft, and weather-something state law doesn’t require but lenders do. Uninsured and underinsured motorist protection covers your drivers and assets when at-fault motorists lack sufficient resources, a scenario that occurs regularly on Arizona highways. For owner-operators leasing to carriers, non-trucking liability or bobtail coverage protects you during downtime when you operate outside dispatch.

Special Requirements for Passenger Transport Services

Arizona law imposes higher minimums for taxi, livery, and limousine services: $250,000 primary commercial liability and uninsured motorist coverage per incident while transporting passengers, dropping to $25,000 bodily injury per person when not actively transporting. These specialized requirements demand that drivers carry proof of insurance in the vehicle at all times during passenger transport. The distinction between active transport and downtime creates two separate coverage tiers that operators must maintain carefully.

How Maintenance and Safety Records Impact Your Rates

Vehicle maintenance directly influences both safety and insurance costs, since insurers review your maintenance records and driving history when calculating premiums. A clean safety record and consistent preventative maintenance reduce claims frequency and can lower your rates substantially. Your fleet’s condition and operational history become the foundation for the next critical decision: selecting the right coverage types that match your actual business needs.

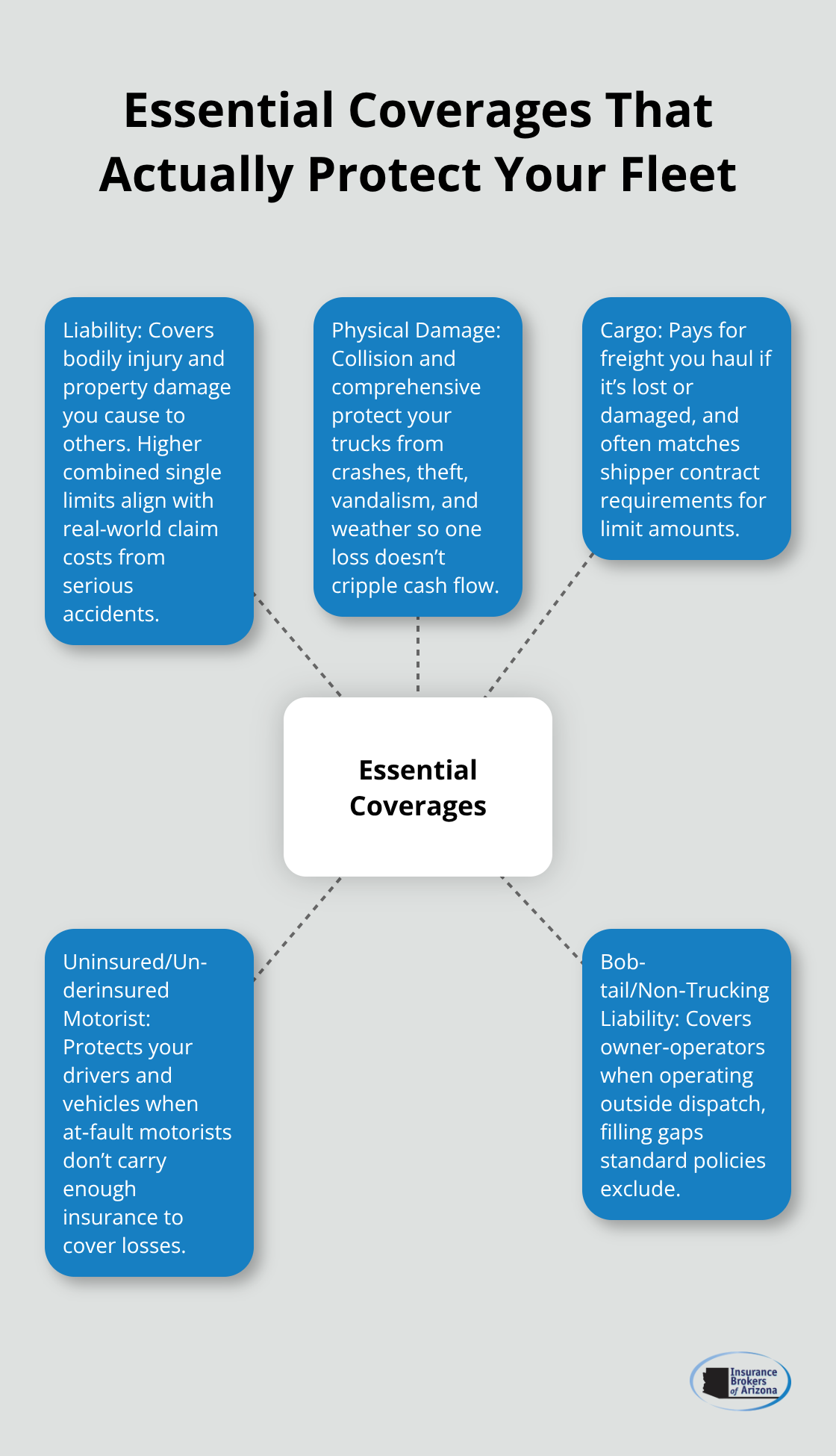

What Coverage Actually Protects Your Fleet

Liability Insurance Forms Your Foundation

Liability coverage forms the foundation of any commercial truck operation, but the coverage itself splits into two distinct protections that work together. Bodily injury liability covers medical expenses, lost wages, and pain-and-suffering claims when your driver injures someone else, while property damage liability covers vehicle repairs, property destruction, and other tangible losses from accidents you cause. Arizona requires minimums of $25,000 bodily injury per person and $15,000 property damage, but the Federal Motor Carrier Safety Administration baseline of $750,000 to $1,000,000 combined single limit exists because real accidents cost far more.

A serious multi-vehicle collision on Interstate 10 involving multiple injuries and vehicle damage routinely exceeds $500,000 in claims, making state minimums dangerously insufficient. Your liability limits directly determine how much protection you have when catastrophic accidents happen, and undersized limits leave your business exposed to judgments that exceed your coverage.

