Is Hazard and Home Insurance the Same?

Many homeowners ask us whether hazard and home insurance are the same thing. The short answer is no-they’re different types of coverage that protect different aspects of your property.

At Insurance Brokers of Arizona®, we’ve found that confusion between these two policies often leaves homeowners underinsured. Understanding what each covers will help you make better decisions about protecting your home and finances.

What Hazard Insurance Covers and Why Lenders Demand It

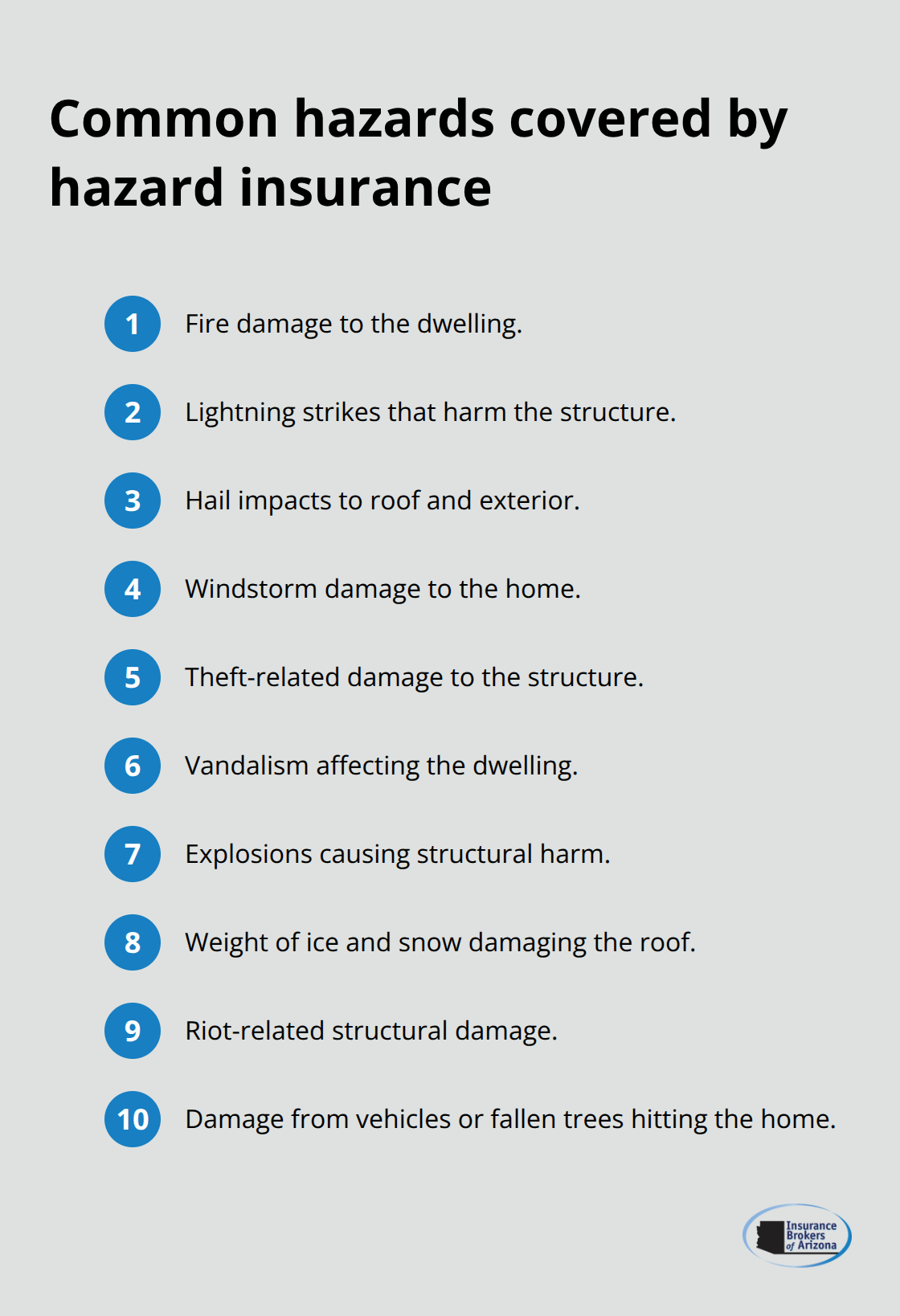

Hazard insurance protects your home’s physical structure from specific perils. Your mortgage lender requires this coverage as a condition of your loan, which is why understanding what it actually protects matters so much. Hazard insurance covers fire, lightning, hail, windstorms, theft damage to the structure, vandalism, explosions, weight of ice and snow, riots, and damage from vehicles or fallen trees hitting your home.

What Hazard Insurance Excludes

Standard hazard policies exclude floods, earthquakes, mold, wear and tear, and neglect. These gaps matter because they leave your home vulnerable to common risks in certain regions. If you live in a flood-prone area or earthquake zone, you’ll need separate policies to fill these holes. According to Bankrate data from July 2025, the average homeowners insurance cost with $300,000 in dwelling coverage runs about $2,466 per year, though your actual premium depends heavily on your location, home age, construction type, and deductible choice.

What Happens When You Skip Hazard Insurance

Your mortgage lender requires hazard insurance, period. If you fail to maintain it, lenders purchase forced-place insurance on your behalf, which costs significantly more and provides minimal coverage. This forced-place option is far more expensive than selecting your own policy, making it financially foolish to let coverage lapse.

Hazard Insurance for Homeowners Without Mortgages

If you own your home outright, no lender mandate exists, yet hazard coverage remains a smart protection for your investment. Premiums vary considerably by location, with coastal hurricane zones and wildfire-prone areas seeing substantially higher rates because insurers price coverage based on actual risk data.

How Your Deductible Affects Your Premium

Your deductible choice directly affects your premium, so raising it from $500 to $1,000 or $1,500 can lower your annual costs (provided you have emergency savings to cover the higher out-of-pocket expense when filing a claim). Location, home construction, and your claims history all influence what you pay. Understanding these factors helps you compare quotes effectively and find coverage that fits your budget and risk tolerance.

