Handyman Coverage Details: What Your Policy Should Include

Handymen face unique risks on every job site, from property damage claims to equipment theft. A standard business policy won’t cut it-you need handyman coverage details tailored to your actual work.

At Insurance Brokers of Arizona®, we’ve seen too many handymen operate with dangerous gaps in their protection. This guide walks you through the coverage components that matter and the gaps that could cost you everything.

What Handyman Insurance Actually Covers

The Building Blocks of Handyman Protection

Handyman insurance isn’t a single product-it’s a customized combination of coverages built around the specific risks you face on job sites. General liability protects you when you accidentally damage a client’s property or someone gets hurt because of your work. Tools and equipment coverage reimburses you for stolen or damaged gear, which matters because the National Association of Home Builders reports that tool theft costs contractors over $1 billion annually. Workers’ compensation covers medical bills and lost wages if you or your employees get injured, and most states require it once you hire even one person.

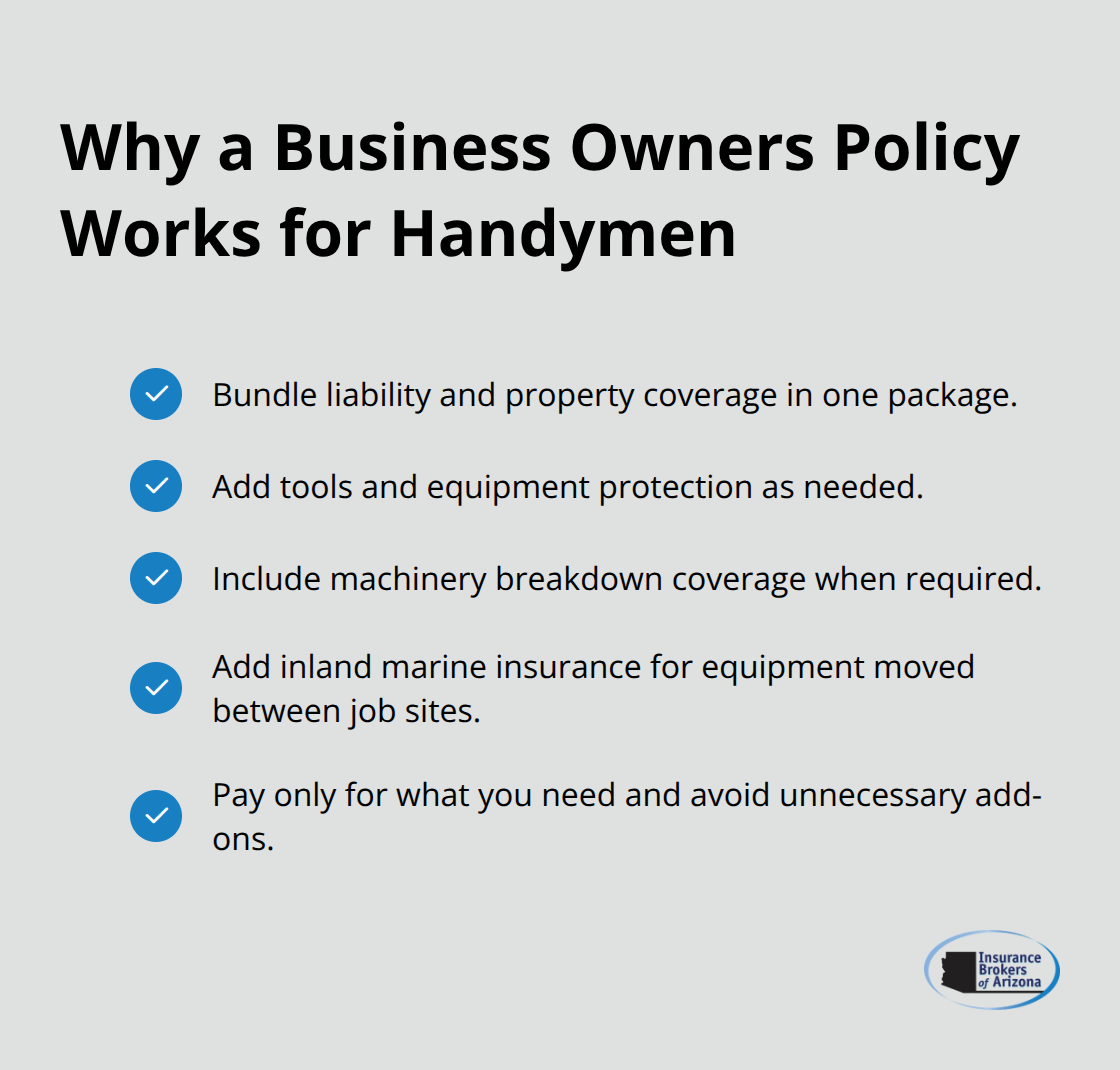

Why a Business Owners Policy Works for Handymen

A Business Owners Policy bundles liability and property coverage into one package, making it easier to customize what you actually need without paying for unnecessary add-ons. This approach lets you add tools and equipment protection, machinery breakdown coverage, and inland marine insurance for equipment transported between job sites. You control what you pay for instead of accepting a one-size-fits-all policy that leaves you exposed or overinsured.

The Hidden Gaps in Standard Business Policies

Standard business policies create massive problems for handymen. A basic commercial general liability policy might cover third-party injuries but completely exclude property damage from tools, equipment theft from your vehicle, or water damage from plumbing work gone wrong. Many policies explicitly carve out lawn care, tree trimming, and roofing tasks-exactly the work handymen do regularly. If a client requires proof of insurance before you start a job, showing up with inadequate coverage won’t cut it.

Real Consequences of Incomplete Coverage

We’ve seen handymen with $500,000 in general liability but zero tools and equipment protection, which means one stolen drill or stolen truck full of equipment wipes out your profit margin for months. The coverage gaps aren’t accidents-they’re exclusions buried in policy language that most handymen never read until a claim gets denied. This is why handyman-specific policies exist: they’re designed around the actual work you do, not the theoretical risks a general contractor faces.

Moving Forward With the Right Protection

Understanding what your policy actually covers separates handymen who stay profitable from those who face financial disaster after a single claim. The next section breaks down each essential coverage component and shows you exactly what to look for when you review your current policy.

