How to Find Cheap Commercial Auto Insurance

Commercial auto insurance costs can drain your business budget faster than you think. The average small business pays $1,200 annually for commercial vehicle coverage, but smart strategies can cut these expenses significantly.

We at Insurance Brokers of Arizona® see businesses overpay for coverage daily. Finding cheap commercial auto insurance requires knowing where to look and what mistakes to avoid.

What Strategies Cut Commercial Auto Insurance Costs Most

The quickest path to lower premiums starts with aggressive comparison shopping across multiple carriers. The National Association of Insurance Commissioners data shows businesses can find price variances of 40% or more for identical coverage when they quote from at least five different insurers. Independent agents provide quotes from 15 to 20 carriers simultaneously, which gives you access to rates that captive agents (who represent single insurers) cannot match.

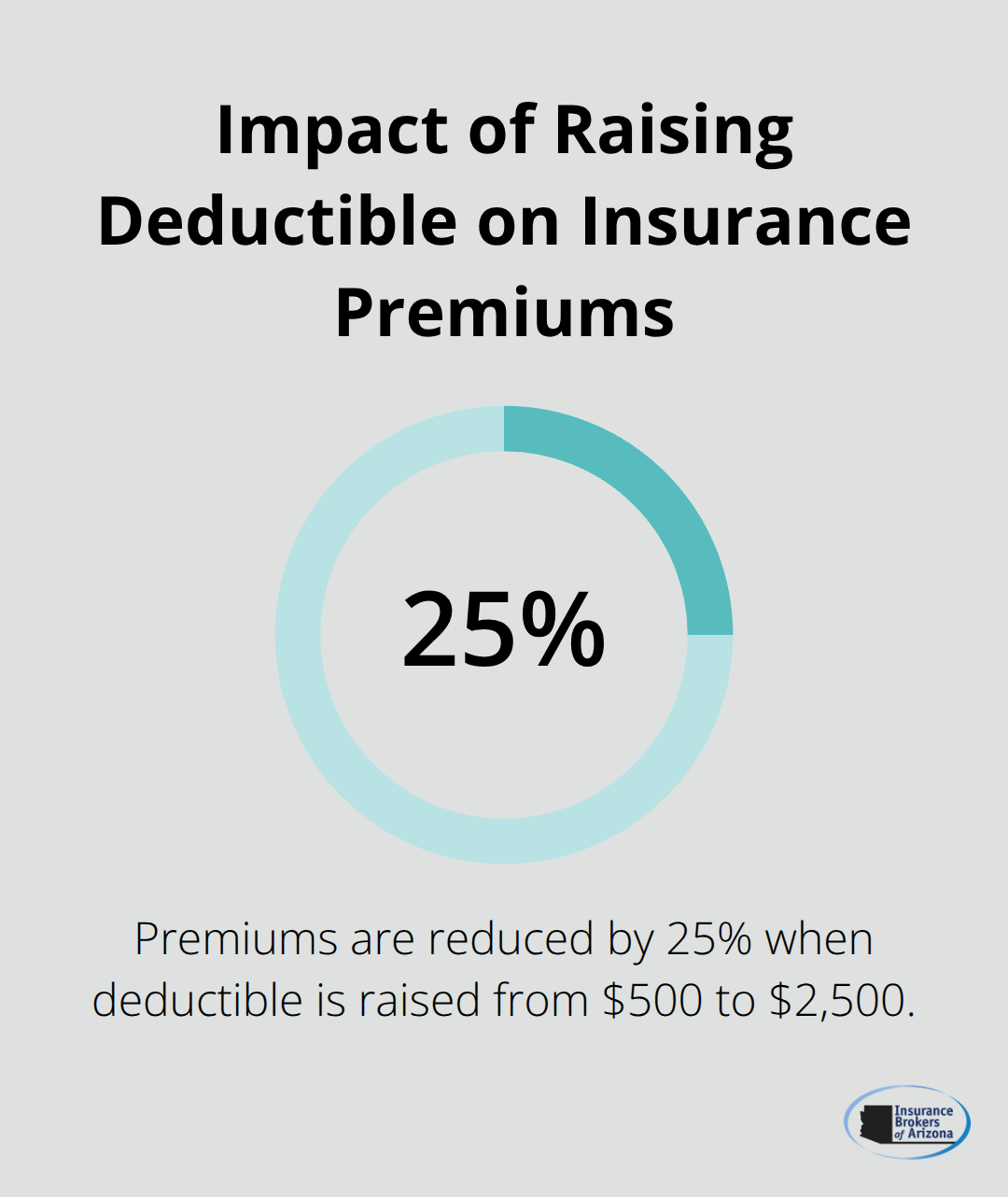

Smart Deductible Adjustments Slash Premium Costs

Raising your deductible from $500 to $2,500 typically reduces premiums by 25% according to industry data. For businesses with clean claims histories, pushing deductibles up to $10,000 can cut costs by 50% as the National Association of Insurance Commissioners reports. The key lies in maintaining enough cash flow to handle higher out-of-pocket expenses when claims occur.

