Artisan Contractor Insurance Quotes: How To Compare And Save

Artisan contractor insurance quotes vary wildly depending on your coverage needs and business setup. Getting the right price means understanding what you actually need to protect, then comparing options from multiple carriers.

We at Insurance Brokers of Arizona® help contractors cut through the confusion and find real savings. This guide walks you through the process step by step.

What Coverage Do Artisan Contractors Actually Need

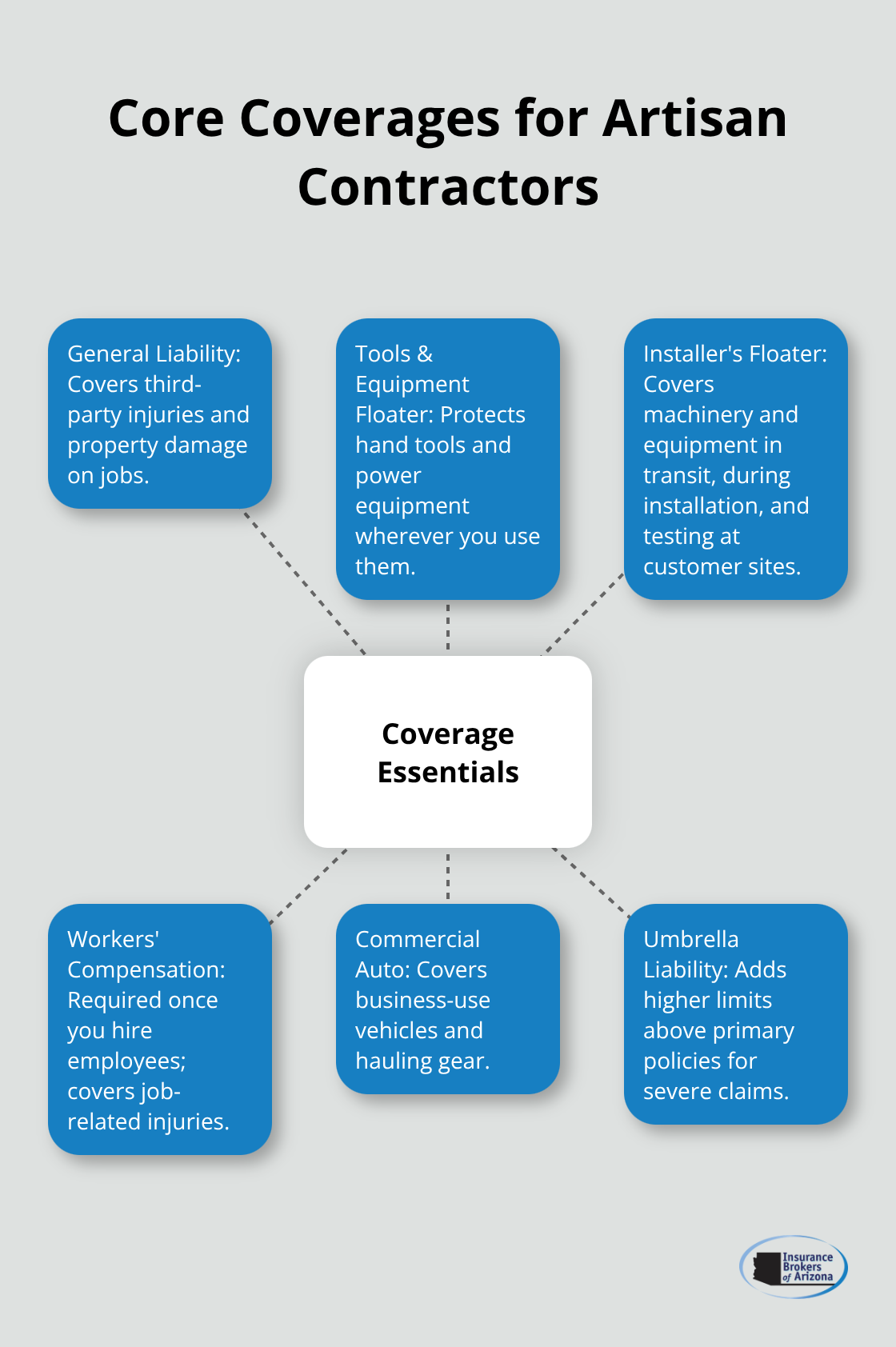

General Liability Protects Your Bottom Line

General liability insurance protects you when someone gets hurt at your job site or your work damages their property. For electricians, this typically costs $85 to $150 per month for small businesses, while self-employed electricians pay about $300 to $500 annually. Roofers face higher premiums at $150 to $300 monthly because working at heights creates serious injury risks. Plumbers average $75 to $140 per month, and carpenters fall somewhere in between. These costs reflect real hazard differences, not arbitrary pricing.

Most standard policies offer $1 million per occurrence and $2 million aggregate limits, but you can increase these if your projects warrant it. Arizona doesn’t impose unique general liability requirements beyond what federal law expects, so your focus should be on matching coverage limits to your actual job scope rather than purchasing a one-size-fits-all policy.

Tools and Equipment Need Real Protection

Tools stolen from a job site or damaged during transport create serious cash-flow problems. Standard property insurance won’t cover equipment moving between locations, which is exactly where artisan contractors lose money. An installer’s floater covers your machinery and equipment during transit, installation, and testing at customer premises. A tools and equipment floater covers hand tools, power drills, hoisting machines, and power pumps wherever you use them.

These aren’t optional add-ons if you move equipment regularly. They address the gaps that standard policies leave open, protecting your most valuable assets on the job.

Workers’ Compensation Thresholds in Arizona

Workers’ compensation requirements in Arizona kick in once you hire three or more employees, and violations trigger substantial penalties. For electrical contractors, workers’ comp averages around $217 monthly because ladder falls and electrical shocks create expensive claims. Roofing has the highest workers’ comp costs due to fall exposure. If you operate as a solo contractor, you can skip workers’ comp in most cases, but hiring even one employee changes everything.

Contact the Arizona Department of Insurance and Financial Institutions before expanding your team to confirm current thresholds and compliance requirements. Understanding these rules upfront prevents costly mistakes later.

How Coverage Costs Align with Your Trade

Your premium reflects the specific hazards your trade creates. Electricians face fire and shock risks, roofers confront fall dangers, and plumbers deal with water-damage exposure. A new business typically pays more until you establish a solid safety and claims history. Location also matters-Arizona’s regulatory environment differs from states like California or New York, which affects your overall costs.

The next step involves gathering the right information about your operations so you can request accurate quotes from multiple carriers and actually compare what you’re getting for your money.

