Renters Insurance Arizona: Protecting Your Space

Your apartment is one of your most valuable assets, yet many renters in Arizona skip insurance altogether. Renters insurance Arizona protects your belongings and shields you from liability claims when accidents happen.

We at Insurance Brokers of Arizona® know that Arizona’s intense heat, monsoons, and rising crime create unique risks renters face daily. This guide walks you through what coverage you need and how to find the right policy for your situation.

What Your Renters Insurance Actually Covers

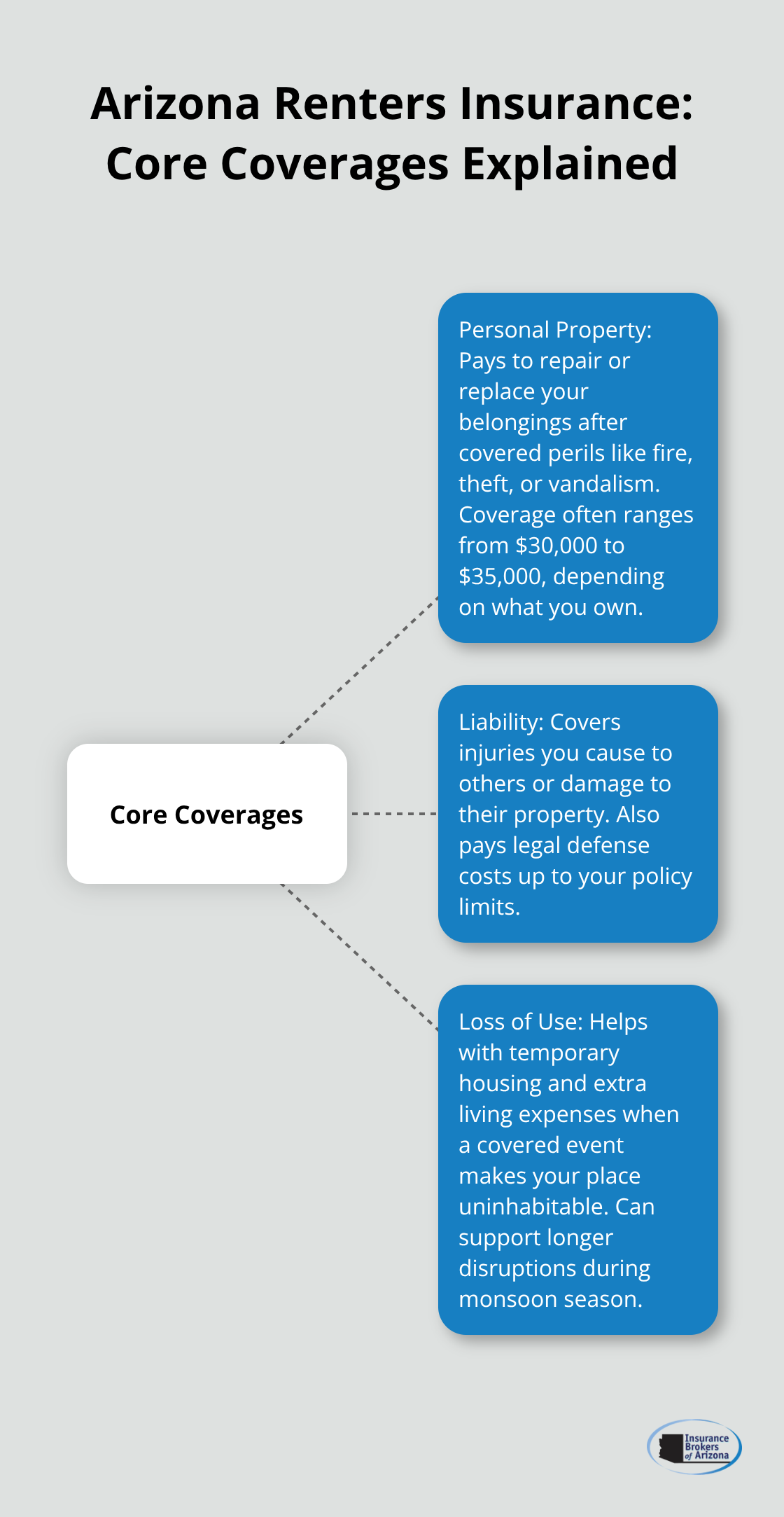

Personal property coverage forms the backbone of any renters policy in Arizona, protecting the items you own inside your rental unit. This coverage protects your belongings from common perils like fire, smoke, theft, vandalism, wind, hail, and lightning.