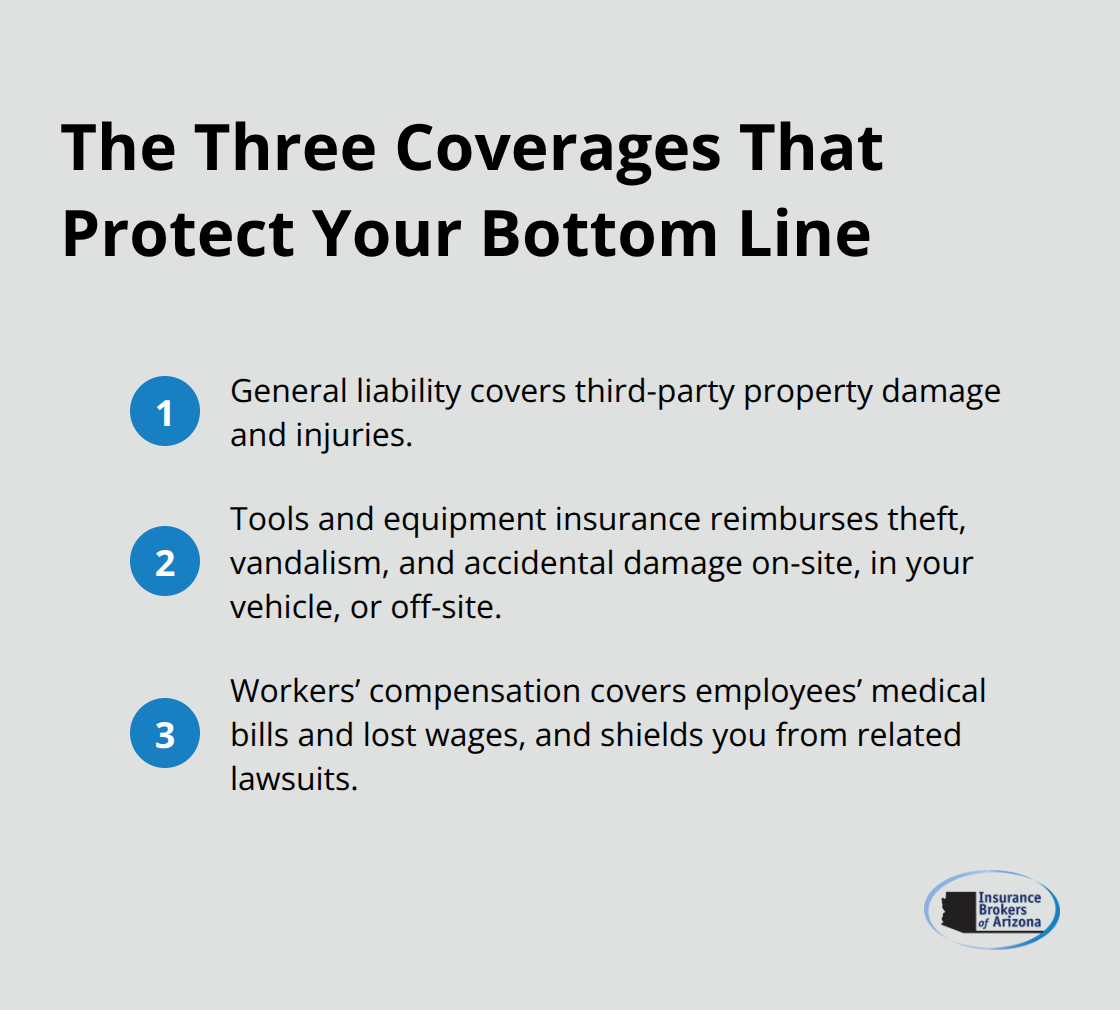

The Three Coverages That Actually Protect Your Bottom Line

General Liability: Your First Line of Defense

General liability covers the damage you cause to someone else’s property or the injuries that happen because of your work. A client’s granite countertop gets scratched during installation, or someone slips on wet flooring you just cleaned-general liability pays for repairs or medical bills up to your policy limit. Most handymen need at least $300,000 in general liability protection, though clients doing commercial work often demand $1,000,000 or higher.

The real issue isn’t understanding what it covers; it’s understanding what it doesn’t. Your general liability policy won’t touch equipment theft, water damage from plumbing mistakes, or injuries to yourself if you’re self-employed. That’s where the gaps start.

Tools and Equipment Coverage: Protecting Your Most Valuable Assets

Tools and equipment coverage fills one of those gaps by protecting the drills, saws, ladders, and power tools you haul to every job. Tool theft from vehicles costs contractors over $1 billion annually according to the National Association of Home Builders, which means one stolen truck full of equipment can wipe out months of profit. This coverage reimburses you for theft, vandalism, and accidental damage to your gear whether it sits on a job site, in your vehicle, or stored off-site.

You need to know your total tool value before you request a quote-list major items like generators, nail guns, and compressors with their replacement costs. Inland marine insurance, which often bundles with tools and equipment coverage, specifically protects equipment transported between locations, making it essential if you move tools daily.

Workers’ Compensation: Protecting Your Team and Your Business

Workers’ compensation is non-negotiable once you hire even one employee, and most states fine you heavily for operating without it. This coverage pays medical expenses and lost wages for injured employees while protecting you from lawsuits related to workplace injuries. Arizona requires workers’ compensation for any business with employees, with penalties including fines up to $2,500 per violation and potential license suspension.

The cost depends on your payroll and job classification-roofing and demolition work costs more to insure than basic repairs because the injury risk is higher. A handyman with a clean claims history pays significantly less than one with multiple incidents, so maintaining a safe workplace directly reduces your premiums. If you’re self-employed with no employees, you can purchase owner’s coverage as an add-on, which covers your medical bills and lost income if you get hurt. This matters because general liability won’t cover your own injuries-only third-party claims.

