Commercial Truck Insurance: The Complete Guide

Running a commercial truck fleet means managing serious financial risks. One accident or cargo loss can cost thousands-or even shut down your operation.

At Insurance Brokers of Arizona®, we’ve helped countless trucking companies find the right coverage. This guide covers commercial truck insurance 101, from liability and physical damage to cargo protection and policy selection.

What Your Truck Insurance Actually Protects

Liability Coverage: Your Legal Foundation

Liability coverage is legally mandatory, and the FMCSA sets minimum requirements that vary by cargo type and operating authority. If you haul general freight interstate, you need a combined single limit of $750,000, though hazmat or specialized cargo can push requirements to $1,000,000 or higher depending on your routes and shipper contracts. This coverage pays for injuries to other people and damage to their property when you’re found at fault-medical bills, lost wages, legal defense, and settlements all fall under this umbrella. However, liability doesn’t cover damage to your own truck, so you need physical damage coverage to protect your equipment.

Physical Damage: Protecting Your Assets

Physical damage comes in two forms: collision covers accidents and rollovers, while comprehensive handles theft, fire, vandalism, and weather. For a $120,000 tractor, you’ll pay 3 to 6 percent of its stated value annually, which translates to roughly $3,600 to $7,200 per year according to FreightWaves Checkpoint data. Newer trucks cost more to insure because repair bills are steeper, so a 2019 Freightliner might run around $4,000 annually for physical damage at a 4 percent rate, whereas an older unit could be cheaper. Your deductible strategy matters here-raising it from $1,000 to $5,000 can slash premiums by 8 to 20 percent, but only if your cash reserves can absorb that out-of-pocket hit.

Cargo and Specialized Coverage

Cargo coverage protects the freight you haul from theft, damage, or loss in transit, with typical minimums starting at $100,000 but scaling up for high-value loads. Brokers and shippers often require specific cargo limits in their contracts, so match your coverage to actual load values rather than over-insuring cheap freight and paying unnecessary premiums. General liability covers off-duty incidents like damage to a customer’s loading dock during unload operations, separate from your auto liability policy. Non-trucking liability, sometimes called bobtail coverage, kicks in when your tractor operates without a trailer or dispatch-this is essential if you move the truck for personal reasons or position it between loads. Motor truck general liability typically runs $750,000 to $1,000,000 and is often required by states and risk managers.

Real-World Cost Expectations

For owner-operators with clean driving records and three or more years of loss-free operations, total annual insurance costs usually range from $12,000 to $25,000 per power unit according to FreightWaves Checkpoint, though new entrants or hazmat specialists pay significantly more. Your policy stack should reflect your actual operations-routes, cargo types, vehicle values, and how you use the truck dictate what you truly need. The right coverage combination protects your business from catastrophic losses while keeping premiums aligned with your real risk profile. Understanding these coverage types sets the stage for selecting the right policy mix, which depends on your fleet size, operating radius, and specific operational demands.

Types of Commercial Truck Insurance Policies

General Liability Covers Off-Vehicle Incidents

General liability protects your operation when incidents happen away from the road-damage to a customer’s dock during loading, injuries on their property, or accidents in your yard. This coverage typically carries limits of $1 million per occurrence and $2 million aggregate according to industry standards. It operates separately from your auto liability policy and shields your business from lawsuits arising from operations beyond driving. Many carriers bundle general liability into a commercial auto package, which simplifies administration, while others sell them separately and give you flexibility to adjust limits independently.

