Home Builder Insurance Arizona: Protecting Construction Projects

Arizona’s construction industry faces unique challenges that standard insurance policies simply don’t address. Desert heat, monsoon storms, and strict state regulations create risks that demand specialized coverage.

We at Insurance Brokers of Arizona® help builders navigate home builder insurance in Arizona with policies tailored to your specific project needs. This guide walks you through the coverage types, local requirements, and selection process that protect your construction investment.

Essential Coverage for Arizona Builders

General Liability Protects Your Bottom Line

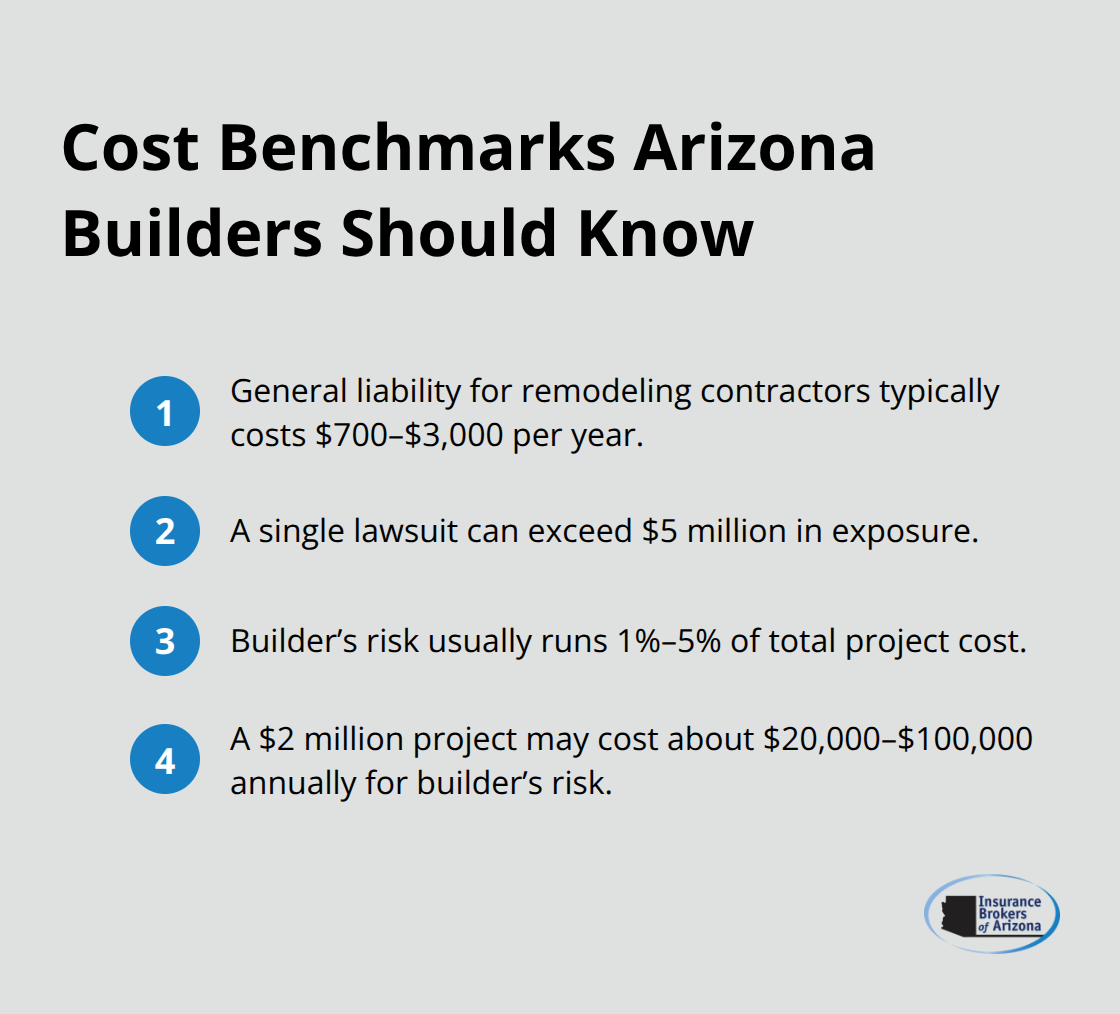

General liability insurance protects you when someone is injured on your job site or your work damages neighboring property. In Arizona, remodeling contractors typically pay between $700 and $3,000 per year for general liability coverage, depending on your trade type and project size, according to Professional Insurance Strategies. A single lawsuit from a worker or property owner can exceed $5 million. High-dollar verdicts in Maricopa County regularly surpass this threshold, which is why carriers have tightened underwriting and raised premiums across the state.

