How to Finance Commercial Truck Insurance Coverage

Commercial truck insurance can drain your operating budget fast. The average commercial truck operator pays between $5,500 and $15,000 annually, depending on vehicle type, driving record, and coverage level.

At Insurance Brokers of Arizona®, we help truck operators navigate commercial truck insurance financing options that actually fit their cash flow. This guide breaks down your costs, payment plans, and proven strategies to reduce what you’re paying.

What Actually Drives Your Truck Insurance Premiums

Your insurance bill isn’t random. Underwriters evaluate concrete factors year-round, and understanding what moves the needle helps you control costs before renewal.

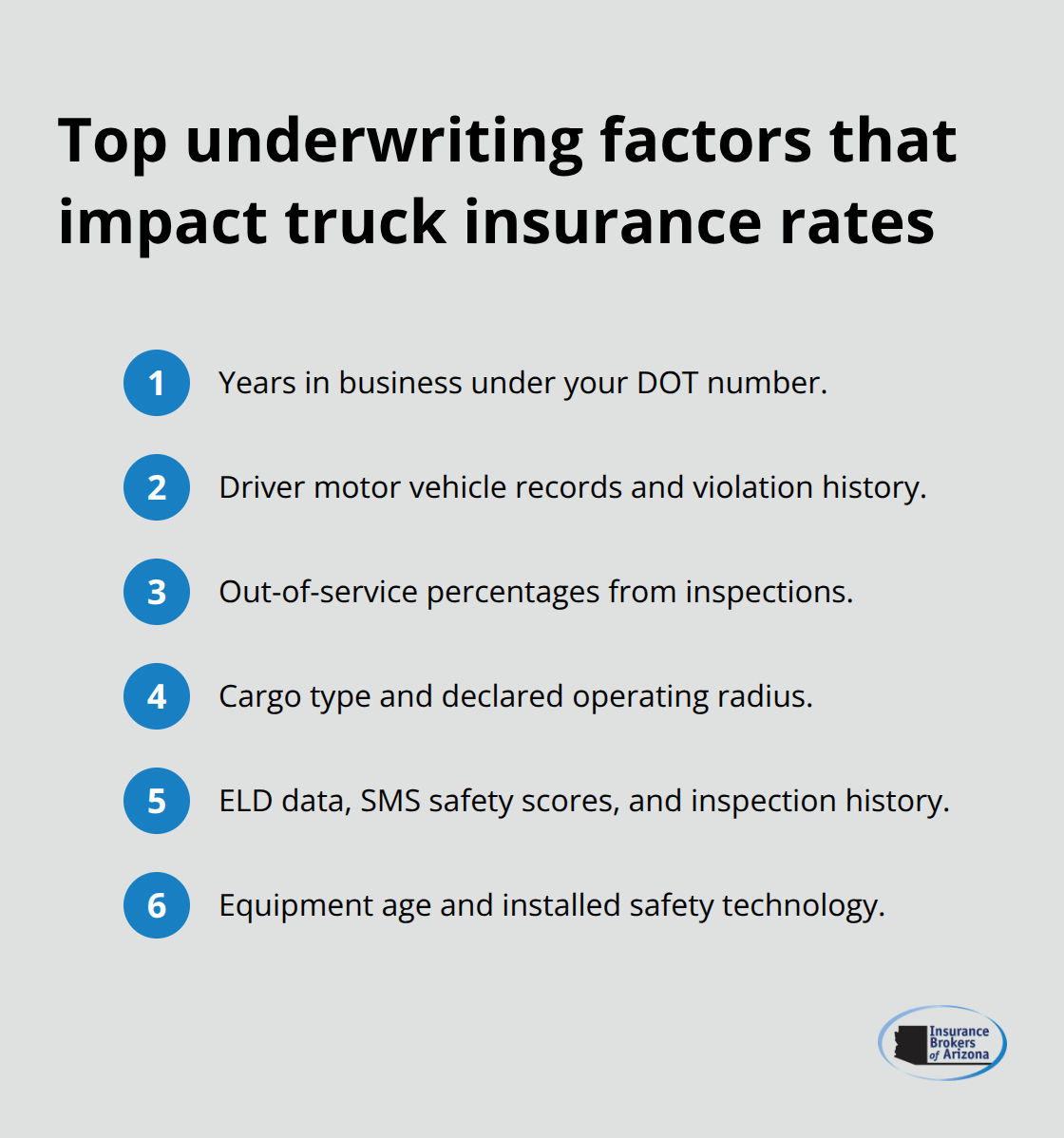

The Underwriting Factors That Matter Most

Years in business under your DOT number, driver motor vehicle records, out-of-service percentages from inspections, cargo type and operating radius, ELD data and safety scores, and equipment age all factor into your rate. According to FreightWaves The Playbook, SMS scores matter year-round, not just at renewal. A single driver with multiple violations or an out-of-service finding can spike your premium by thousands. One-truck operations averaged $11,000 to $16,000 annually in 2023–2024 for primary liability plus cargo coverage. Early 2025 budgets jumped to $12,000 to $17,000 per truck due to tightening markets, higher repair costs, nuclear verdicts, and elevated claims activity.

Why Premiums Keep Rising

This upward pressure isn’t temporary. The trucking insurance market has been hard for years, with premiums rising as some carriers exit the space entirely. Inflation and underwriting dynamics continue pushing rates higher, which means your 2026 renewal won’t be cheaper than last year.

Breaking Down Coverage Costs