Commercial Auto Insurance Forms Your Primary Layer

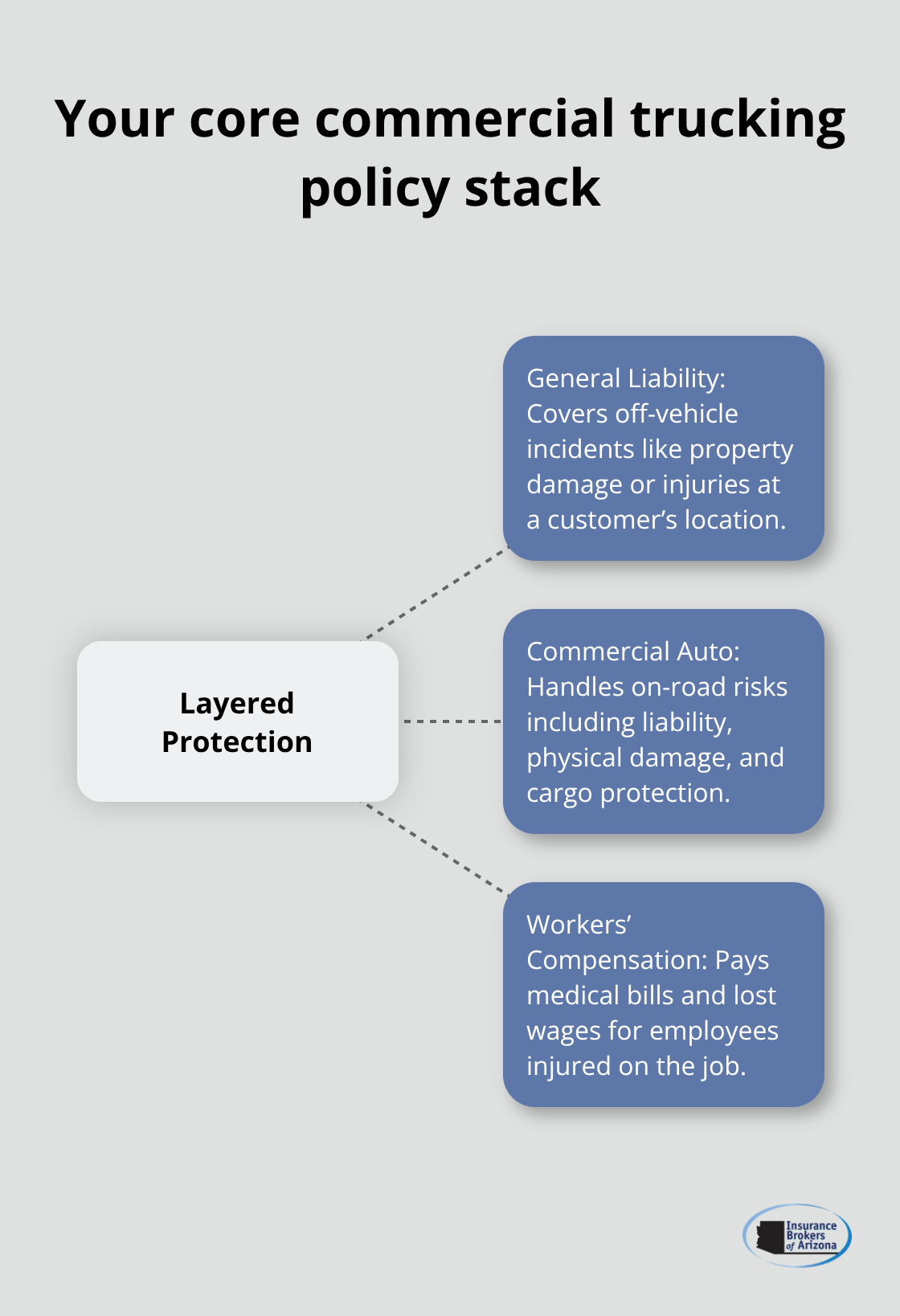

Commercial auto insurance includes the liability, physical damage, and cargo protections that form your core coverage. Your limits must meet FMCSA requirements and often exceed them based on shipper contracts and the specific routes you operate. This policy handles the majority of your on-road risk exposure and represents the largest component of your total insurance spend. The structure of your commercial auto policy determines how much you pay and what gaps exist in your overall protection strategy.

Workers’ Compensation Protects Your Team

Workers’ compensation is legally required in most states and covers medical expenses and lost wages for employees injured on the job, whether they’re in the truck or at your facility. Premiums scale with payroll and claims history, typically ranging from $800 to $2,000 annually per employee in trucking depending on your state and safety record. A solo owner-operator with no employees doesn’t need this coverage, but someone running five trucks with drivers absolutely does. Review your workers’ compensation classification annually to confirm accuracy and avoid overpaying for misclassified positions.

How These Policies Work Together

These three policy types aren’t optional add-ons-they’re mandatory components that work together to shield your business from different angles of risk. New entrants often overspend by purchasing identical limits across all three policies without matching them to actual exposure. Try aligning your general liability limits to match your commercial auto limits when possible, and drop coverage you genuinely don’t need rather than paying for blanket protection.