According to the National Association of Insurance Commissioners, renters in Arizona can obtain around $30,000 to $35,000 in personal property coverage for approximately $13 per month. The critical part most renters miss is that this coverage travels with you-it protects your belongings even when you move, store items off-site, or travel outside your home.

Build Your Home Inventory

A detailed home inventory lists each item, its purchase date, and current replacement cost. You should photograph your belongings and store this inventory somewhere safe, either digitally or in cloud storage. This inventory becomes invaluable when you file a claim because insurers need proof of what you owned and its value. The value of possessions accumulates quickly, so an accurate inventory reflects current replacement costs rather than what you originally paid.

Your Financial Shield Against Liability Claims

Liability coverage protects you from financial devastation when someone gets injured in your rental or you accidentally damage someone else’s property. If a guest slips on your floor and breaks their arm, your liability coverage pays their medical bills up to your policy limit. If you accidentally cause a fire that damages the unit next door, this coverage helps pay for repairs. Medical payments to others coverage specifically handles guest injuries, typically covering up to $1,000 to $5,000 in medical expenses without requiring you to be found legally responsible. Liability coverage also pays your legal expenses if you’re sued, which can cost thousands even if you ultimately win. Most Arizona renters underestimate this risk, but apartment living means more foot traffic and higher exposure to liability claims than detached homes.

Coverage When You Can’t Stay Home

Loss of use coverage activates when a covered event like fire makes your rental uninhabitable and you need temporary housing. This coverage pays the difference between your normal rent and your temporary living costs, including hotel stays or short-term rental apartments. State Farm data shows this coverage can help for up to 24 months, though your policy limit determines the maximum monthly benefit. If your rent is $1,200 monthly and you’re forced into a hotel costing $1,800 per night, loss of use covers that $600 gap plus additional expenses. Arizona’s monsoon season and extreme heat create real risks of temporary displacement, making this coverage worth the modest premium increase. You should calculate this coverage by considering your monthly rent and what comparable temporary housing would cost in your area.

Understanding these three core coverages positions you to make informed decisions about your protection level. The next step involves assessing how much coverage you actually need based on your specific situation and belongings.

Why Arizona Renters Face Real Insurance Needs

Arizona’s environment creates tangible threats to your belongings and finances that renters insurance directly addresses. The state experiences extreme heat regularly exceeding 120 degrees, monsoon storms with wind speeds reaching 60 mph, and hail that destroys windows and property. These aren’t rare occurrences-monsoon season runs from June through September, and the National Weather Service tracks significant weather events across Arizona annually. When a monsoon damages your rental, your landlord’s insurance covers structural repairs, but your personal property coverage pays to replace your furniture, electronics, and clothing. Without renters insurance, you absorb these replacement costs yourself, which can total thousands of dollars.

Arizona’s Weather Threats Hit Your Wallet Hard

Monsoons and extreme heat create direct financial exposure for renters who lack coverage. A single monsoon event can damage air conditioning units, shatter windows, and destroy electronics worth $5,000 or more. Hail storms in Arizona strike without warning and cause rapid damage to outdoor belongings and rental interiors. Your landlord’s policy protects the building structure only-it never covers your personal items. This gap means you face the full replacement cost alone unless you carry renters insurance. Progressive’s 2024 data shows Arizona renters pay approximately $16.97 per month for coverage, a cost that seems minimal compared to replacing a laptop, repairing monsoon damage, or rebuilding your wardrobe after a weather event.

Crime in Arizona Neighborhoods Demands Protection

Arizona’s urban areas face property crime challenges that directly impact renters. Phoenix, Tucson, and other cities report theft incidents that target the exact items renters own-electronics, jewelry, and valuables. Thieves know apartment dwellers accumulate expensive possessions, making renters attractive targets. Renters insurance protects against stolen electronics, jewelry, and other valuables that criminals actively seek. Without this coverage, you replace stolen items from your own pocket, which can exceed $3,000 to $5,000 in a single theft.