Physical Damage Coverage Protects Your Vehicles

Physical damage coverage protects your actual trucks through collision coverage for accidents and comprehensive coverage for theft, vandalism, weather, and other non-collision events. This coverage matters intensely because a single semi truck replacement cost runs $100,000 to $150,000, and losing even one vehicle without proper physical damage coverage can cripple cash flow for months. Your fleet represents your most valuable operational asset, and physical damage coverage keeps that asset protected against the full range of on-road and off-road risks.

Cargo Insurance Protects Goods in Transit

Cargo insurance becomes non-negotiable if you haul any freight of significant value, since liability coverage does not protect the goods themselves, only third-party injuries and property damage. A $50,000 cargo load lost to theft or accident requires dedicated cargo coverage to recover that value, and many shippers contractually require you to carry cargo limits matching shipment values. Without cargo coverage, you absorb the full loss when freight disappears or gets damaged in transit.

Uninsured Motorist and Bobtail Coverage Fill Critical Gaps

Uninsured and underinsured motorist coverage protects your drivers and vehicles when at-fault drivers lack sufficient insurance, a scenario that happens regularly on Arizona highways where not all motorists maintain adequate coverage. Owner-operators leasing to carriers should add non-trucking liability or bobtail coverage for the hours spent operating outside of dispatch, since your primary commercial coverage excludes personal use. These supplemental coverages address real exposure gaps that state minimums and standard commercial policies leave unprotected.

Matching Coverage to Your Actual Operations

One major claim without proper coverage can eliminate years of profit and force business closure, which is why matching coverage limits to your actual operational exposures matters far more than settling for legal minimums. Your cargo type, vehicle values, operating radius, and driver count all shape which coverage combinations protect your fleet most effectively. The next step involves understanding the specific cost factors that drive your premiums and identifying which adjustments actually reduce your rates without sacrificing protection.

