HVAC Contractor Insurance Arizona: What You Need to Know

Running an HVAC business in Arizona means managing real risks every day. From equipment damage to employee injuries, one accident can threaten your entire operation.

At Insurance Brokers of Arizona®, we’ve helped countless contractors understand what HVAC contractor insurance coverage actually protects them. This guide walks you through the policies you need, how to pick the right coverage, and what Arizona requires.

The Three Core Coverages Every Arizona HVAC Contractor Must Have

General Liability: Your First Line of Defense

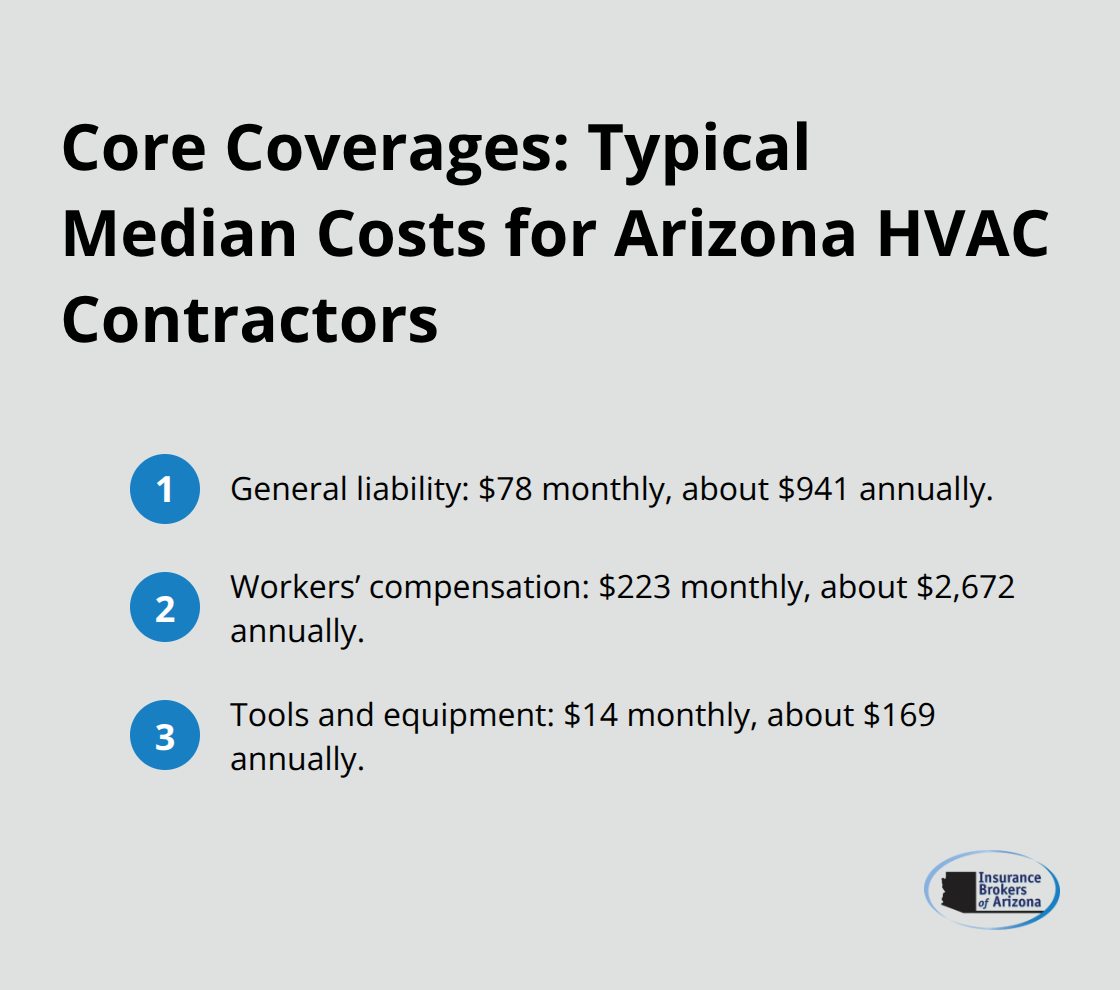

General liability insurance protects you when your work causes bodily injury or property damage to someone else. A technician punctures a homeowner’s wall while installing ductwork, or an air conditioning unit falls during rooftop installation-general liability covers the medical bills, repair costs, and legal defense. According to TechInsurance data, HVAC contractors pay a median of $78 monthly for general liability, which translates to roughly $941 per year. Most policies include $1 million per occurrence and $2 million aggregate limits with a $500 deductible.