Getting Quotes That Actually Compare

Document Your Business Operations First

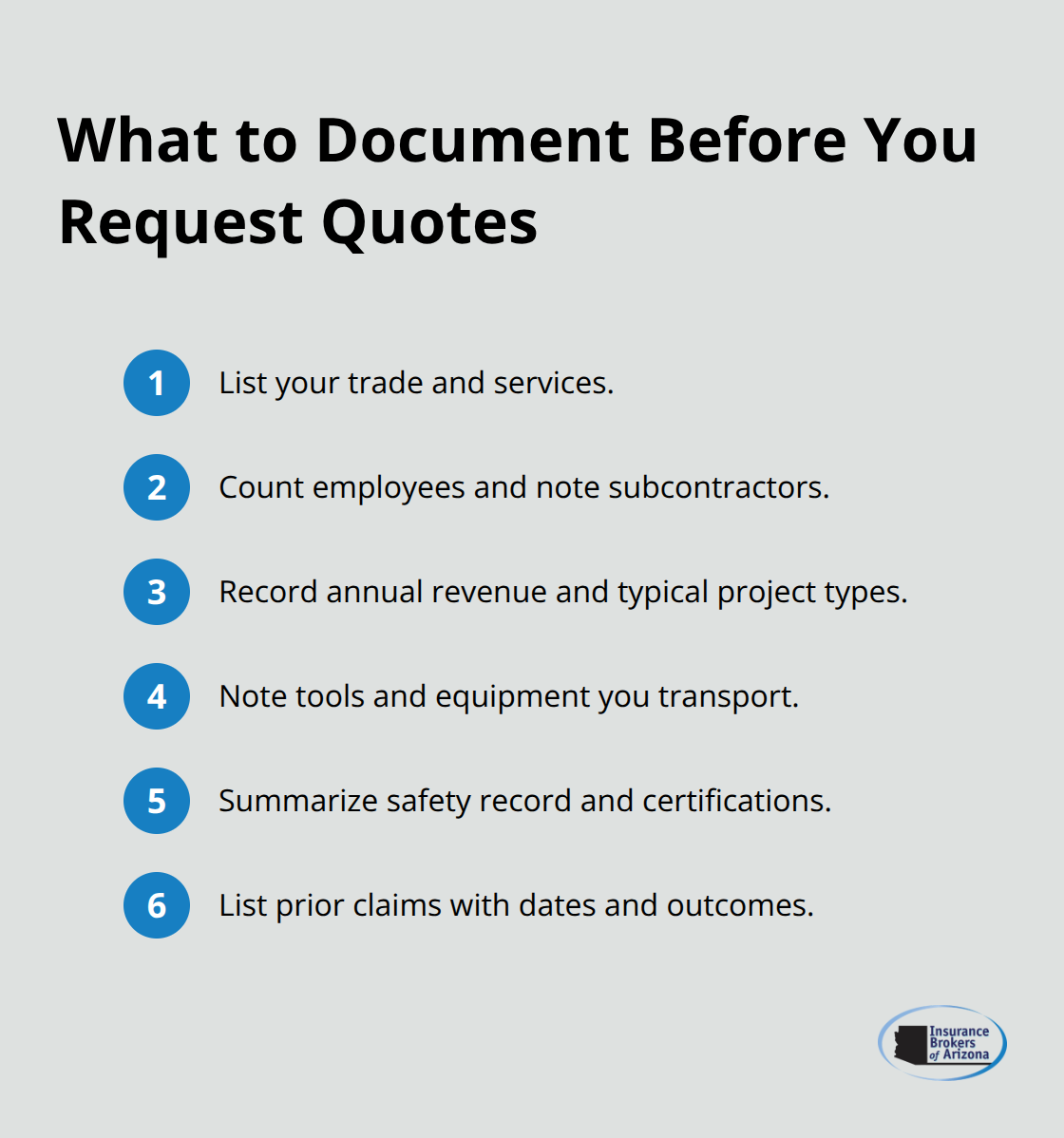

Collecting quotes from multiple carriers takes work, but skipping this step costs you real money. Start by documenting your business operations in writing before contacting any insurer. Write down your specific trade (electrician, roofer, plumber, carpenter), the number of employees you have, annual revenue, the types of projects you typically handle, whether you hire subcontractors, and which tools or equipment you transport between jobs.

Include details about your safety record and any previous claims. Insurers use these specifics to calculate premiums, so vague information produces vague quotes that don’t reflect your actual risk.

Request Quotes from Multiple Carriers at Once

Request quotes from at least three carriers simultaneously rather than shopping one at a time, since pricing and coverage terms shift constantly. When you contact carriers or brokers, ask each one for quotes with identical coverage limits so you can compare apples to apples. Request $1 million per occurrence and $2 million aggregate limits for general liability unless your projects demand higher coverage. Specify the exact floaters you need-installer’s floaters for equipment in transit and at customer sites, tools and equipment floaters for hand tools and power equipment. Ask whether workers’ compensation is included if you have employees, and confirm whether the quote includes any endorsements like professional liability if your work involves design responsibilities.