Primary liability protects you against at-fault injury and property damage claims, but it covers only third-party losses. Cargo insurance protects freight value and depends entirely on what you haul. A reefer operator carrying temperature-sensitive loads pays more than a dry van operator. Physical damage covers collision, comprehensive, and uninsured motorist protection for your own truck. Non-trucking liability covers you when you’re not under dispatch. Optional add-ons like business interruption, property insurance, auto loss of use, and reefer endorsements add cost but close coverage gaps.

The mistake most operators make is chasing the lowest premium without matching coverage to actual risk. Under-insuring or missing coverage layers costs far more after a loss than paying slightly higher premiums upfront.

How to Strengthen Your Risk Profile

When comparing quotes from multiple carriers, pull fresh motor vehicle records for every driver and perform a mini-audit of your driver qualification files, including medical cards, previous employment verification, and drug and alcohol testing compliance. This documentation strengthens your risk profile in underwriters’ eyes. Start your renewal 90 to 120 days before expiration so brokers have time to shop multiple markets. Waiting until the last 30 days often results in overpriced offers because carriers know you’re desperate.

Newer trucks with modern safety gear like forward-facing cameras, telematics, automatic braking, and lane departure warnings typically qualify for lower rates. One fleet shaved 6% off liability premiums by documenting forward collision avoidance system installations with photos and spec sheets. Operating radius strategy also matters significantly. A 0–300 mile radius costs less than 301–500 miles, which costs less than 500+ miles. If your operation shifts, update filings immediately and verify ELD data aligns with your declared radius. Misalignment can result in surcharges or coverage disputes after a claim.

Now that you understand what drives your costs, the next step is exploring how to actually pay for that coverage without straining your cash flow.