Your general liability policy should cover bodily injury, property damage, and personal injury claims that arise from your construction activities.

Workers’ Compensation Protects Your Team

Workers’ compensation coverage is mandatory in Arizona for any builder with employees. This coverage pays medical bills and lost wages when a worker is injured on the job, and it protects you from lawsuits filed by injured employees. Arizona’s construction industry employs around 22,181 people in the home builders sector alone, according to IBISWorld, and workplace injuries happen frequently on active sites. Premiums vary based on your payroll, the types of work your crew performs, and your safety record. Implement on-site safety training and conduct regular safety audits to lower your costs. These practical steps reduce incidents and signal to insurers that you take risk management seriously, which often translates to lower renewal rates.

Builder’s Risk Covers Your Project Assets

Builder’s risk insurance is temporary coverage that protects the building, materials, equipment, and temporary structures during construction or renovation. It covers theft, vandalism, fire, lightning, storms, and debris removal. In Arizona, builder’s risk premiums typically range from 1% to 5% of your total project cost, meaning a $2 million project might cost $20,000 to $100,000 annually for this coverage. The actual cost depends on your location, construction materials, project duration, and optional add-ons like soft costs or business income protection.

Arizona’s rapid growth, with cities like Queen Creek and Maricopa ranking among the fastest-growing in the nation, is driving higher demand for this coverage. For projects under $5 million, many carriers now offer streamlined underwriting with quick online quotes and minimal human review, making it easier to get coverage in place before breaking ground. This speed matters when you’re working against tight construction schedules and need protection active on day one.