This targeted approach reduces waste while maintaining the layered defense your operation requires.

Your next step involves assessing your specific fleet size and operating radius to determine which coverage limits actually fit your business model.

How to Size Coverage and Compare Quotes

Map Your Operating Radius and Fleet Reality

The gap between under-insuring and over-insuring often comes down to one question: what does your operation actually look like day-to-day? A five-truck local delivery fleet operating within a 100-mile radius faces fundamentally different risks than a single owner-operator running hazmat across state lines, yet many operators apply generic coverage limits to both scenarios. Start by mapping your actual operating radius on paper-not the maximum distance you could theoretically travel, but where you realistically spend 80 percent of your time. Operating radius directly impacts your premium; a carrier running primarily within Arizona pays less than one covering the Southwest, and that carrier pays less than a cross-country operation.

Next, count your trucks and drivers honestly. A fleet of five vehicles with three full-time drivers and two part-time drivers requires different workers’ compensation classifications and general liability exposure than a solo owner-operator. Your fleet size also affects how underwriters view you-larger fleets with standardized hiring and training programs often qualify for fleet credits that reduce per-unit costs by 10 to 15 percent according to FreightWaves Checkpoint data. Document your cargo types as well. Hauling refrigerated food differs fundamentally from hauling dry goods or construction materials, and hazmat cargo can triple your premium compared to non-hazardous freight.

Align Limits to Contracts and Actual Load Values

Shippers will dictate minimum coverage limits in their contracts anyway, so pull those agreements and use them as your baseline rather than guessing. Your liability limits must meet FMCSA minimums, but shipper contracts often demand $1,000,000 or higher combined single limits regardless of what federal law requires-check your actual contracts before locking in limits. For cargo coverage, match your limit to what you actually haul, not worst-case scenarios. If your typical load value runs $40,000 to $60,000, a $100,000 cargo limit is sufficient-paying premiums for $250,000 coverage you’ll never use is waste.

Optimize Deductibles for Your Cash Position

Physical damage deductibles merit serious attention: raising your deductible from $1,000 to $2,500 typically saves 8 to 12 percent on premiums, and jumping to $5,000 can save 15 to 20 percent if your cash reserves can absorb that hit in an emergency. The math works only if you can actually pay that deductible without crippling operations. Higher deductibles reduce your insurer’s risk exposure, which translates directly to lower premiums for you.