Bundle Policies for Immediate Savings

Progressive’s research shows businesses save around 12% on auto insurance when they bundle it with property coverage. This multi-policy discount strategy works because insurers prefer customers who consolidate their coverage. The savings compound when you add general liability and workers compensation to the package (creating comprehensive business protection).

Annual Reviews Prevent Rate Creep

Companies that skip annual policy reviews pay premiums that average 12% above current market rates. Businesses that switch carriers every three years maintain more competitive rates than those who stay with one insurer long-term. The insurance market shifts constantly, and yesterday’s best rate becomes tomorrow’s overpriced policy without regular monitoring.

These cost-cutting strategies work best when you understand the specific factors that drive your premium calculations in the first place.

What Drives Your Commercial Auto Insurance Rates

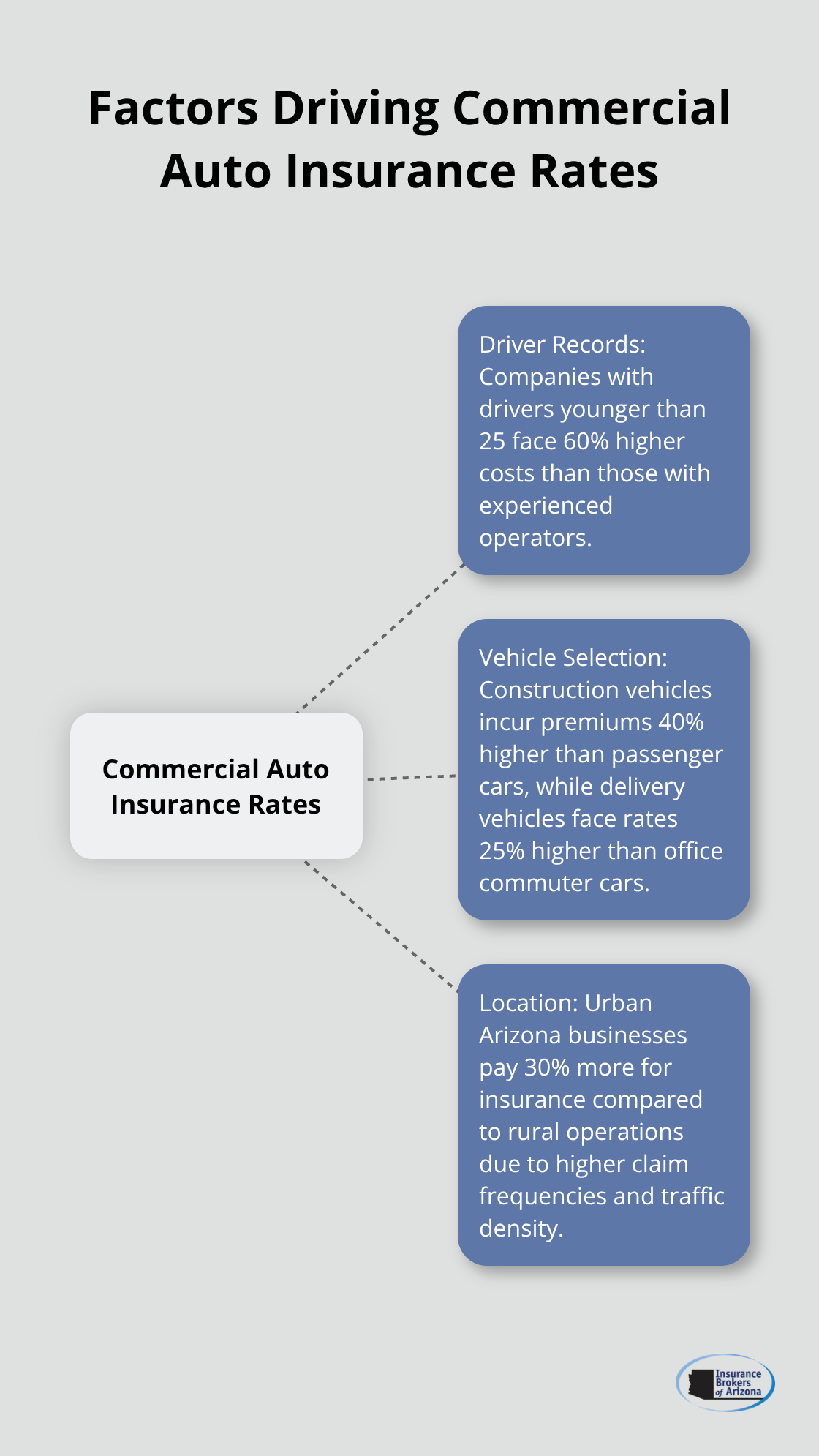

Your driver records create the foundation of your premium calculations, and the numbers tell a harsh story. Companies with drivers younger than 25 face costs that are 60% higher than those with experienced operators, according to Insurance Information Institute data. Clean records slash premiums by up to 35%, while accidents within the past three years add approximately $1,200 to annual insurance costs. The Federal Motor Carrier Safety Administration found that businesses that implement driver safety programs decrease accident rates by 40% within one year. Companies that train new hires for 40 hours reduce first-year accident rates by 60%, which makes comprehensive driver education a direct path to lower premiums rather than a nice-to-have expense.