Paying for Truck Insurance Without Killing Cash Flow

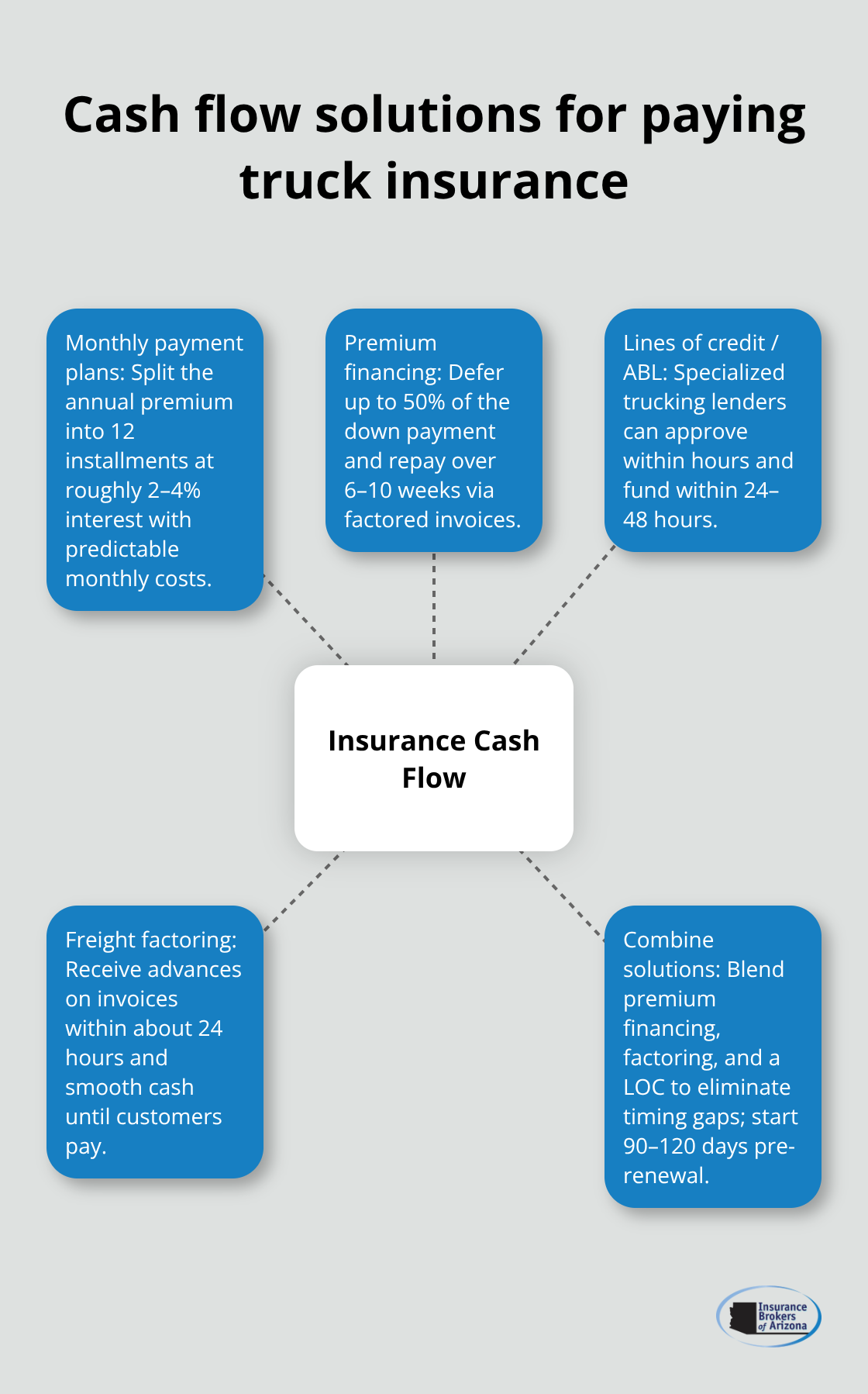

Most truck operators face the same reality: insurance premiums are due upfront, but freight revenue arrives 30 to 60 days later. This timing mismatch forces you to either deplete working capital or find a financing solution that actually works.

Monthly Payment Plans: The Simplest Approach

Start with monthly payment plans through your insurance carrier. Many insurers allow you to split your annual premium into 12 equal installments with minimal interest, typically 2 to 4 percent. The advantage is straightforward: no credit application, no approval delays, and predictable monthly costs that fit your cash flow cycle.

However, monthly plans work only if your annual premium is manageable. If you’re paying $15,000 annually, that’s $1,250 monthly plus interest. For operators with tighter margins, this still strains operations.

