Vacant Home Insurance: Complete Coverage Guide

An empty house is a liability waiting to happen. Pipes freeze, thieves strike, and weather damage spreads unchecked when no one’s home to catch problems early.

Vacant home insurance protects your property during extended absences in ways standard homeowners policies won’t. We at Insurance Brokers of Arizona® help Arizona property owners understand their coverage options and find affordable protection for unoccupied homes.

What Vacant Home Insurance Actually Covers

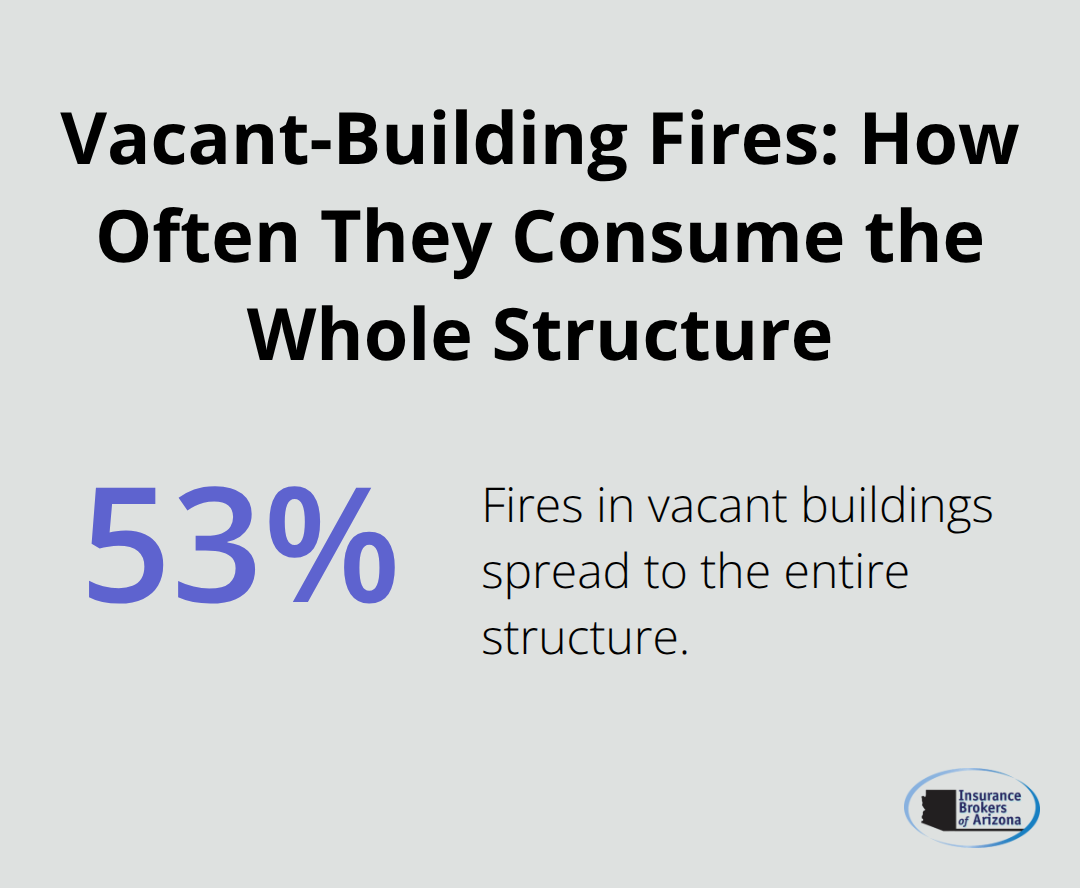

Vacant home insurance protects the structure of your empty property against specific perils when standard homeowners policies won’t. Most regular homeowners policies stop covering critical damage after your home sits vacant for 30 to 60 days, according to the National Association of Insurance Commissioners. Once that threshold hits, you lose protection for vandalism, theft, and water damage unless you switch to vacant coverage. A vacant home policy typically uses a DP-1 form, which covers fire, lightning, windstorms, hail, explosions, and smoke damage to the structure itself. Theft and vandalism coverage require endorsements, and liability protection rarely appears in the base policy. This matters because standard coverage gaps leave you exposed to expensive losses. The Insurance Information Institute reports that fires in vacant buildings spread to the entire structure about 53 percent of the time, versus much lower rates in occupied homes. That’s real damage that happens faster and spreads further when no one’s there to catch it early.