Landlord Requirements and Your Financial Protection

Many Arizona landlords now require renters insurance as a lease condition, which means you cannot rent without it regardless of whether you think you need it. This requirement protects landlords from liability but also protects you by forcing coverage you might otherwise skip. Financial protection matters equally-if you cause damage to your rental or someone gets injured there, your personal liability coverage prevents a lawsuit from destroying your finances. A single liability claim can cost $10,000 to $50,000 in legal fees and damages, amounts that would devastate most renters without insurance backing them.

Bundling Saves Money on Your Arizona Coverage

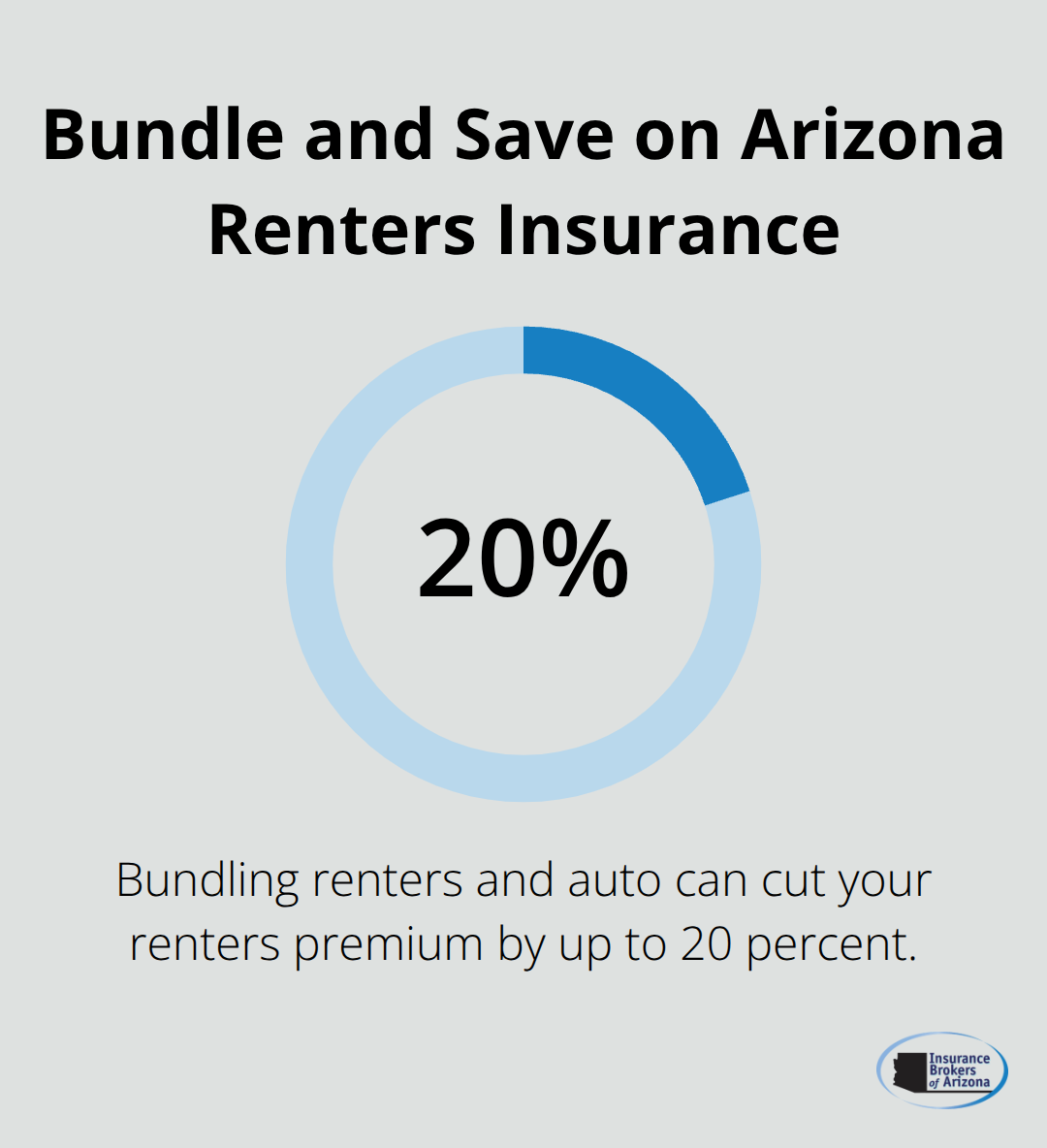

Renters who combine their policy with auto insurance save significantly on both lines. Some carriers offer up to 20 percent discounts on renters coverage when combined with other policies, and bundling can save up to $900 per year on average.

This financial incentive makes renters insurance even more affordable than the base $16.97 monthly cost suggests. Your landlord may mandate coverage, but even without that requirement, Arizona’s environmental and crime realities make renters insurance a practical necessity rather than an optional expense. The next step involves assessing your specific belongings and determining how much coverage actually protects your situation.