What Actually Drives Your Truck Insurance Costs

Driver Safety Records Shape Your Premiums Most

Your driver’s safety record stands as the single most influential factor determining your premiums, far outweighing vehicle age or coverage adjustments. Insurers scrutinize motor vehicle records intensely because accidents and violations directly predict future claims, and a single at-fault collision can increase your rates by 20 to 40 percent or force non-renewal entirely. Arizona commercial truck operators face even steeper penalties than standard auto drivers because truck accidents cause significantly higher damages and injuries.

Strict hiring standards that include multi-year motor vehicle record checks protect your rates from the start. Standardized onboarding with ride-alongs assesses driving behavior before drivers operate your fleet independently. Zero-tolerance policies for distracted driving or safety violations send clear expectations to your team. A fleet with five drivers maintaining clean records over three years typically saves $3,000 to $8,000 annually compared to operators with violation histories, making driver management your most cost-effective loss control investment.

Training and Accident Response Procedures Reduce Claims

Training programs focused on defensive driving, load securement, and accident avoidance reduce claims frequency measurably, though generic training yields minimal results. Your drivers need scenario-based instruction covering the specific roads and conditions they actually encounter in Arizona operations. Establish formal accident response procedures before incidents occur, requiring drivers to document scene details, preserve dashcam footage immediately, and report within specific timeframes so claims adjusters receive complete information.

Vehicle Maintenance and Fleet Age Impact Rates

Vehicle maintenance schedules and fleet age influence rates because well-maintained trucks experience fewer breakdowns and accidents than neglected equipment. Daily driver vehicle inspection reports should cover tire tread depth, brake responsiveness, and load securement, with maintenance issues addressed before they create safety hazards or trigger claims. Newer trucks with advanced safety features like automatic braking systems sometimes qualify for modest rate reductions, though insurers weight safety records far more heavily than vehicle age alone.