When Your Home Actually Becomes Vacant

Your home crosses into vacant territory after 30 to 60 days of no occupancy, depending on your insurer. The distinction between vacant and unoccupied matters legally: vacant means no one lives there and personal property is minimal or gone; unoccupied means residents are temporarily away but furniture and utilities remain. If you’re buying a home and won’t move in for two months, renovating extensively, inherited property you haven’t occupied yet, or selling between owners, you need vacant coverage. Mortgage lenders require it in these situations because they want proof that the structure is protected. Even if you own the property outright, one burst pipe or break-in can cost $10,000 to $50,000 in repairs-far more than a few months of vacant insurance premiums. Vacant coverage typically costs 50 to 60 percent more than standard homeowners insurance according to the Insurance Information Institute, but that premium difference is minimal compared to the financial damage from an uninsured loss.

How Problems Compound in Empty Homes

The real risk compounds when problems go undetected. A slow water leak in winter can cause mold and structural rot for weeks before anyone notices. Squatters can move into an unsecured property. Vandals target empty homes knowing no one will interrupt them. Thieves target empty homes because no one calls police, no lights turn on at night, no cars sit in the driveway, and no signs of activity appear. Pipes freeze in winter without furnaces running or water circulating. Storms damage roofs, windows, and siding with no one there to document the loss or make emergency repairs.

Environmental and Legal Risks in Vacant Properties

Humidity levels in vacant homes spike to 60 to 90 percent relative humidity in many climates, creating ideal conditions for mold growth that spreads rapidly through walls and insulation. In Florida specifically, this humidity problem combined with high rainfall and temperature swings creates mold risk that can destroy a home’s value within months. Adverse possession becomes a legal liability when squatters occupy your property long-term; in some states they can gain legal rights to the property if you don’t actively prevent occupation. Vacant homes also face attractive nuisance liability if someone is injured on your property-a broken window invites trespassing, and if a trespasser is hurt, you could face a lawsuit. These aren’t remote possibilities. They’re the primary reasons insurers charge so much more for vacant coverage and why standard policies exclude vacant properties entirely. Understanding what your vacant policy covers is only half the battle-knowing what protection options exist helps you choose the right endorsements for your specific situation.

What Your Vacant Home Policy Actually Covers

Understanding DP-1 Forms and Their Limits

DP-1 policies form the backbone of vacant home coverage, and understanding exactly what they protect matters before you buy. These specialized forms cover fire, lightning, windstorms, hail, explosions, and smoke damage to your home’s structure. What they don’t cover is equally important: water damage from burst pipes, theft, vandalism, and liability claims typically require separate endorsements. This gap exists because insurers view vacant homes as higher-risk properties where problems escalate faster. A burst pipe in an occupied home gets fixed within hours; in a vacant home it runs for weeks, causing mold, structural rot, and foundation damage that can exceed $50,000 in repairs.

Water Damage and Weather-Related Endorsements

You need to be explicit about which endorsements matter for your situation. If your vacant home sits in an area with freeze-thaw cycles or winter weather, water damage endorsements are non-negotiable. If your property is in a neighborhood with theft or vandalism issues, those endorsements become essential protection rather than optional upgrades. The Insurance Information Institute data shows that fires in vacant buildings spread to the entire structure roughly 53 percent of the time, making fire coverage the one peril you absolutely cannot skip. Water damage endorsements protect against the most common and costly losses in vacant properties (burst pipes, frozen lines, and roof leaks).

Theft, Vandalism, and Liability Protection

Theft and vandalism endorsements exist because base DP-1 policies exclude them entirely, leaving your windows, doors, and fixtures vulnerable to thieves who know empty homes won’t report crimes immediately. These endorsements typically cost 5 to 15 percent more on your vacant premium but protect against real losses that happen regularly in unoccupied properties. Liability coverage rarely appears in base vacant policies, which means if someone is injured on your property or damages someone else’s property from your vacant home, you face personal financial exposure. This matters most if your property sits on a corner lot, has visible damage that attracts trespassers, or has known hazards like a deteriorating deck or broken fence. Adding liability endorsements costs roughly 10 to 20 percent more but shields you from lawsuits that could cost far more than the premium difference.