What Home Insurance Actually Covers

Home insurance is fundamentally broader than hazard insurance because it combines dwelling protection with personal property coverage and liability protection into one comprehensive policy. Where hazard insurance focuses exclusively on your home’s structure, home insurance protects your belongings inside that structure and shields you financially if someone gets injured on your property and sues.

How HO-3 Policies Work

Most homeowners purchase an HO-3 policy, the standard market option that uses open-peril coverage for the dwelling (meaning it covers all perils except those specifically excluded) while using named-peril coverage for your personal property (meaning it covers only the specific perils listed in the policy). This distinction matters practically because your furniture, electronics, and clothing operate under different rules than your roof and walls.

Personal Property Coverage Limits

Personal property coverage typically runs at 50 to 70 percent of your dwelling limit, so if your home’s structure is insured for $300,000, your belongings might be covered for $150,000 to $210,000. You should adjust this percentage based on what you actually own, not what an insurance company suggests. High-value items like jewelry, art, or expensive electronics often need separate endorsements called floaters because standard policies cap coverage on certain categories.

Liability Protection and Umbrella Policies

Personal liability coverage protects you when someone is injured at your home and holds you responsible. According to Bankrate’s 2025 data, liability limits typically range from $100,000 to $300,000 depending on your assets and risk profile. Most people with significant savings or investments should carry at least $300,000 in liability protection, and many financial advisors recommend adding an umbrella liability policy that provides an additional $1 million or more in coverage for roughly $150 to $300 annually.

Additional Living Expenses Coverage

Additional living expenses coverage activates if a covered peril forces you to leave your home during repairs, paying for hotel stays, restaurant meals, and other necessary costs while your home is being restored. This protection matters because reconstruction timelines can stretch months, and without this coverage, you absorb those living costs yourself while also paying your mortgage or rent. These gaps between what hazard insurance covers and what home insurance provides create significant financial exposure that many homeowners overlook until they face a loss.