Build a Comparison Spreadsheet

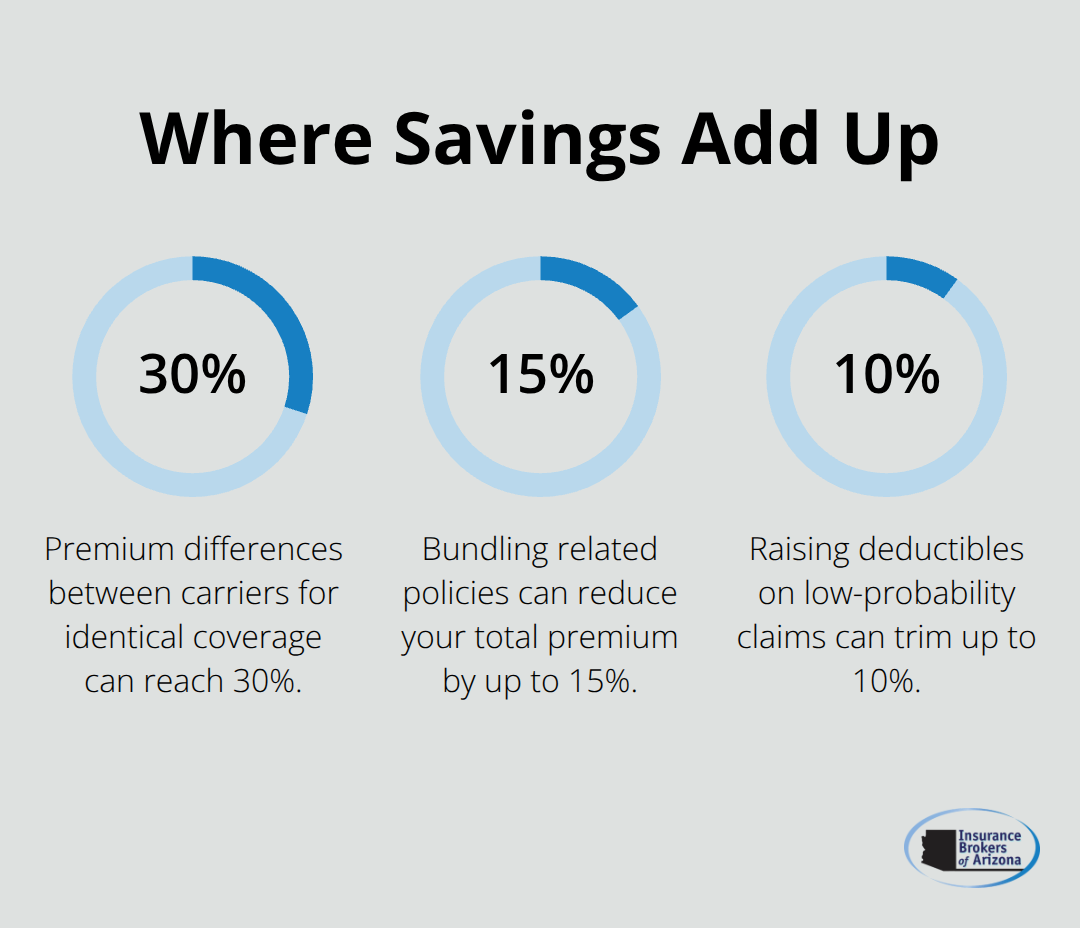

Once you have quotes in hand, the comparison becomes mechanical. Create a simple spreadsheet with each carrier’s name, total monthly premium, general liability limits, what floaters are included, deductible amounts, and any exclusions specific to your trade. Premium differences of 20 to 30 percent between carriers are common for identical coverage, which means comparing quotes literally saves thousands annually. Pay close attention to deductibles-a $500 deductible versus a $1,000 deductible changes your out-of-pocket costs when a claim happens.