The coverage also includes completed operations protection, meaning you stay covered for problems that emerge after you finish the job. HVAC systems sometimes develop issues weeks or months later, and clients may return with damage claims. Many Arizona homeowners and commercial property managers now require proof of general liability before they hire any contractor, making this policy essential for landing jobs.

Workers’ Compensation: A Legal Requirement in Arizona

Workers’ compensation is mandatory in Arizona if you have even one employee on payroll. The Arizona Department of Insurance enforces this requirement strictly. The coverage pays medical expenses, rehabilitation costs, and lost wages for employees injured on the job, and it also protects you from lawsuits by covering employer’s liability.

TechInsurance reports that HVAC contractors pay a median of $223 monthly, or approximately $2,672 annually, though costs vary based on your payroll size and claims history. A clean safety record directly reduces your premiums, so investing in worker training and jobsite safety practices pays off. Your team stays safer, and your bottom line improves.

Tools and Equipment: Protecting Your Investment

Equipment and tools represent significant investments for HVAC contractors, and protecting them requires dedicated coverage. Tools and equipment policies cover theft, vandalism, and damage to portable tools and machinery worth under $10,000 and typically under five years old. The median monthly cost is $14, or $169 annually. This coverage keeps your jobs moving forward when tools are stolen from a jobsite or damaged during transport.

Arizona’s extreme heat, dust storms, and monsoons increase the risk of equipment damage, making this coverage particularly valuable in the state. Your equipment faces constant exposure to harsh conditions, and one major loss can halt operations for days or weeks.

Building Your Foundation

These three coverages form the foundation that protects your business, keeps you legally compliant, and gives clients confidence in hiring you. With general liability, workers’ compensation, and equipment protection in place, you’ve addressed the most common risks HVAC contractors face in Arizona. The next step involves understanding the specific policy types available and how they differ in scope and cost.

Policy Types That Protect Your HVAC Business

Commercial general liability insurance addresses the specific risks that plague HVAC contractors in Arizona. A $1 million per occurrence limit with a $2 million aggregate protects you against the scenarios that happen regularly on job sites. Rooftop unit installations expose you to fall hazards and roof damage claims. Evaporative cooler work introduces water-damage liability that standard policies often exclude. TechInsurance data shows HVAC contractors pay around $941 yearly for general liability, but this figure assumes standard residential work. Commercial systems in hospitals or manufacturing facilities carry different risk profiles and command higher premiums. You need coverage that explicitly addresses products-completed operations because HVAC systems fail weeks or months after installation.

A refrigerant leak damages a client’s property. An improperly sealed ductwork causes mold growth. A thermostat malfunction leads to frozen pipes. These scenarios demand protection that extends far beyond the job completion date. Many Arizona contractors choose the lowest premium without examining what’s actually covered. A $500 deductible sounds reasonable until you face a $3,000 claim and realize your policy excludes that specific scenario.

Tools and Equipment Coverage Keeps Operations Running

Tools and equipment coverage fills a critical gap that general liability ignores. Your portable tools, ladders, and diagnostic equipment represent your ability to work, yet standard policies won’t touch them. TechInsurance reports this coverage costs only $14 monthly or $169 annually, making it one of the cheapest investments you’ll make.

Arizona’s environment accelerates equipment deterioration and theft. Tools left on roofs during installations vanish in seconds. Equipment stored in trucks gets damaged by flying debris during monsoons. Extreme heat, dust storms, and monsoons create constant threats to your gear. This coverage protects your investment and keeps jobs moving forward when tools are stolen or damaged.

Commercial Auto Insurance Covers Arizona-Specific Risks

Commercial auto insurance becomes essential the moment you use a company vehicle for HVAC work. TechInsurance data shows contractors pay approximately $191 monthly or $2,292 annually for commercial auto coverage. This policy covers liability if your van causes an accident while transporting equipment or a technician. It also protects you if an employee drives their personal vehicle for work-related tasks through hired and non-owned auto coverage.