How to Choose the Right Renters Insurance Policy

Calculate Your Actual Coverage Needs

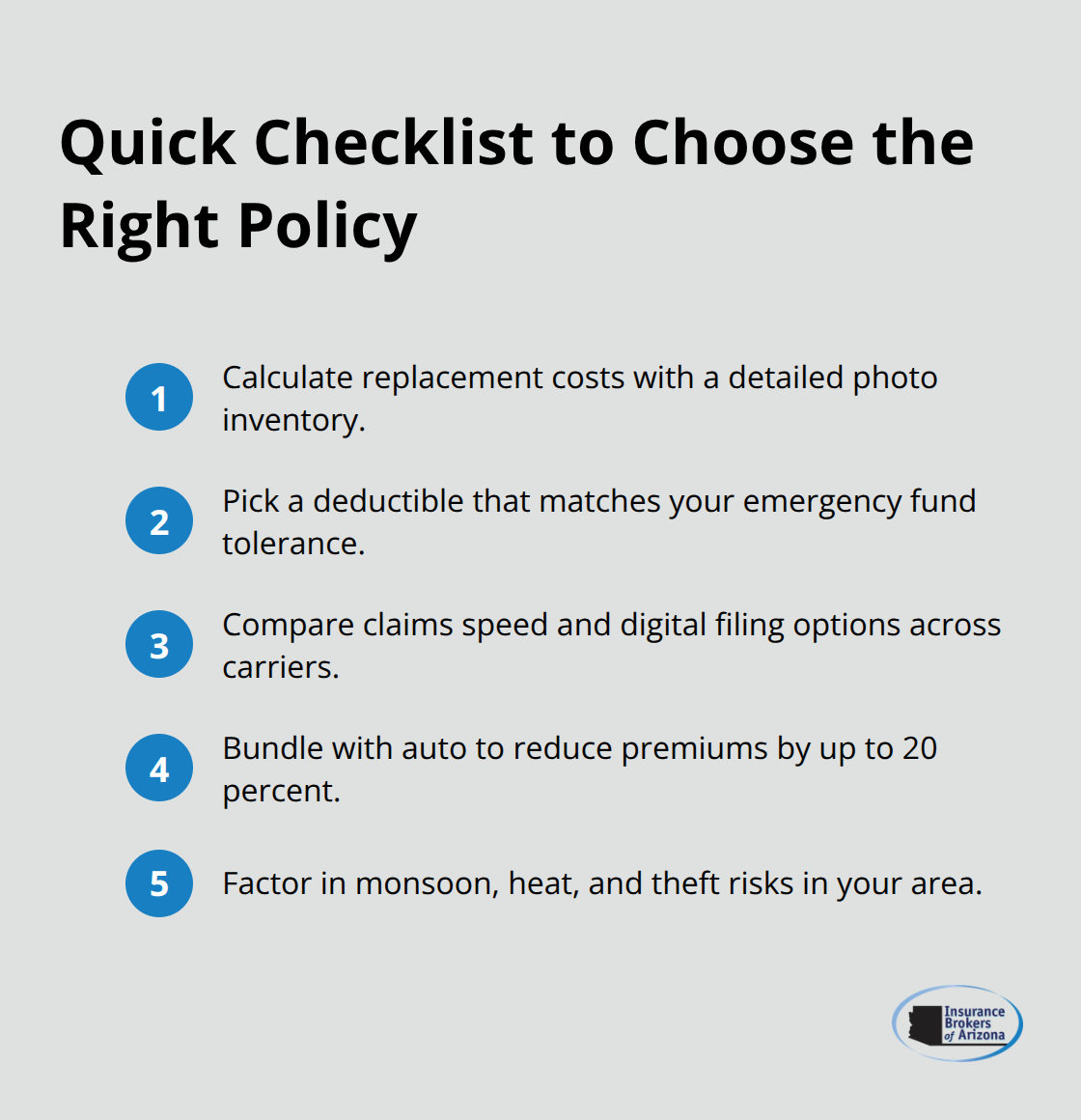

Start by calculating what your belongings actually cost to replace at today’s prices, not what you paid years ago. Most renters drastically underestimate their possessions until they physically list everything. Walk through your apartment and document your electronics, furniture, clothing, kitchen items, and anything else you own. A laptop costs $800 to $1,500 new. A bedroom set runs $2,000 to $4,000. Quality clothing adds up fast.

According to the National Association of Insurance Commissioners, renters in Arizona typically need between $30,000 and $35,000 in personal property coverage, though your actual needs depend entirely on what you own. Use a spreadsheet or phone app to photograph each item and record its current replacement cost, not its original price. This inventory becomes your tool when comparing quotes because you’ll know exactly how much coverage you actually need instead of guessing. Many renters choose $20,000 in coverage when they really need $40,000, leaving themselves dangerously underinsured. Others choose $50,000 when $25,000 would suffice, overpaying unnecessarily.

Select the Right Deductible for Your Situation

Once you know your coverage amount, compare deductibles across carriers because this choice dramatically impacts your monthly cost and your out-of-pocket expenses when you file a claim. A $250 deductible costs more monthly than a $1,000 deductible, but when you file a claim, you pay that amount before insurance kicks in. If a theft costs you $3,000 and your deductible is $1,000, you pay $1,000 and insurance covers $2,000. Progressive’s 2024 data shows Arizona renters pay approximately $16.97 monthly for standard coverage, but this varies based on your deductible choice, location, and specific coverage limits. Bundling renters insurance with auto insurance saves up to 20 percent on renters coverage according to Farmers Insurance data, making that option worth exploring if you carry a vehicle.

Evaluate Claims Processing and Customer Service Quality