Arizona Construction Risks That Change Your Insurance Needs

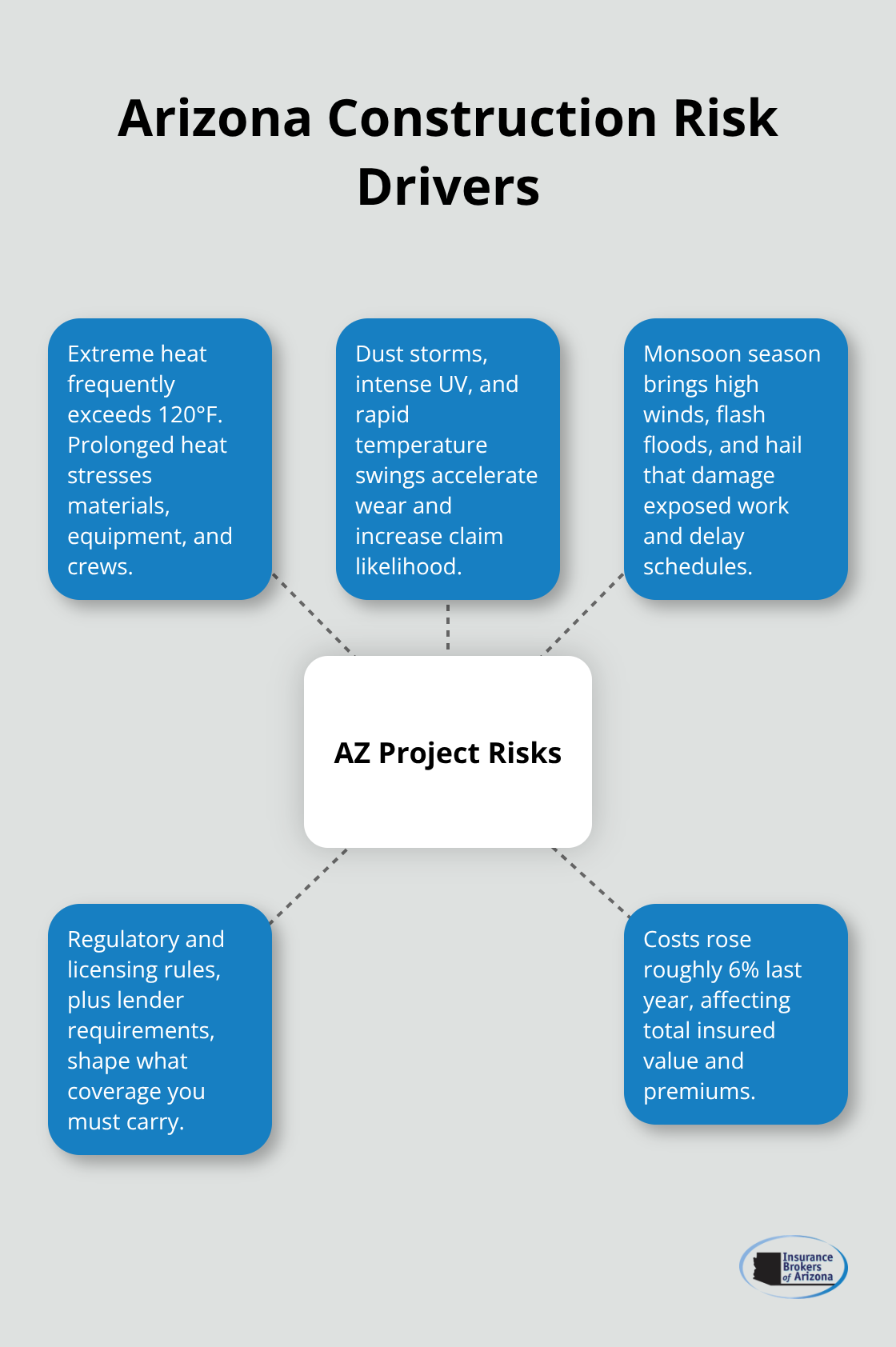

Arizona’s construction environment differs dramatically from most states, and your insurance strategy must account for these regional realities. Desert temperatures regularly exceed 120 degrees, creating stress on materials, equipment, and workers that standard policies don’t adequately address. Dust storms, intense UV exposure, and rapid temperature swings damage exposed materials and equipment faster than contractors expect. Arizona construction costs rose roughly 6% in the last year alone, according to the Arizona Department of Insurance and Financial Institutions, which directly impacts your total insured value and premium calculations. When you quote builder’s risk coverage, your materials and equipment face accelerated wear that influences claim frequency and underwriting decisions.

Carriers price Arizona projects higher because they account for these environmental factors. This means your builder’s risk premium of 1% to 5% of project cost reflects not just the building itself but the genuine risk posed by Arizona’s harsh climate.

Monsoon Season Demands Specific Coverage

Arizona’s monsoon season runs June through September and brings wind gusts exceeding 60 miles per hour, flash flooding, and hail that destroys unprotected materials and temporary structures. Standard builder’s risk policies cover wind and hail damage, but you need to verify that your coverage includes debris removal and ordinance-or-law upgrades, since monsoon damage often triggers code compliance work. Confirm with your broker that soft costs coverage is included if project delays occur due to monsoon shutdowns. Arizona licensing regulations require builders to carry general liability and workers’ compensation before obtaining a license, but they don’t mandate builder’s risk-yet many lenders now require it before releasing construction funds. This creates a practical reality: your lender controls your coverage requirements regardless of state law. Document your policy’s effective date carefully during monsoon season, since many carriers impose weather exclusions during peak months or require higher deductibles if coverage starts mid-June through August.

Local Regulations and Licensing Requirements Shape Your Coverage

Arizona’s Department of Insurance and Financial Institutions enforces strict contractor licensing rules that indirectly affect insurance requirements. Licensed contractors must maintain active general liability and workers’ compensation coverage to keep their license valid. Municipal permitting offices in Phoenix, Scottsdale, Mesa, and other major Arizona cities increasingly request proof of builder’s risk insurance before issuing construction permits, even when not legally mandated. Maricopa County projects face additional scrutiny due to high-dollar verdicts exceeding $5 million in recent years, which means carriers underwrite these projects more conservatively and charge accordingly. If you work on projects in multiple counties, understand that each jurisdiction may have different insurance expectations. A commercial office project in downtown Phoenix carries different risk profiles than a residential remodel in Prescott, and your carrier will price accordingly.

How Location and Project Type Affect Your Premiums

Your project’s specific location within Arizona determines much of your insurance cost. Carriers assess proximity to flood zones, wildfire risk areas, and regions with higher crime rates-all factors that raise premiums beyond the base 1% to 5% of project cost. Construction materials also influence pricing significantly. Wood-frame structures cost more to insure than fire-resistive or masonry buildings because they present higher loss potential. A $2 million commercial office project in downtown Phoenix with dust storm exposure and temporary storage could incur approximately $20,000 per year in builder’s risk premiums, while a similar project in a lower-risk area might cost substantially less. Project duration matters too-longer timelines expose your work to more weather events and theft risk, which carriers reflect in their quotes. When you select your coverage limits, set them equal to your final anticipated construction cost, including materials, labor, overhead, permits, and architectural plans. This alignment prevents underinsurance and ensures your lender’s interests receive proper protection.