Demand Apples-to-Apples Comparisons

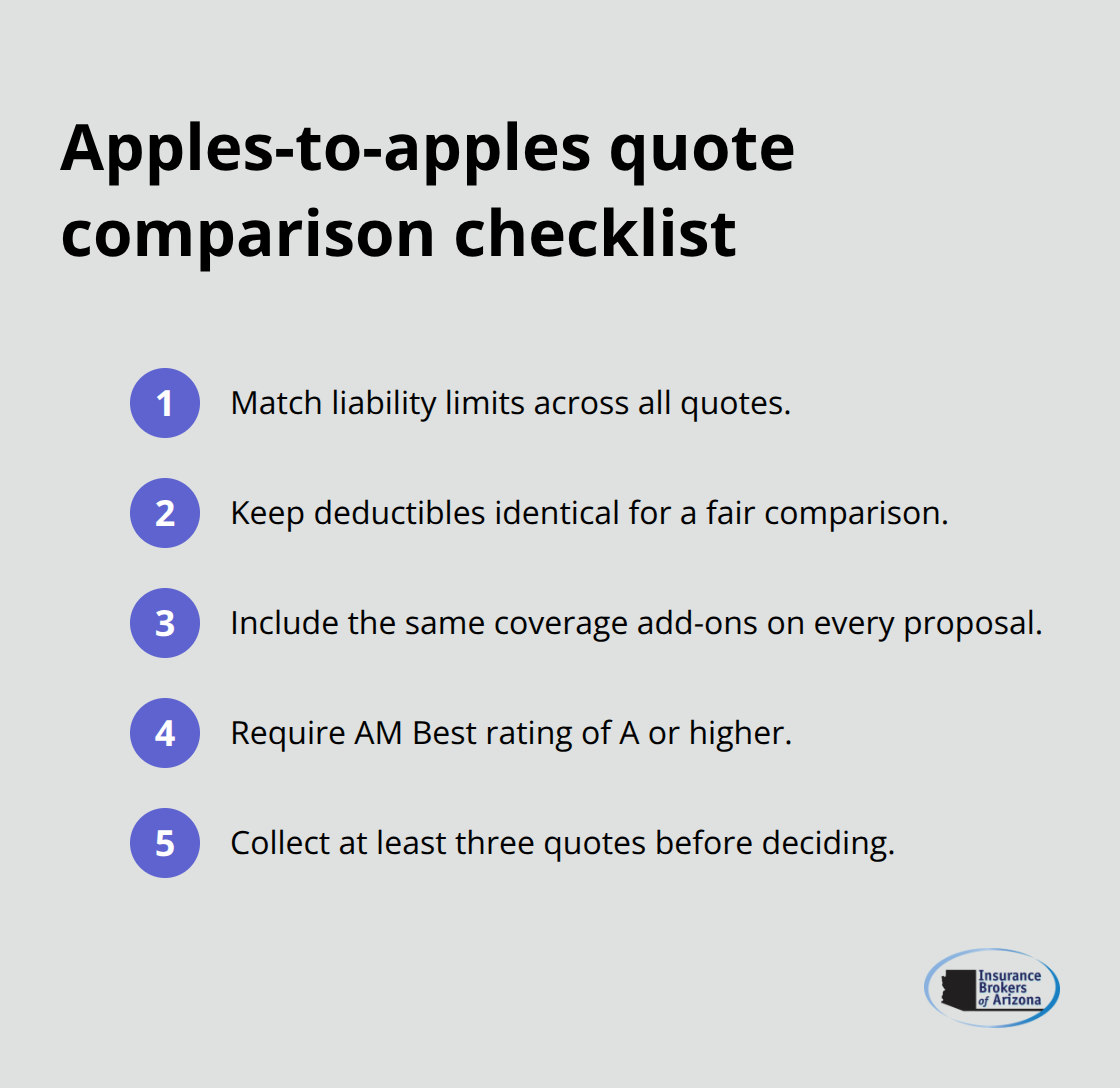

When comparing quotes from different carriers, demand identical liability limits, identical deductibles, and identical coverage add-ons across all proposals. A $12,000 quote with a $2,500 deductible is not comparable to a $10,500 quote with a $500 deductible. Carrier ratings matter more than you might think. Stick with insurers rated A or higher by AM Best-this rating reflects financial strength and claims-paying ability.

A cheaper premium from a carrier with a C rating evaporates instantly if they deny a major claim or lack reserves to pay it.

Gather Multiple Quotes and Leverage Discounts

Gather at least three quotes before deciding, and specifically ask about telematics discounts (typically 5 to 10 percent savings for dash cam or GPS safety monitoring) and multi-policy bundling. Insurance Brokers of Arizona® works with over 40 carriers to access competitive quotes tailored to trucking operations, ensuring you see real options rather than whatever one agent happens to offer.

Final Thoughts

Commercial truck insurance 101 requires you to match coverage limits to shipper contracts and FMCSA requirements rather than applying generic numbers across the board. Liability coverage protects you legally, physical damage covers your trucks, and cargo protection matches what you actually haul-these three layers form your complete defense against operational risk. Your deductible strategy directly impacts premiums; raising physical damage deductibles from $1,000 to $5,000 cuts costs by 15 to 20 percent if your cash reserves support that out-of-pocket expense.

Carrier financial strength matters far more than the lowest quote on the table. An A-rated insurer from AM Best will actually pay claims when you need them, while telematics programs and clean driving records yield real savings of 5 to 10 percent that you can document and leverage at renewal. Gather three or more proposals with identical limits, deductibles, and coverage add-ons so you can compare apples to apples across all carriers.

We at Insurance Brokers of Arizona® work with over 40 carriers to deliver competitive quotes tailored specifically to trucking operations, cutting through the noise to show you real options that fit your fleet. Pull your shipper contracts to confirm minimum coverage requirements, document your actual operating radius and cargo types, and be honest about your fleet size and driver experience. Contact us today to discuss your coverage needs and lock in rates that protect your business without overpaying for protection you don’t need.