Vehicle Selection Determines Base Premium Structure

Your vehicle choices dictate premium costs more than most business owners realize. Construction vehicles incur premiums that are 40% higher than passenger cars, while delivery vehicles face rates 25% higher than office commuter cars. Businesses that switch from cargo vans to standard sedans save approximately $800 per vehicle annually. Fleet technology reduces accidents by 30% and qualifies businesses for discounts that average 20% on insurance rates according to industry studies. The age and size of vehicles matter too – newer and larger vehicles command higher premiums, but their safety features often offset costs through available discounts.

Location and Coverage Limits Shape Final Costs

Urban Arizona businesses pay 30% more for insurance compared to rural operations due to higher claim frequencies and traffic density. Your coverage limits directly impact costs – businesses that reduce combined single limits from $300,000 to $100,000 decrease premiums significantly, though this strategy requires careful risk assessment. Replacement cost coverage costs 30% more than actual cash value coverage but provides full vehicle replacement without depreciation calculations (making it valuable for newer fleets). The key lies in matching your coverage limits to actual business risks rather than purchasing maximum coverage across all categories.

These rate factors work together to create your final premium, but many businesses unknowingly make costly mistakes that push their rates even higher than necessary.

What Costly Mistakes Drive Up Your Commercial Auto Insurance

Most businesses sabotage their own insurance costs through three expensive errors that compound over time. The first mistake involves purchasing minimal liability coverage to save money upfront, which backfires when lawsuits exceed policy limits. Businesses that carry only state minimum coverage face personal asset exposure when claims reach nuclear verdict territory – awards exceeding $10 million that have increased by 300% since 2010 according to the American Transportation Research Institute.

Minimal Coverage Creates Maximum Risk

Smart businesses carry at least $1 million in combined single limit coverage because the cost difference between minimum and adequate coverage averages just $200 annually per vehicle. The protection gap spans millions in potential exposure when businesses choose inadequate limits. Companies that select state minimums often discover their mistake too late when major accidents occur and legal settlements exceed their coverage caps.

Outdated Policy Information Triggers Premium Penalties

The second critical error involves failure to update policy details when business operations change. Companies that add vehicles without notifying insurers face coverage gaps that void protection entirely. Businesses that remove vehicles continue paying premiums for non-existent assets (wasting thousands annually on phantom coverage).

Driver additions create similar problems when new employees lack proper coverage notifications. This oversight can trigger policy cancellations after accidents occur. Annual revenue updates matter because insurers calculate exposure based on business size, and outdated information leads to incorrect premium calculations. The National Association of Insurance Commissioners found that businesses with current policy information pay 15% less than those with outdated details.

Wrong Provider Selection Costs Thousands Annually

The third mistake involves choosing insurers based on price alone rather than claims handling capability and industry expertise. Carriers with poor commercial auto experience delay claim payments and dispute coverage decisions, which creates cash flow problems during critical periods. GEICO maintains a high complaint rate according to the NAIC Company Complaint Index, making it a risky choice despite competitive pricing.

Businesses need insurers that understand commercial operations and provide 24/7 claim reporting because downtime costs exceed premium savings. Companies should match with insurers that specialize in their industry rather than accept one-size-fits-all solutions that fail when claims occur. Working with a local agent provides the expertise needed to navigate complex commercial coverage decisions.

Final Thoughts

Cheap commercial auto insurance becomes achievable when businesses apply systematic comparison strategies and maintain strong risk management practices. Data proves companies reduce premiums by 40% or more through aggressive quote collection from multiple carriers, strategic deductible adjustments, and policy bundling. Companies that establish driver safety programs and maintain clean records achieve the most significant long-term savings.

Experienced insurance professionals help businesses avoid costly coverage mistakes that drain budgets unnecessarily. We at Insurance Brokers of Arizona® connect you with competitive options from multiple reputable carriers. Our team helps you navigate complex coverage decisions while avoiding inadequate limits, outdated policy details, and poor provider selection.

Your next action involves collecting quotes from at least five different insurers while you evaluate current coverage requirements. Annual policy reviews prevent rate increases and maintain competitive rates as your business grows (smart businesses treat insurance as protection investment rather than expense minimization). Balance cost reduction with adequate coverage that protects against catastrophic losses.