Comparing Coverage Across Carriers

When comparing quotes from carriers like Farmers, American Modern, or Foremost, verify which perils come standard and which require endorsements. Some insurers bundle theft and vandalism; others charge separately. Some include limited liability; others require you to add it. The cheapest quote often omits critical endorsements, making the final premium appear lower until you discover gaps at claim time. Request quotes with identical coverage levels across carriers to compare apples to apples, and ask specifically which endorsements each policy includes versus requires. Understanding these coverage differences now prevents expensive surprises later when you file a claim.

What Really Drives Vacant Home Insurance Costs

Location and Property Condition Shape Your Premium

Your vacant home insurance premium reflects factors you control and factors you don’t. Location matters enormously-a vacant home in a high-crime neighborhood with a history of break-ins costs significantly more than the same home in a quiet rural area. Home condition and maintenance level directly affect your rate; insurers charge more for properties showing signs of neglect because deterioration accelerates in empty homes. Vacant home insurance typically costs 150 to 300 percent more than standard homeowners coverage, but this figure hides a real reality: some properties pay closer to double or triple the standard rate depending on their risk profile. Florida vacant properties average around $1,842 annually compared to about $1,228 for standard coverage, reflecting the state’s specific risks from humidity, hurricanes, and weather exposure.

Duration and Security Features Lower Your Costs

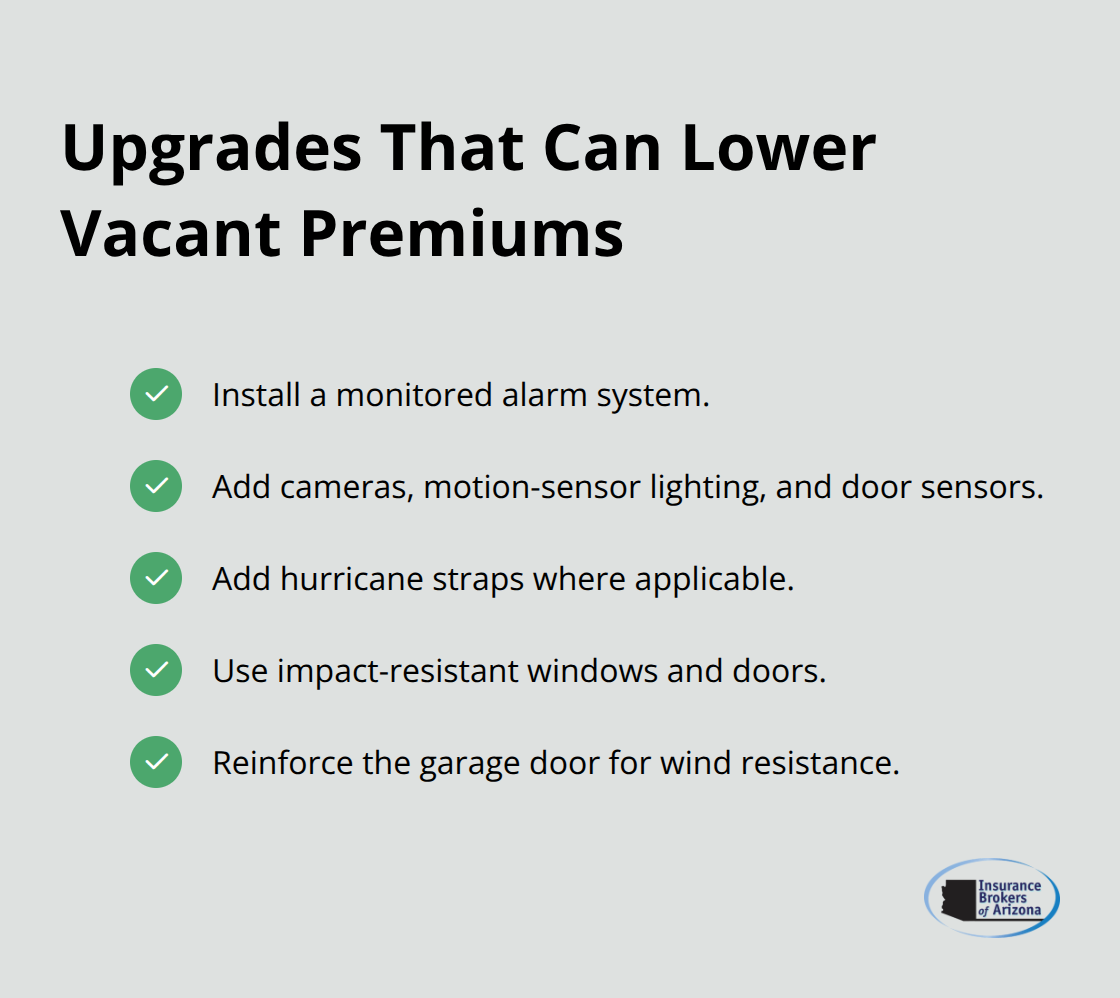

Your expected vacancy duration affects your premium directly-a three-month vacancy costs less to insure than a twelve-month one because shorter timeframes mean lower exposure to cumulative risks. Security features influence your premium in measurable ways. A monitored alarm system typically qualifies you for a 5 to 15 percent discount on your vacant policy, while comprehensive security packages combining cameras, motion-sensor lighting, and door sensors can push savings toward 15 percent or higher. Wind mitigation features in hurricane-prone areas like Arizona’s monsoon regions or Florida’s coastal zones reduce premiums by 20 to 40 percent-items like hurricane straps, impact-resistant windows and doors, and reinforced garage doors signal to insurers that you take prevention seriously.

Compare Identical Coverage Across Multiple Carriers

Shopping for vacant coverage requires comparing identical coverage across multiple carriers rather than chasing the lowest quote. Farmers, American Modern, Foremost, and American Family all offer vacant policies, but their coverage bundles differ significantly. Request quotes with the same dwelling limit, identical endorsements (water damage, theft, vandalism, liability), and matching deductibles so you’re actually comparing prices for equivalent protection. A quote that appears 20 percent cheaper often excludes an endorsement the other quote includes, making the real difference much smaller.