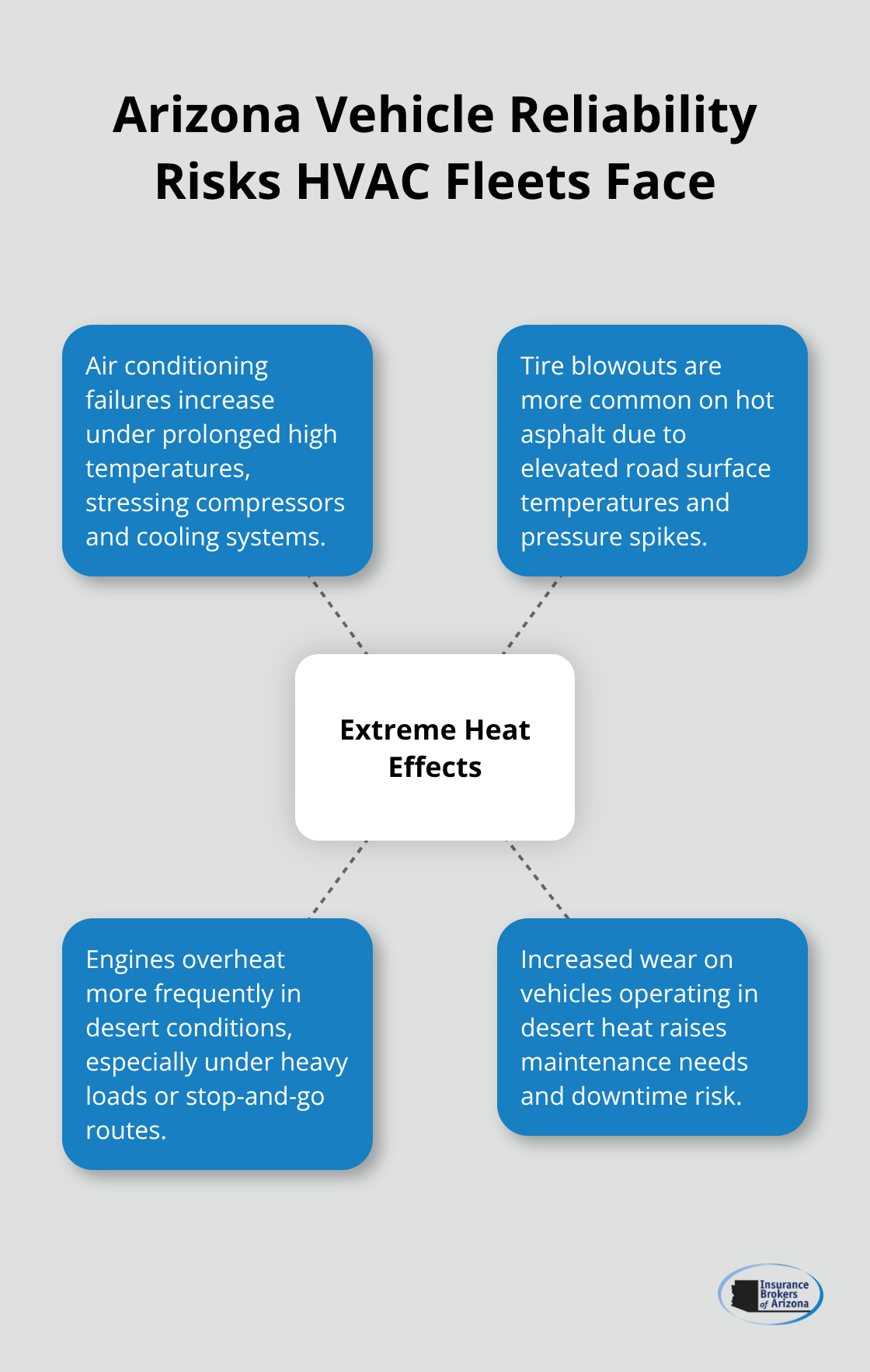

Arizona’s extreme heat affects vehicle reliability in ways contractors outside the state rarely experience. Air conditioning failures, tire blowouts from hot asphalt, and overheating engines happen frequently. Your commercial auto policy must account for these Arizona-specific conditions and the increased wear on vehicles operating in desert heat.

Bundling Policies Reduces Your Overall Costs

Many contractors bundle these three policy types together, which reduces overall costs significantly compared to purchasing separately. A business owner’s policy combines general liability with commercial property coverage at a median cost of $124 monthly or $1,493 annually. This approach delivers better value than standalone policies for smaller operations. When you combine general liability, workers’ compensation, and commercial auto into one package, you often qualify for additional discounts that lower your total premium burden.