When comparing carriers, examine their claims processing speed and customer service quality because these factors matter enormously when you actually need to file a claim. State Farm and Farmers both offer digital filing options that let you submit claims through mobile apps, which matters if you’re dealing with theft or weather damage and need quick resolution. Some carriers process simple claims within days while others take weeks. Arizona renters should specifically ask about how carriers handle monsoon damage claims since these events happen seasonally and carriers sometimes experience volume spikes during June through September. Insurance Brokers of Arizona® works with over 40 reputable carriers, giving you access to multiple options rather than being locked into a single company’s claims process or customer service quality. This variety matters because one carrier might excel at handling theft claims while another specializes in weather-related damage, and your specific risks should influence which company you choose.

Final Thoughts

Renters insurance Arizona protects your belongings, shields you from liability claims, and covers temporary housing costs when disaster strikes. The coverage costs around $16.97 monthly through most carriers, yet most renters skip it entirely and expose themselves to thousands in potential losses. Arizona’s monsoon season, extreme heat, and property crime create real financial risks that renters insurance directly addresses.

Calculate your actual belongings’ replacement cost by creating a detailed inventory with photos and current prices, then compare deductibles across carriers because this choice impacts both your monthly premium and out-of-pocket expenses when you file a claim. Evaluate how quickly each carrier processes claims and whether they offer digital filing options, since these factors matter when you deal with theft or monsoon damage. Consider bundling renters insurance with auto coverage to save up to 20 percent on your renters premium.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers, giving you access to multiple options rather than settling for a single company’s coverage or claims process. Contact Insurance Brokers of Arizona® to compare quotes from multiple carriers and find the right renters insurance policy for your Arizona rental.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.