Coordinating Coverage Across Multiple Parties

Construction projects typically involve owners, general contractors, developers, and subcontractors-each with different insurance needs and responsibilities. Your builder’s risk policy can name multiple parties as insureds, and your lender often requires inclusion as mortgagee. Clarify who pays for builder’s risk insurance before contracts are signed, since terms vary widely. Some owners absorb the cost; others require general contractors to carry it. Subcontractors need their own coverage or endorsements on the main policy to avoid gaps. When project scope changes occur (and they always do in Arizona construction), coordinate immediately with your insurer to update limits and the list of insureds. Failing to add a new subcontractor or adjust coverage for design changes leaves you exposed to uninsured losses. Your policy duration must align with your project timeline, and you should adjust it as work progresses to avoid lapses between phases.

Understanding these Arizona-specific factors positions you to select coverage that actually protects your project rather than leaving gaps when claims arise. The next section walks you through the practical process of choosing the right policy and working with professionals who understand Arizona’s construction landscape.

Choosing the Right Coverage for Your Arizona Project

Start with your total project cost and work backward to determine coverage limits. Many Arizona builders underestimate their total insured value, which creates dangerous gaps when claims arise. Your total insured value should include materials, labor, overhead, permits, architectural plans, and any soft costs like project management or temporary facilities. If your project costs $2 million, your builder’s risk coverage should reflect that full amount, not just the building structure.

Carriers in Arizona typically quote builder’s risk at 1% to 5% of total project cost, but this percentage only applies if your coverage limits match your actual exposure. Set limits too low and you face partial recovery on a claim. Set them too high and you overpay unnecessarily. For projects under $5 million, many carriers now offer streamlined online underwriting that delivers quotes within 24 to 48 hours, so you can obtain accurate quotes faster than ever before.