Hazard vs Home Insurance: What Actually Differs

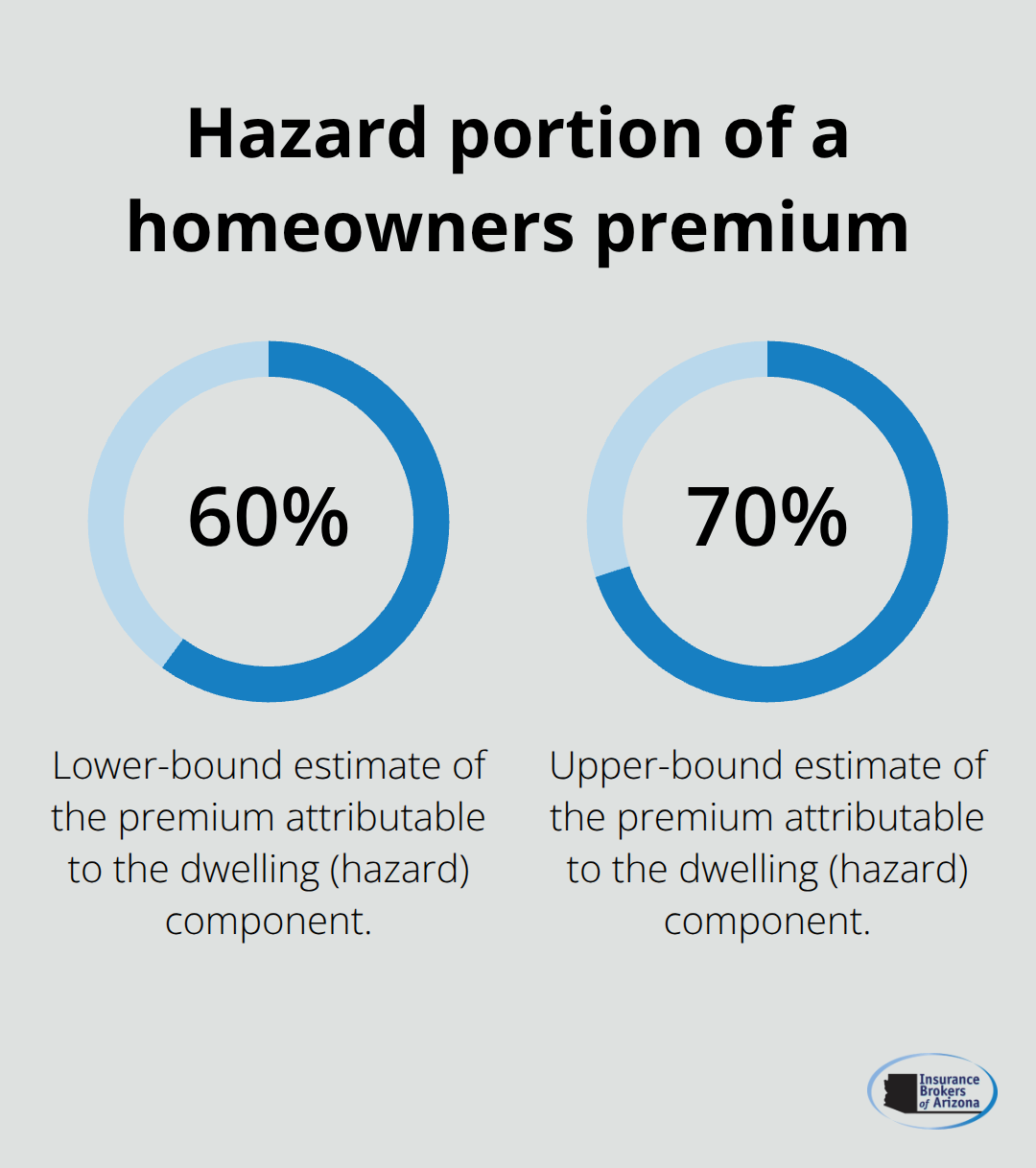

Hazard insurance and home insurance operate under completely different financial structures, which is why comparing their costs side-by-side misleads most homeowners. Hazard insurance isn’t a separate line item you purchase independently; it’s the dwelling protection component bundled inside your homeowners policy. When you see that average homeowners insurance costs $2,466 annually according to Bankrate’s July 2025 data for $300,000 in dwelling coverage, that figure includes hazard protection plus personal property coverage, liability protection, and additional living expenses. The hazard portion alone represents roughly 60 to 70 percent of your total premium, meaning the structural protection costs somewhere between $1,480 and $1,726 annually in that example.

Location drives massive premium variations, with coastal hurricane zones paying 40 to 60 percent more than inland areas because actual loss data shows higher risk. If you live in a high-risk wildfire zone in Arizona, your premium will exceed national averages substantially. Your deductible choice creates the most direct cost control: raising it from $500 to $1,500 typically reduces premiums by 15 to 25 percent, but only if you maintain emergency savings to cover that higher out-of-pocket expense when filing a claim.

Why Lenders Mandate Hazard Coverage

Your mortgage lender mandates hazard insurance specifically because they hold a financial interest in your home. They don’t care whether you have personal property coverage or liability protection; they only require that the structure itself is insured at replacement cost so the mortgage can be paid off if your home burns down. This legal requirement means forced-place insurance becomes your reality if you let hazard coverage lapse, and that lender-purchased coverage costs 50 to 100 percent more than standard policies while providing minimal protection.

Home insurance, by contrast, protects you and your financial assets rather than satisfying a lender’s requirement. This distinction explains why owning your home outright changes the insurance conversation entirely: without a lender mandate, hazard coverage becomes optional rather than mandatory, though it remains financially prudent for anyone carrying a significant asset.

The Personal Property Protection Gap