Premium Financing: Defer Your Down Payment

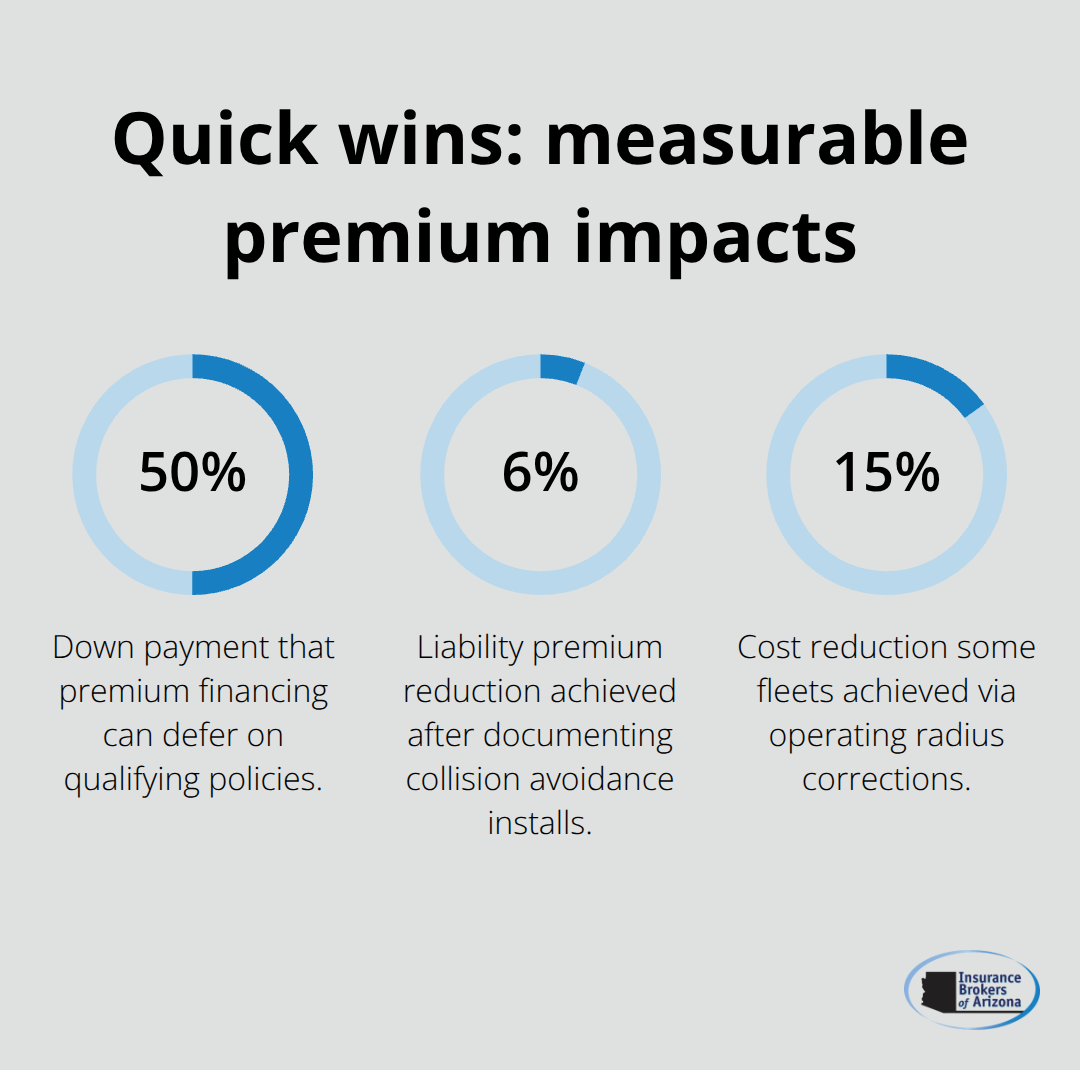

Premium financing offers a different path. A premium financing provider pays your insurer directly upfront, and you repay through factored invoices over 6 to 10 weeks. The structure lets you defer up to 50 percent of your down payment, which is critical for new authorities or operators renewing after a gap.

You collaborate with your insurance agent to confirm coverage and calculate the down payment. The financing provider then covers up to 50 percent of that amount, and you repay the advance via factored invoices as freight revenue arrives. This approach works best for operators with average monthly purchase volume of at least $5,000 and is ideal for flatbed, reefer, step deck, dry van, and hot shot equipment types.

Business Lines of Credit and Asset-Based Lending

Beyond insurance-specific financing, business lines of credit and asset-based lending provide broader working capital solutions. Traditional bank lines require strong credit history and typically take weeks to approve. Specialized trucking lenders move faster and evaluate risk beyond credit scores alone, sometimes approving within hours and funding within 24 to 48 hours.

Freight Factoring: Your Cash Flow Engine

Freight factoring complements insurance financing perfectly. When you factor invoices, you receive up to 100 percent of invoice value within about 24 hours, with the remainder held as a reserve. Once your customer pays, the factor releases the reserve and charges a transaction fee. This steady cash flow lets you pay insurance premiums on schedule, which improves your payment history and strengthens your risk profile with underwriters.