The right combination of policies protects your equipment, your team, and your liability exposure. Understanding which coverages work together and which ones address specific Arizona risks positions you to make informed decisions about your protection strategy. The next step involves assessing your unique business situation and comparing what different insurers actually offer.

Choosing Coverage That Matches Your Arizona HVAC Operation

Your business size, service offerings, and claims history directly determine which policies you actually need and what you’ll pay. A solo technician with no employees faces entirely different risks than a five-person crew installing commercial systems in Phoenix hospitals.

Identify Your Specific Services and Risk Exposure

Start by listing every service your company provides. Do you install rooftop units, evaporative coolers, or both? Do you handle commercial projects or stick to residential work? Do you employ technicians or operate as a sole proprietor? Each service type carries distinct liability exposure.

Rooftop installations require fall protection coverage and roof damage liability. Evaporative cooler work introduces water damage exposure that many standard policies explicitly exclude. Commercial installations in manufacturing or healthcare facilities demand higher coverage limits than residential jobs. Once you’ve identified your specific services, calculate your annual payroll and equipment value. These numbers directly affect your workers’ compensation and equipment coverage costs.

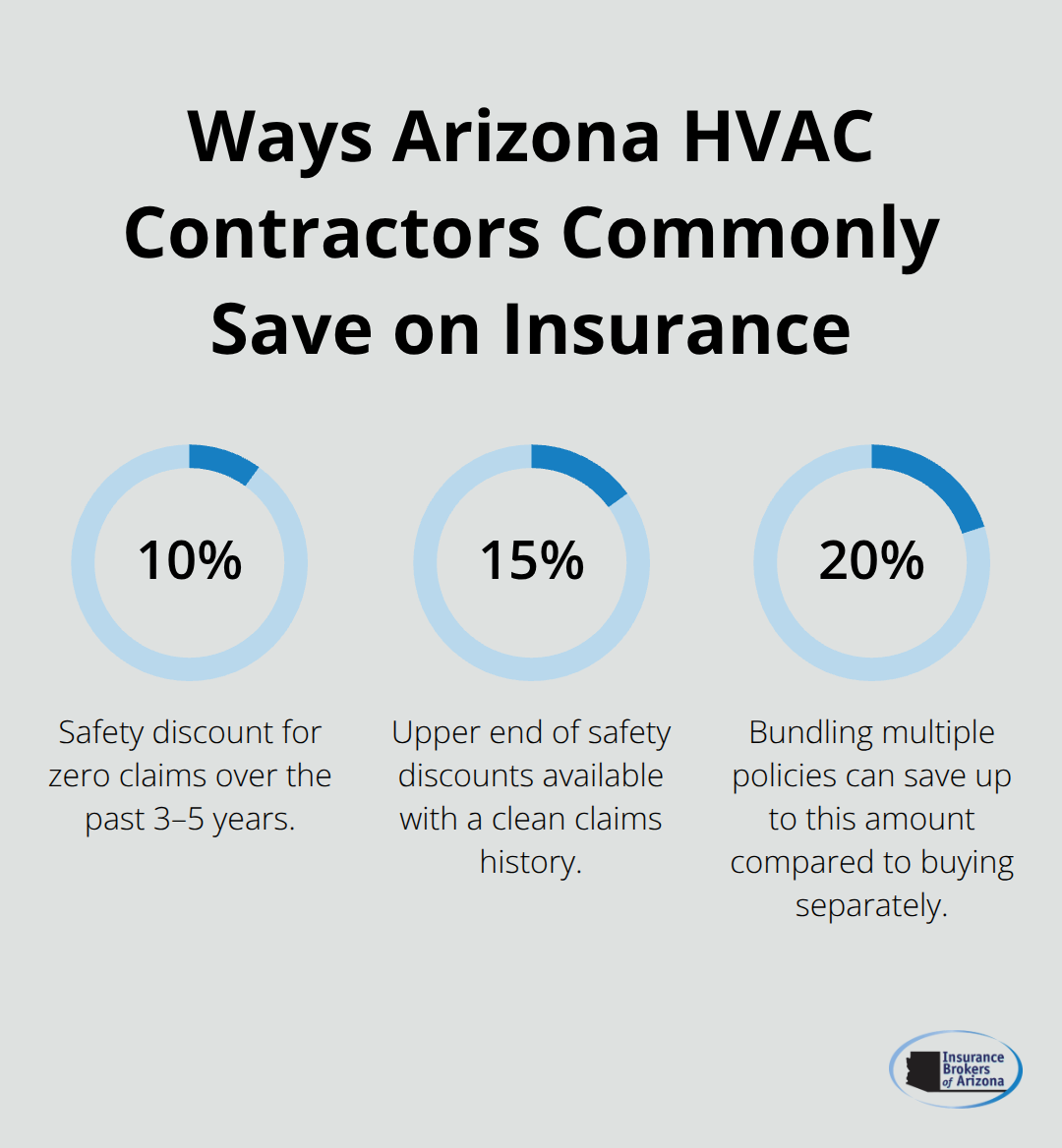

A contractor with $200,000 annual payroll pays significantly more for workers’ comp than one with $50,000, but the difference is predictable and quantifiable. Next, review your claims history over the past three to five years. Contractors with zero claims qualify for safety discounts that can reduce premiums by 10 to 15 percent.

Calculate Your Expected Insurance Costs

Arizona contractors typically pay between 1.3 and 2.6 percent of annual gross revenue for liability insurance, according to industry data. A business with $150,000 annual revenue might expect to pay around $3,140 annually across all coverages, though this varies by risk profile and claims history.

These figures provide a realistic baseline for budgeting your insurance expenses. Your actual costs depend on the specific coverage limits you select and the deductibles you choose. Understanding this range helps you evaluate quotes from different carriers and spot outliers that don’t match market rates.

Request Quotes and Compare Coverage Details

Obtaining quotes from multiple insurers is non-negotiable because premium variation is substantial. One carrier might quote $2,500 annually for your general liability while another quotes $4,200 for identical coverage.

When you request quotes, ask each insurer exactly what their general liability policy covers and what it excludes. Specifically ask about products-completed operations coverage, rooftop installation protection, and water damage liability if those apply to your work. Request quotes that include bundled policies, which typically save 15 to 20 percent compared to purchasing each policy separately.