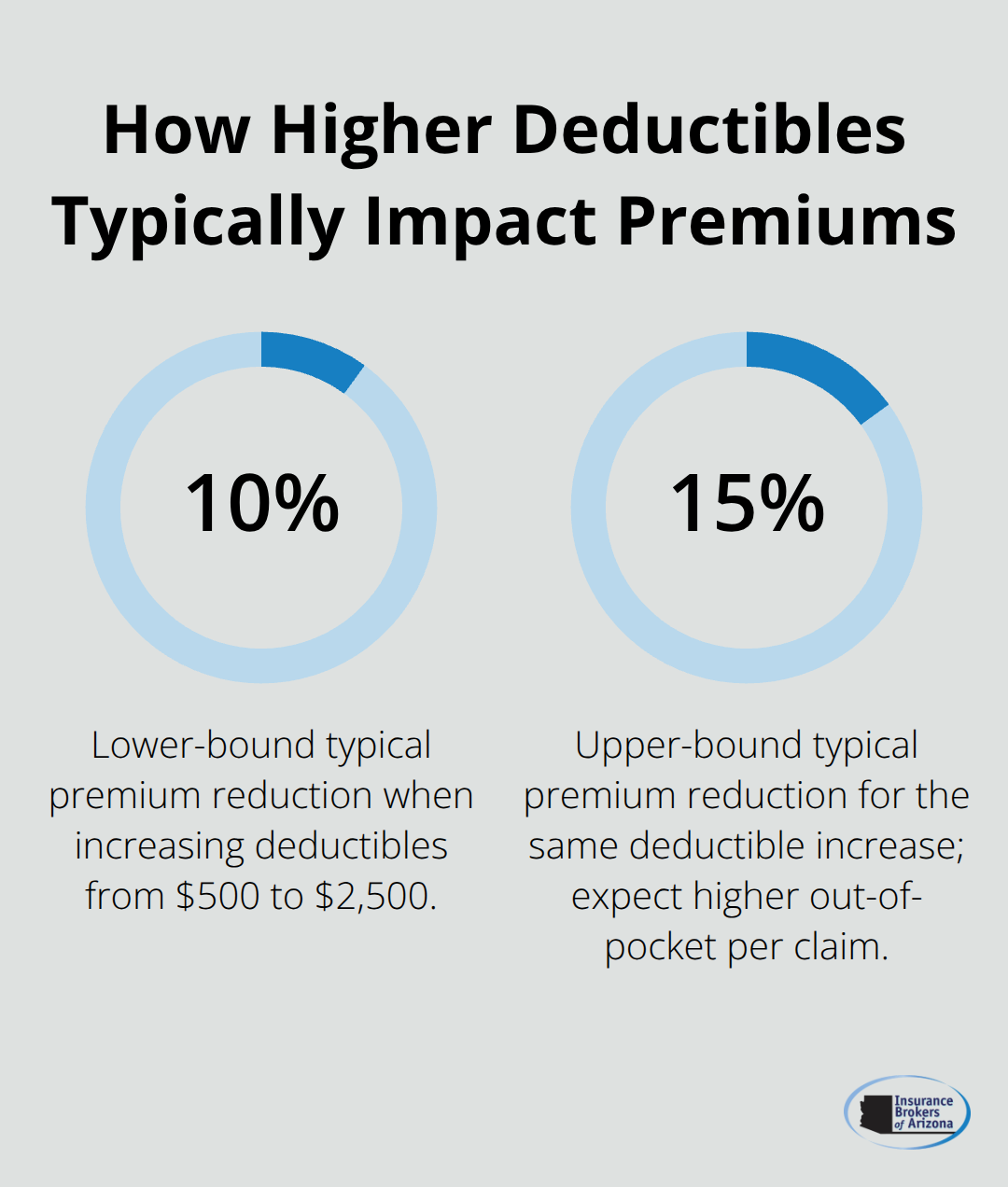

Deductibles, Operating Radius, and Cargo Type Control Costs

Your coverage limits and deductible choices directly control your out-of-pocket exposure and premium costs. Raising deductibles from $500 to $2,500 typically reduces your annual premium by 10 to 15 percent, but you’ll absorb that higher amount after each claim.

Most fleet operators find the sweet spot between $1,000 and $2,500 deductibles, balancing manageable out-of-pocket costs against meaningful premium savings.

Your operating radius matters substantially because regional routes within Arizona cost less to insure than multi-state operations, and cross-state travel exposes you to unfamiliar highways and higher accident risk. Cargo type directly influences your rates since transporting hazardous materials or high-value freight increases liability exposure dramatically compared to general freight operations.

Final Thoughts

Protecting your Arizona commercial truck insurance strategy means matching your coverage to actual operational exposures rather than accepting legal minimums that expose you to financial ruin. State minimums of $25,000 bodily injury and $15,000 property damage collapse when a single serious accident exceeds $500,000 in claims, which is why federal requirements demand $750,000 to $1,000,000 in combined single limit coverage. Your liability foundation, physical damage protection, cargo coverage, and uninsured motorist safeguards work together to shield your business from the financial devastation that one major claim inflicts.

The cost factors you control directly determine your premiums, with driver safety records mattering most and clean records saving $3,000 to $8,000 annually compared to violation histories. Strict hiring standards, scenario-based training, and formal accident response procedures reduce claims frequency measurably, while vehicle maintenance schedules and deductible choices between $1,000 and $2,500 balance protection against premium costs effectively. Your operating radius and cargo type shape rates substantially, making these operational decisions inseparable from your insurance strategy.

Arizona commercial truck insurance becomes manageable when you understand what protects your fleet and which adjustments genuinely reduce costs without sacrificing coverage. We at Insurance Brokers of Arizona® work with fleet owners across Arizona to match coverage limits to operational realities and identify premium savings through partnerships with reputable carriers. Contact us today for a personalized review of your current coverage and a competitive quote that reflects your specific fleet needs and safety record.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.