Identify Bundling Discounts and Safety Credits

Ask each carrier about bundling discounts if you need commercial auto coverage, umbrella liability, or business property insurance alongside your general liability and tools coverage. Bundling can reduce your total premium by 10 to 15 percent compared to buying policies separately. Check whether each carrier offers premium reductions for safety certifications, completed safety training, or a claims-free history, since these discounts vary widely.

Time Your Quote Requests Strategically

Request your quotes within a single week so the pricing reflects the same market conditions. Insurance Brokers of Arizona® partners with over 40 carriers, which means you can access a wider range of options than shopping independently. Make your decision based on which carrier offers the best combination of coverage, deductibles, and price for your specific trade and risk profile-but the real savings come from understanding what each policy actually covers and how it protects your operations.

How to Actually Save Money on Artisan Contractor Insurance

Bundle Policies to Cut Your Total Premium

Combining your general liability, tools coverage, workers’ compensation, and commercial auto into a single policy cuts your total premium by 10 to 15 percent compared to purchasing each separately. A masonry contractor who bundled liability, tools, and auto coverage saved approximately 20 percent on combined premiums. When you request quotes, ask each carrier about bundling discounts and request a bundled quote alongside individual policy quotes so you can see the actual dollar savings. Some carriers offer larger discounts for bundling than others, which is why comparing bundled quotes from at least three carriers matters. Carriers like Next Insurance and Thimble now offer hourly, daily, or monthly coverage options that let you pay only for the time you actually work, which saves money if you take seasonal breaks or juggle multiple part-time contracts.

Safety Records Lower Your Premiums Directly

Carriers reduce premiums for contractors who complete safety training certifications, maintain documented safety protocols on job sites, and stay claims-free. A contractor with a clean claims history pays substantially less than one with prior claims because insurers view you as lower risk. Arizona contractors should document their safety practices in writing, including equipment maintenance schedules, job-site safety briefings, and incident reporting procedures. Ask each carrier what specific safety certifications or programs qualify for discounts during your quote request phase. Workers’ compensation costs drop noticeably when you implement fall-prevention systems if you work at heights, electrical-safety protocols if you’re an electrician, or water-damage prevention procedures if you’re a plumber. These aren’t just risk-reduction strategies; they directly translate to lower monthly premiums.

Annual Reviews Prevent Overpaying Year After Year

You should review your coverage annually because your risk profile changes as your business grows. If you hired your first employee this year, your workers’ compensation costs will shift. If you added roofing work to your carpentry business, your general liability premium should adjust upward to reflect the new hazard.

Carriers adjust pricing annually, and shopping every two years catches rate increases before they compound. When you review coverage, ask whether you still need every floater or endorsement you’re paying for. A contractor who stopped transporting equipment between job sites no longer needs an installer’s floater but might continue paying for it if they don’t review their policy. Increasing deductibles on low-probability claims can trim 5 to 10 percent from your premium without reducing meaningful protection.

Final Thoughts

Comparing artisan contractor insurance quotes from multiple carriers saves you thousands of dollars annually, but only if you take the process seriously. You now understand what coverage protects your business, how to gather accurate information before requesting quotes, and where bundling and safety improvements create real savings. The difference between accepting one quote and comparing three or more typically amounts to substantial money, which is why this work pays off.

Working with Insurance Brokers of Arizona® changes the equation significantly because we partner with over 40 carriers and access far more pricing options than you could find independently. We compare quotes on your behalf, identify bundling opportunities you might miss, and explain what each policy actually covers in plain language. This matters because artisan contractor insurance quotes can look identical on the surface while differing substantially in what they protect.

Document your business operations, including your trade, employee count, annual revenue, project types, and equipment you transport, then contact us to request quotes from multiple carriers simultaneously. After you secure coverage, mark your calendar for an annual review since your risk profile changes as your business grows and carriers adjust pricing constantly. The contractors who save the most money compare quotes regularly and adjust coverage as their operations evolve.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.