Compare the deductible options carefully. A $500 deductible versus $1,000 might save you $200 annually, but it increases your out-of-pocket cost when claims occur. For HVAC contractors in Arizona, the $500 deductible remains standard because claims happen regularly enough that higher deductibles create unacceptable financial risk.

Work with a Broker Who Understands HVAC Risks

Working with an insurance broker who specializes in HVAC contractor coverage matters more than many contractors realize. A general insurance agent may miss Arizona-specific risks like extreme heat damage to vehicles or monsoon-related equipment loss.

Insurance Brokers of Arizona® partners with over 40 reputable carriers and can match your specific operation with policies designed for HVAC contractors in your region. A broker explains policy exclusions in plain language, helps you understand what completed operations coverage actually means, and identifies discounts you might otherwise miss. They also handle certificate of insurance requests quickly when clients require proof of coverage before hiring you.

Most Arizona HVAC contractors can obtain instant quotes and same-day certificates through brokers, keeping projects on schedule without administrative delays. The right broker asks detailed questions about your business structure, equipment investments, and project types before recommending coverage, rather than simply selling the lowest-cost option available.

Final Thoughts

HVAC contractor insurance in Arizona protects your business from the specific risks you face every day. General liability, workers’ compensation, and equipment coverage form the foundation that keeps your operation running when accidents happen. These three policies address the scenarios that occur most frequently on Arizona job sites, from rooftop installations to equipment theft during monsoons. Your claims history directly affects your premiums, meaning a clean safety record translates to lower costs year after year.

Most Arizona HVAC contractors pay between 1.3 and 2.6 percent of annual gross revenue for liability coverage, giving you a realistic budget baseline. Request quotes from multiple carriers and compare what each policy actually covers, not just the premium price. Bundling your policies typically saves 15 to 20 percent compared to purchasing each one separately, so always ask about combined packages when you request quotes.

Working with an insurance broker who understands HVAC contractor insurance Arizona risks makes the entire process faster and more effective. A broker with experience in your industry identifies coverage gaps you might miss and explains policy exclusions in language that makes sense. Contact Insurance Brokers of Arizona® today to get personalized quotes that match your operation and secure competitive rates across all your coverage types.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.