Is Vandalism Covered by Commercial Property Insurance?

Vandalism can be a costly and disruptive event for any business owner. At Insurance Brokers of Arizona®, we often hear the question: “Is vandalism covered by commercial property insurance?”

This blog post will explore the ins and outs of vandalism coverage in commercial property policies, helping you understand your protection and what steps to take if your business falls victim to such an incident.

What Does Commercial Property Insurance Cover?

Commercial property insurance protects business owners’ physical assets against various risks. This type of insurance covers damage to buildings, equipment, inventory, and other property used in business operations.

Types of Coverage

Most commercial property policies offer protection against fire, theft, and natural disasters. However, coverage can vary significantly between policies. Some policies might cover damage from floods or earthquakes, while others exclude these perils. Business owners must review their policies carefully to understand their exact coverage.

Common Exclusions

Commercial property insurance provides broad protection, but it’s not all-encompassing. Common exclusions often include:

- Wear and tear

- Certain types of water damage

- Damage from war or nuclear hazards

The Insurance Information Institute reports that many businesses discover gaps in their coverage only after suffering a loss.

Customizing Your Coverage

Every business has unique needs, which is why off-the-shelf policies often fall short. Insurance professionals work closely with clients to tailor coverage to their specific risks. This might involve adding endorsements for specific perils or increasing limits for high-value equipment.

The Importance of Regular Reviews

Business needs change over time, and so should insurance coverage. A study by the National Association of Insurance Commissioners found that 40% of businesses are underinsured by 40% or more. Regular policy reviews can help ensure coverage keeps pace with business growth and changing risk landscapes.

Commercial property insurance forms the backbone of a comprehensive business insurance strategy. Understanding its scope and limitations is essential for protecting business assets effectively. Now, let’s explore how vandalism is specifically addressed within these policies.

Does Commercial Property Insurance Cover Vandalism?

Defining Vandalism in Insurance Terms

For insurance purposes, vandalism refers to the willful or malicious destruction or defacement of property. This includes acts such as graffiti, broken windows, damaged signage, or intentional flooding. It’s important to note that theft is generally not considered vandalism and may require separate coverage.

Typical Coverage for Vandalism

Most standard commercial property insurance policies include coverage for vandalism. If vandals damage your business property, your policy will likely cover the costs of repairs or replacements. However, you should review your specific policy, as coverage can vary between insurers and policy types.

The Insurance Information Institute reports that vandalism claims rank among the most common types of property damage claims for businesses (underscoring the importance of adequate coverage).

Understanding Policy Limits and Deductibles

While vandalism is typically covered, it’s subject to policy limits and deductibles. Your policy limit is the maximum amount your insurer will pay for a covered loss. For instance, if your policy has a $500,000 limit and vandalism causes $600,000 in damages, you’ll be responsible for the $100,000 difference.

Deductibles also play a crucial role. This is the amount you agree to pay out of pocket before your insurance coverage kicks in. For example, if you have a $1,000 deductible and vandalism causes $5,000 in damages, you’ll pay $1,000, and your insurer will cover the remaining $4,000.