Hazard insurance covers your home’s structure but ignores your belongings completely, creating a dangerous gap that most homeowners don’t recognize until after a loss occurs. If a fire destroys your home, hazard insurance rebuilds the structure while your personal property coverage compensates for furniture, electronics, and clothing inside that structure. Without home insurance’s personal property component, you lose everything you own inside the burned home with zero compensation.

Liability Protection You Cannot Ignore

Liability protection matters equally: if someone slips on your icy driveway and sues for $500,000 in medical bills, hazard insurance provides nothing because it covers only the structure. Home insurance’s liability component protects you in that scenario, and most people carrying significant assets should add umbrella liability coverage providing $1 million or more in additional protection for $150 to $300 annually. This structural protection versus comprehensive protection distinction is absolute: hazard insurance alone leaves you financially exposed in ways that home insurance prevents.

Final Thoughts

Is hazard and home insurance the same? No-hazard insurance covers only your home’s structure against specific perils like fire, wind, and hail, while home insurance bundles that structural protection with personal property coverage and liability protection. Your mortgage lender requires hazard coverage because they have a financial stake in your home, but home insurance protects you and your assets from losses that hazard coverage alone cannot address.

The gaps between these two policies create real financial exposure that affects your wallet directly. Hazard insurance leaves your personal belongings completely unprotected, meaning a fire that destroys your home also destroys everything inside it with zero compensation from hazard coverage. Liability protection matters equally: if someone sues you for injuries sustained at your home, hazard insurance provides nothing because it covers only the structure, so most homeowners carrying significant assets should add umbrella liability coverage providing $1 million or more in additional protection for roughly $150 to $300 annually.

Your specific situation determines what coverage you actually need, and shopping around produces meaningful savings. If you carry a mortgage, your lender mandates hazard insurance, and skipping it triggers forced-place insurance that costs 50 to 100 percent more while providing minimal protection. We at Insurance Brokers of Arizona® work with over 40 reputable carriers to find coverage that matches your specific needs and budget, so contact us today for a personalized assessment that identifies gaps and secures competitive rates tailored to your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.