Bringing It All Together With a Business Owners Policy

A Business Owners Policy bundles general liability and property coverage, then you add tools and equipment protection and workers’ compensation as needed, giving you one organized package instead of managing separate policies from different carriers. This structure lets you control exactly what you pay for while ensuring you don’t leave critical gaps unprotected.

The next section reveals the specific gaps that slip past most handymen-the exclusions and coverage limits that create real financial exposure on your job sites.

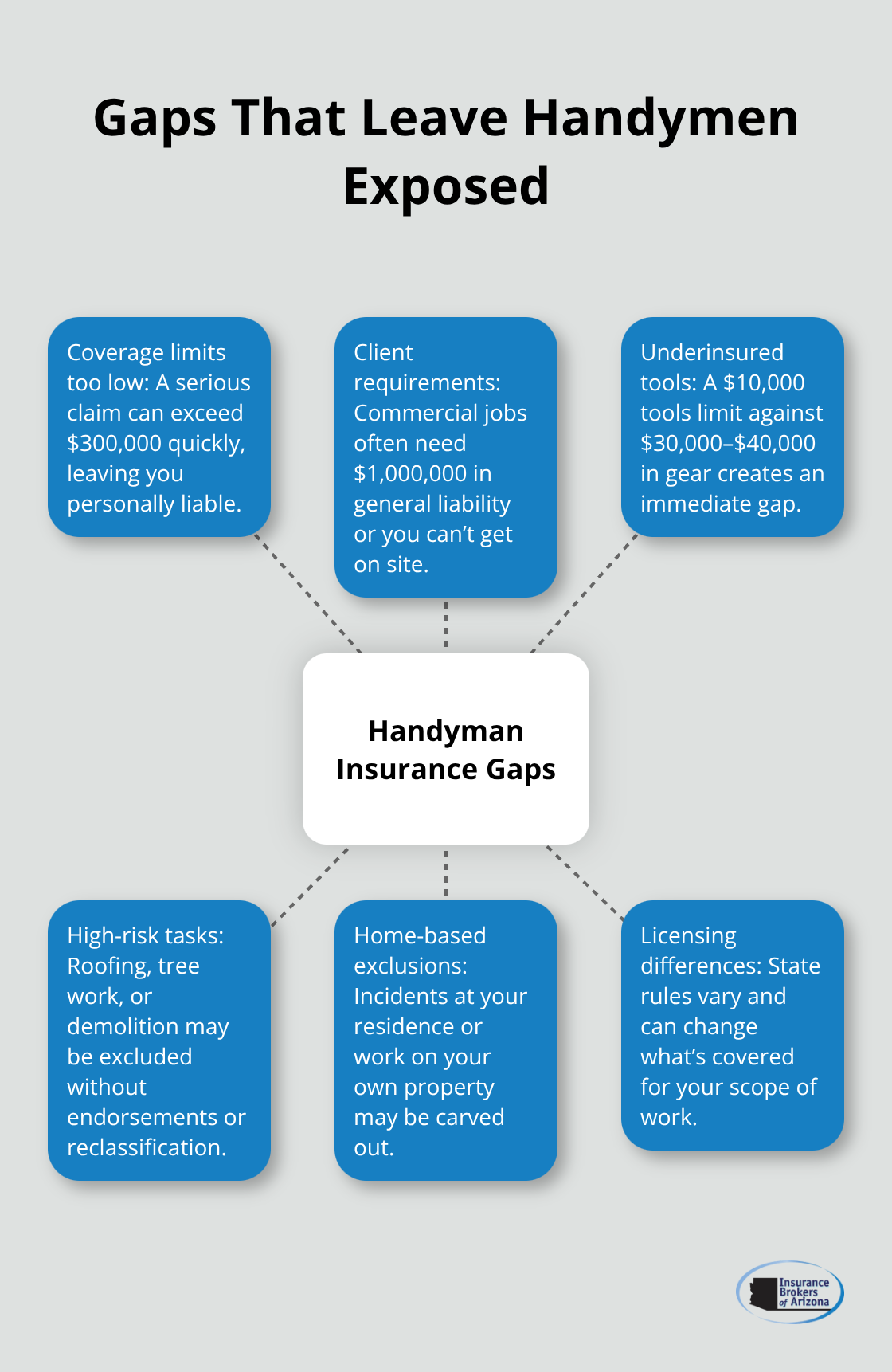

Gaps That Leave You Exposed

Coverage Limits That Vanish Too Fast

Most handymen buy a general liability policy with $300,000 in coverage and assume they’re protected, but that limit disappears quickly when a real claim hits. A single incident-water damage to a client’s home during a plumbing repair, or accidental damage to an expensive appliance during installation-can easily exceed $300,000 in repair or replacement costs. Granite countertops run $3,000 to $5,000 per linear foot, kitchen appliances range from $2,000 to $15,000 each, and structural water damage from a missed pipe can cost $10,000 to $50,000 to remediate. When your policy limit sits at $300,000 and damages reach $75,000, you personally cover anything above that threshold.

Commercial clients almost always require $1,000,000 in general liability before they’ll let you on site, which means inadequate limits don’t just expose you financially-they lock you out of higher-paying work entirely. Tools and equipment coverage has the same trap: handymen often buy $10,000 in equipment protection when their actual tool inventory totals $30,000 or $40,000. One stolen truck full of equipment creates an immediate $20,000 gap you must pay from your business account.

Calculate your total tool value right now-include every power tool, hand tool, ladder, and safety equipment you own-then add 20 percent for items you’ll acquire over the next year. Request a quote based on that real number, not a guess.

High-Risk Tasks That Fall Outside Standard Coverage

High-risk tasks that sit outside standard handyman work demand specialized coverage that most basic policies explicitly exclude. Roofing work, tree trimming, demolition, and anything involving heights or power equipment typically require separate endorsements or entirely different policy classifications. A handyman who occasionally does roof repairs but carries a standard handyman policy discovers mid-claim that roofing work is excluded from coverage.