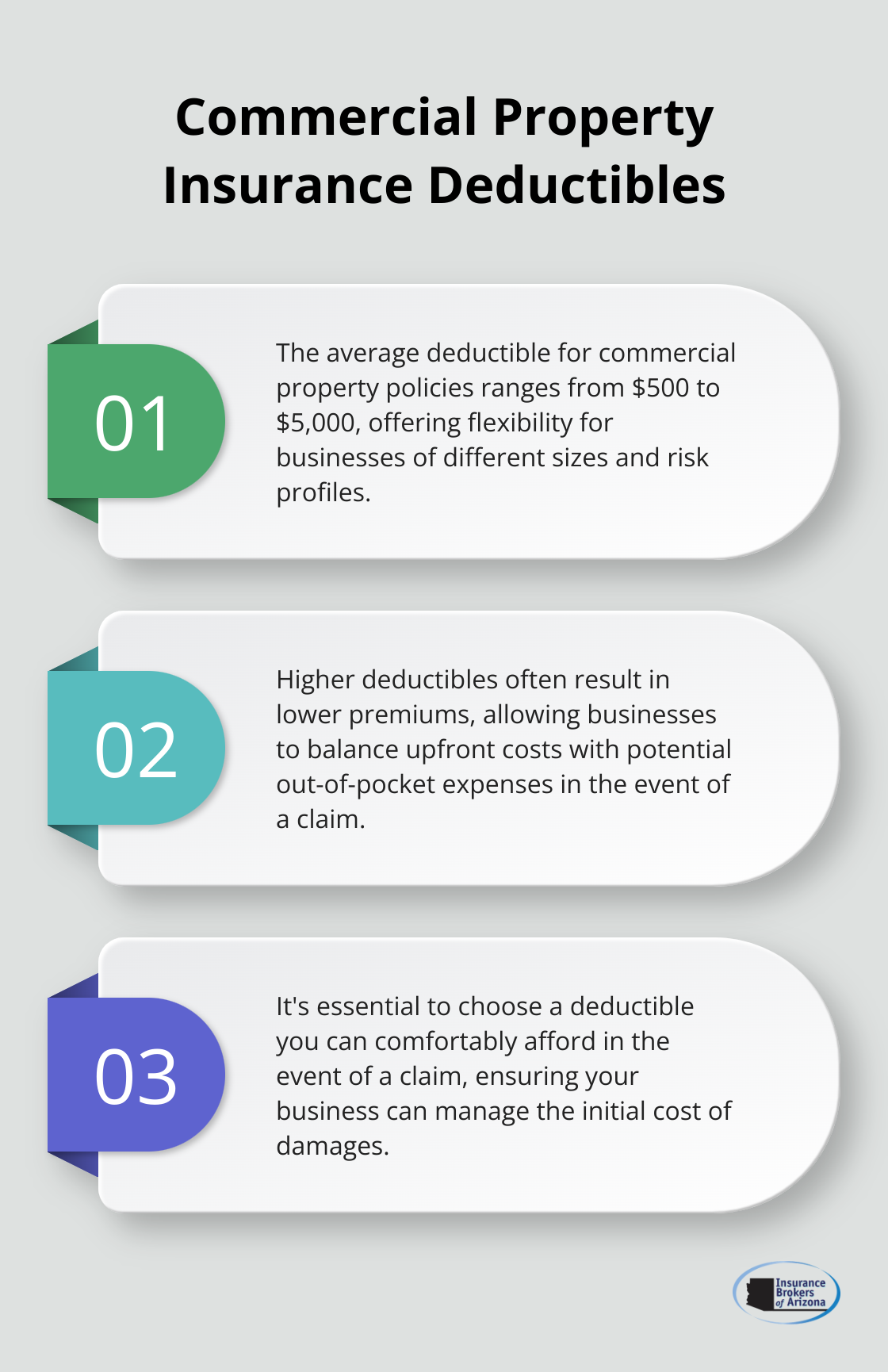

The National Association of Insurance Commissioners reports that the average deductible for commercial property policies ranges from $500 to $5,000. Higher deductibles often result in lower premiums, but it’s essential to choose a deductible you can comfortably afford in the event of a claim.

Special Considerations for Vandalism Coverage

Some policies may have exclusions or limitations for vandalism coverage. For instance, many insurers won’t cover vandalism if a property has been vacant for more than 60 consecutive days. Additionally, intentional damage caused by the policyholder or their employees is typically not covered.

The Importance of Regular Policy Reviews

As your business evolves, so do your insurance needs. Regular policy reviews ensure your coverage keeps pace with your business growth and changing risk landscape. A study by the National Association of Insurance Commissioners found that 40% of businesses are underinsured by 40% or more, highlighting the need for periodic reassessment.

Now that we’ve covered the basics of vandalism coverage in commercial property insurance, let’s explore the steps you should take if your business falls victim to such an incident.

What to Do After Your Business Is Vandalized

Document the Damage

When you discover vandalism at your business, start by documenting everything. Take clear, detailed photos and videos of all affected areas. Capture wide-angle shots to show the extent of the damage, as well as close-ups of specific items. This visual evidence will support your insurance claim and any potential legal proceedings.

Create a comprehensive list of all damaged or destroyed property. Include descriptions, estimated values, and (if possible) purchase dates and original costs. Collect any receipts or invoices for the damaged items. The more detailed your documentation, the smoother your claims process will likely be.

File a Police Report

Contact the police immediately to report the vandalism. A police report is often required by insurance companies when filing a claim. Provide the officers with all the information you’ve gathered about the incident. Ask for a copy of the police report or at least the report number for your records.

The FBI’s Uniform Crime Reporting Program shows that vandalism ranks as one of the most common property crimes, which underscores the importance of prompt reporting.

Contact Your Insurance Provider

Reach out to your insurance provider as soon as possible. Many insurers operate 24/7 claims hotlines, so don’t wait until business hours to make the call. Provide them with all the information you’ve gathered, including the police report number.

Your insurer will guide you through the next steps of the claims process. They may send an adjuster to assess the damage in person. Be prepared to provide access to your property and any additional information they might need.

Secure Your Property

Take immediate steps to secure your property against further damage or potential theft. Board up broken windows, change locks if necessary, and consider hiring temporary security if the vandalism has compromised your building’s safety.

Most insurance policies require you to take reasonable steps to prevent further damage. Failure to do so could potentially affect your claim.

Plan for Business Continuity

If the vandalism has disrupted your business operations, develop a plan to minimize downtime. This might involve setting up temporary workspaces, renting equipment, or adjusting your business hours. Keep detailed records of any additional expenses incurred due to the vandalism, as these might be covered under your business interruption insurance.

Final Thoughts

Vandalism can disrupt business operations, but understanding your insurance coverage protects your assets. Commercial property insurance typically covers vandalism, offering financial protection against willful damage to your business property. However, you must review your policy carefully, as coverage limits, deductibles, and exclusions vary.

Regular policy reviews ensure your coverage aligns with your business growth and changing risk landscape. As your business evolves, so do your insurance needs. What protected you adequately last year might not suffice today.

At Insurance Brokers of Arizona®, we tailor insurance solutions to meet the unique needs of businesses across Arizona. Our team works with over 40 reputable carriers to provide competitive options for commercial property insurance (including vandalism coverage) and other essential policies. Don’t wait for an incident to discover gaps in your coverage; take proactive steps to protect your business today.