Optimize Your Policy Term and Bundling Options

Short-term policies lasting three, six, or nine months with prorated cancellation options exist specifically for renovations or temporary vacancies-don’t pay for twelve months of coverage when you need three. Ask each carrier about bundling discounts; combining your vacant home policy with auto or other property coverage frequently reduces the overall cost. Some insurers offer discounts for good claims history or prior insurance, so mention these details when requesting quotes.

Document Condition and Arrange Professional Inspections

Document your home’s condition with photos before vacancy starts because insurers sometimes require proof that the property was well-maintained before problems developed-this documentation strengthens future claims and occasionally qualifies you for better rates. Professional home inspections conducted every one to two weeks, with documented reports including humidity and temperature readings, can reduce premiums by demonstrating active oversight and potentially satisfy lender requirements. The cheapest option rarely exists; the best option balances premium cost against coverage completeness and insurer reputation for actually paying claims when vacant properties suffer losses.

Final Thoughts

Vacant home insurance protects your property during extended absences when standard homeowners policies won’t cover the risks. After 30 to 60 days of vacancy, your regular coverage disappears, leaving you exposed to theft, vandalism, water damage, and structural losses that accelerate without anyone present to catch them early. A DP-1 policy with the right endorsements covers fire, weather damage, and structural protection, but you need to add theft, vandalism, and liability coverage explicitly to close the gaps that matter most.

Your premium reflects real risk factors including location, home condition, security features, and vacancy duration. A monitored alarm system cuts your cost by 5 to 15 percent, while wind mitigation features in Arizona’s monsoon-prone areas reduce premiums by 20 to 40 percent. Short-term policies lasting three to six months cost less than twelve-month commitments when your vacancy is temporary, and bundling your vacant home insurance with auto or other coverage frequently lowers your overall expense.

The most expensive mistake is comparing quotes without verifying identical coverage across carriers like Farmers, American Modern, or Foremost. Request quotes with matching dwelling limits, identical endorsements, and the same deductibles so you actually compare equivalent protection. Contact Insurance Brokers of Arizona® to discuss your vacant property needs and secure protection that covers the risks your empty home faces.