State regulations vary significantly: Arizona’s licensing requirements differ from California’s, and what qualifies as general handyman work in one state might require a contractor’s license in another. Contact your state’s contractor licensing board to confirm which tasks fall within handyman scope and which ones demand additional credentials or specialized insurance.

Home-Based Business Exclusions That Create Hidden Exposure

Home-based business exclusions create another hidden gap-if you run your operation from home and a client visits your garage to pick up materials or discuss the job, standard policies might exclude any incident that occurs at your residence. Some carriers explicitly carve out work done on your own property, meaning repairs to your own home get no coverage even though you caused the damage.

Before you renew your policy, contact the carrier and ask three specific questions: Does this policy cover the exact tasks I perform most frequently? Are there any geographic or task-specific exclusions that apply to my work? Does coverage extend to incidents at my home address if I operate from there? A broker can review your actual job descriptions against policy language to catch these gaps before they cost you thousands.

Final Thoughts

The handyman coverage details you carry determine whether a single claim strengthens your business or destroys it. You now understand the three essential components-general liability, tools and equipment coverage, and workers’ compensation-and you’ve identified exactly where standard policies fail. These gaps aren’t subtle; they’re exclusions that deny claims when you need them most, coverage limits that evaporate against real-world damages, and task-specific exclusions that leave you personally liable for work you perform regularly.

Pull out your current policy and answer three questions honestly: Does it cover every task you perform? Are your coverage limits based on actual replacement costs, not guesses? Does it include workers’ compensation if you have employees, or owner’s coverage if you’re self-employed? If you hesitate on any answer, your policy has gaps that expose your business to financial disaster.

A broker reviews your actual job descriptions against policy language, identifies exclusions before they cost you money, and compares quotes from multiple carriers to find coverage that fits your specific work. Contact Insurance Brokers of Arizona® to review your current coverage or get a quote for a policy built around your actual work.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.