Deductibles and Seasonal Adjustments

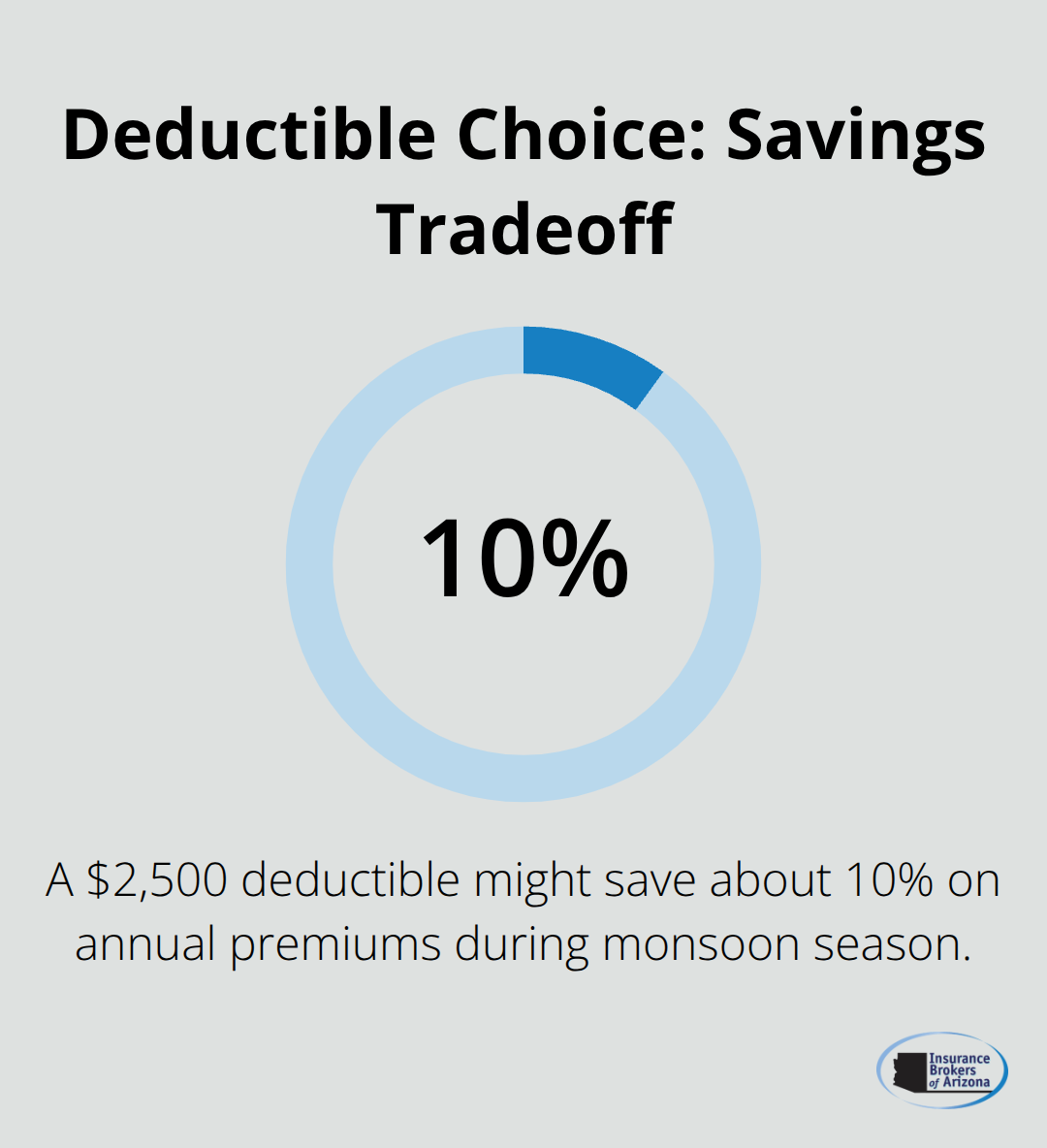

When you compare deductibles, understand that higher deductibles lower your premium but increase your out-of-pocket cost when damage occurs. A $2,500 deductible on a monsoon-damaged project might save you 10% on annual premiums but costs you $2,500 when hail destroys temporary structures. In Arizona’s monsoon season, consider a lower deductible from June through September, then revert to higher deductibles during calmer months.

Your choice depends entirely on your cash flow and risk tolerance.

Aligning General Liability with Your Trades

General liability coverage for Arizona remodeling contractors ranges from $700 to $3,000 annually according to Professional Insurance Strategies, but this baseline assumes standard residential work. Commercial projects, high-rise work, or projects in high-crime areas cost substantially more. Verify that your general liability policy covers all the trades working on your site, since some carriers exclude specific work types. If you hire a roofer, electrician, and plumber, each subcontractor should either carry their own coverage or be added as additional insureds on your policy.

Builder’s Risk Materials and Storage Coverage

Builder’s risk coverage must explicitly cover materials in transit and at temporary storage locations, since Arizona projects frequently stage materials off-site due to space constraints. Soft costs coverage is worth the additional premium because monsoon delays or permit hold-ups can cost thousands daily. Arizona construction costs rose 6% last year according to the Arizona Department of Insurance and Financial Institutions, which means your material costs likely increased since your initial project budget. You should coordinate with your carrier before costs escalate further to adjust your coverage limits upward.

Scope Changes and Coverage Adjustments

When your project scope changes, notify your insurer immediately rather than hoping they won’t notice. Scope changes alter your risk profile, and carriers can deny claims if coverage doesn’t match the actual work being performed. We at Insurance Brokers of Arizona® work directly with Arizona builders to align coverage with real project conditions, adjusting limits and endorsements as your work evolves.

Final Thoughts

Home builder insurance Arizona protects your projects from the specific risks that plague construction in this state. General liability, workers’ compensation, and builder’s risk coverage form the foundation of your protection strategy, but Arizona’s desert climate, monsoon season, and regulatory environment demand more than generic policies. You need coverage that accounts for dust storms, extreme heat, flash flooding, and the high-dollar verdicts that characterize Maricopa County litigation.

Setting your coverage limits equal to your total project cost (including materials, labor, overhead, and permits) prevents dangerous gaps when claims arise. Adjusting deductibles seasonally during monsoon months and coordinating coverage across all parties involved in your project eliminates confusion and exposure. The difference between adequate protection and costly gaps often comes down to working with professionals who understand Arizona’s construction landscape.

Contact Insurance Brokers of Arizona® to discuss your specific project and receive quotes from multiple carriers within 24 to 48 hours. Our team will explain your coverage limits, deductibles, exclusions, and optional add-ons in plain language so you understand exactly what you’re buying. Arizona’s construction industry is booming, but that growth means higher stakes when claims arise.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.