A dedicated account manager and online portal give you transparency and easier cash flow management. Many factoring providers also bundle fuel discount programs that save around 41 cents per gallon at thousands of truck stops, offsetting some financing costs.

Combining Solutions for Maximum Impact

Stop viewing insurance financing as a standalone problem. Combine premium financing with freight factoring and a solid business line of credit, and you eliminate the cash flow squeeze entirely.

Start conversations with your insurance broker 90 to 120 days before renewal so they have time to shop carriers and structure your financing alongside coverage. Rushing this process forces you into overpriced offers or inadequate coverage. Once you’ve locked in your financing strategy, the next critical step is identifying which cost-saving tactics actually move your premium needle.

How to Actually Lower Your Truck Insurance Premiums

Bundle Policies to Unlock Carrier Discounts

Bundling your policies with a single carrier creates leverage that most operators ignore. When you combine primary liability, cargo, physical damage, and non-trucking liability under one insurer, you qualify for discounts unavailable when coverage scatters across three or four carriers. According to FreightWaves The Playbook, bundling with a limited set of insurers provides stability and prevents automatic surcharges from risk fragmentation. A cohesive package tells underwriters you operate a managed business rather than a disorganized collection of risks.

Ask your broker which carriers offer the deepest bundle discounts for your equipment type and operating radius. Lock in that relationship for at least two years so the carrier invests in your safety record instead of repricing you aggressively at renewal.

Implement Formal Safety Programs to Cut Premiums

Your safety record drives real premium movement, and most operators leave thousands on the table here. Proactive risk management discounts apply when you implement formal safety programs-quarterly driver training, written policies on distracted driving and fatigue management, and documented safety meetings. Typical savings run 2 to 5 percent off liability premiums, plus you gain better market acceptance when shopping carriers.

Pull fresh motor vehicle records for every driver before renewal and verify employment history to confirm route and equipment familiarity. Monitor your DOT safety record continuously. Newer trucks with forward-facing cameras, telematics systems, and automatic braking systems qualify for lower rates because they reduce claims frequency. One fleet shaved 6 percent off liability premiums after documenting forward collision avoidance system installations with photos and spec sheets provided to underwriters.

Optimize Your Operating Radius and Equipment Strategy

Your operating radius directly impacts cost. A 0–300 mile radius costs significantly less than 301–500 miles, which costs less than 500+ miles. If your business model shifts toward longer routes, premiums spike unless you proactively update filings and verify ELD data aligns with your declared radius. Equipment age matters equally-maintain robust maintenance records to justify risk reductions, and consider upgrading to newer rigs with safety technology to lower premiums.

Adjust Coverage to Match Actual Risk

Coverage adjustments require discipline but deliver immediate savings. Higher deductibles lower premiums, and targeting at least $1,000 or even $2,500 deductibles makes sense if you maintain a liquidity buffer for claims. Never chase the cheapest policy by slashing coverage you actually need.

Review your cargo values annually against what you actually haul. Eliminate coverage you’ve outgrown, and add endorsements only when shipper contracts require them. This approach prevents overpaying for protection you don’t use while maintaining adequate coverage for the risks you face.

Final Thoughts

Commercial truck insurance financing works best when you treat it as a year-round priority rather than a one-time renewal event. Your underwriting factors-years in business, driver records, equipment age, and safety scores-matter continuously, not just at renewal. Pull fresh motor vehicle records before renewal, document safety improvements with photos and spec sheets, and align your operating radius with actual operations. These actions compound into real savings, with some fleets reducing costs by 15 percent through radius corrections alone.

Premium financing and freight factoring solve the cash flow timing problem that stops most operators. When you defer your down payment through a financing provider and factor invoices for immediate cash, you eliminate the gap between upfront insurance costs and delayed freight revenue. This approach works especially well if your monthly purchase volume exceeds $5,000 and you operate flatbed, reefer, or dry van equipment. Bundling policies with a single carrier prevents surcharges from fragmented coverage, while formal safety programs deliver 2 to 5 percent premium reductions.

We at Insurance Brokers of Arizona® work with truck operators across Arizona to structure commercial truck insurance financing that fits your business. Starting your renewal 90 to 120 days early gives us time to shop multiple markets, package your company story for underwriters, and lock in savings before your policy expires. Contact us to discuss your coverage and financing options.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.