How to Get Bundled Home and Auto Insurance Quotes

Bundling your home and auto insurance can cut your premiums significantly, but finding the right quotes requires knowing what to compare. We at Insurance Brokers of Arizona® help clients navigate this process every day, and we’ve seen firsthand how bundled policies deliver real savings.

Getting bundled home and auto insurance quotes doesn’t have to be complicated. This guide walks you through each step, from gathering your information to evaluating coverage options that actually fit your needs.

Why Bundling Actually Saves Money

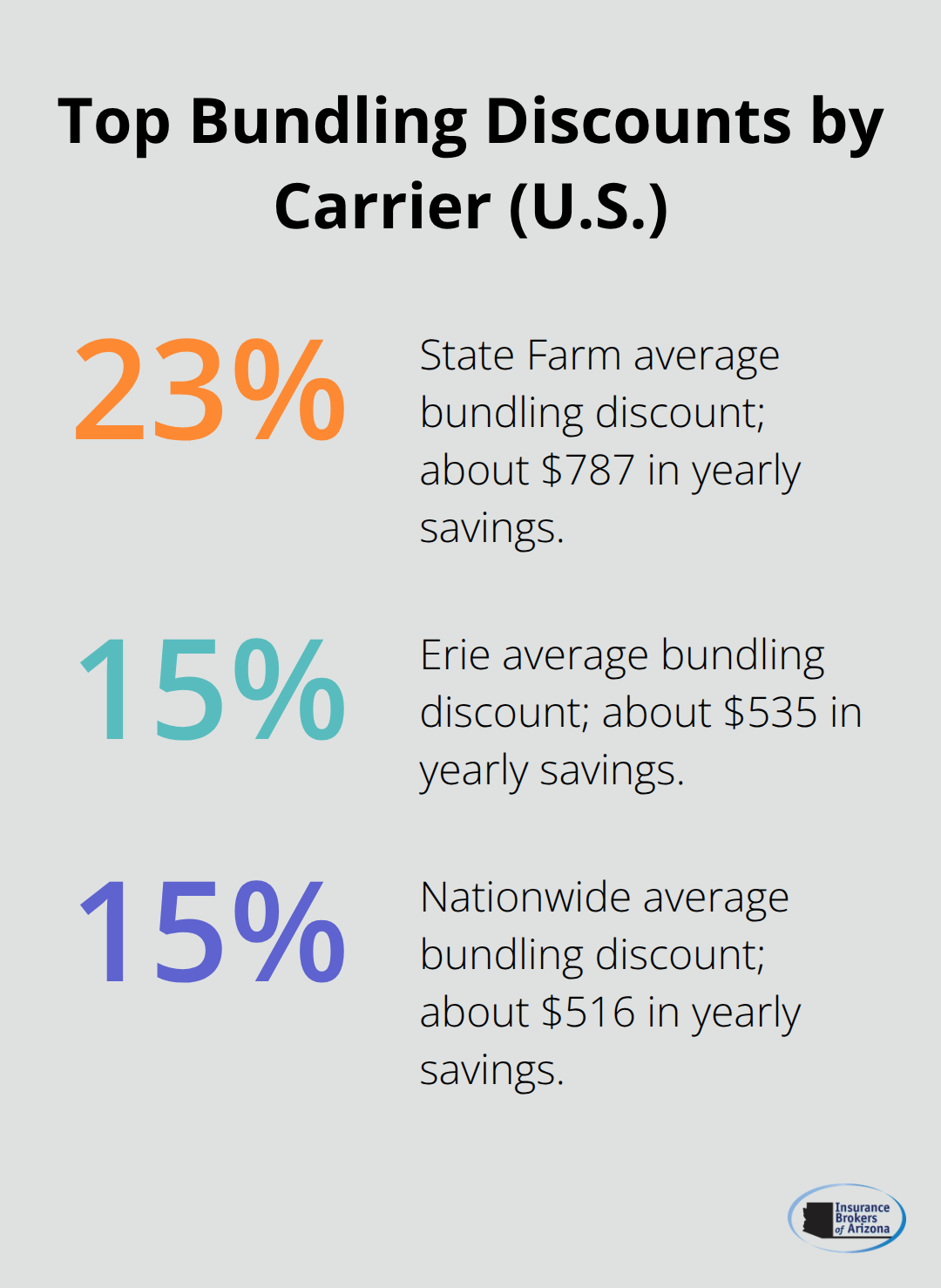

Bundling home and auto insurance works because insurers reward customer loyalty. When you combine policies with one company, they reduce their administrative costs and gain a more stable customer. That savings gets passed to you. Forbes Advisor analyzed bundling discounts across nine major carriers and found an average discount of 14 percent, translating to roughly $466 in annual savings. State Farm leads the pack with a 23 percent average bundling discount, which amounts to about $787 per year for customers who switched between May 2023 and April 2024. Erie offers a 15 percent discount averaging $535 annually, while Nationwide bundles average 15 percent off, around $516 per year.

These aren’t theoretical numbers-they reflect actual customer experiences. The discount applies to both your auto and home premiums, so the savings compound across both policies rather than applying to just one.

The Real Numbers Behind Bundle Savings

The savings range widely depending on which insurer you choose and your specific situation. A Liberty Mutual survey of new customers who switched between May 2023 and April 2024 showed an average savings of $950 per year by bundling auto and home, though this varies significantly by policy and location. Auto-Owners offers a smaller 10 percent average bundling discount at about $214 annually, but their bundled quotes run cheaper overall at roughly $1,878 per year. USAA, limited to military members and their families, offers a 6 percent discount averaging $185 per year but maintains the lowest bundled premiums at approximately $2,630 annually. The point here is clear: bundling typically saves between 5 and 25 percent on total premiums, but the actual dollar amount depends entirely on which carrier you select and the coverage levels you choose.

Bundled Quotes Beat Separate Policies Only Sometimes

This is where most people get confused. A bundled quote isn’t automatically cheaper than purchasing auto and home separately. You must compare the bundled total against the cost of purchasing each policy independently from different insurers. If insurer A quotes you $1,200 for auto bundled with home at a 15 percent discount, but insurer B quotes $800 for auto alone and insurer C quotes $300 for home alone, the separate policies win at $1,100 total. This happens more often than people realize, especially if one carrier dominates the bundled price while competitors excel in specific coverage areas. The convenience of managing one policy, one renewal date, and coordinated claims handling through a single insurer adds real value beyond the discount percentage. However, convenience shouldn’t override price-always obtain quotes from at least three carriers comparing bundled versus separate options side by side (using identical coverage levels and deductibles).

What Comes Next in Your Quote Journey

Now that you understand how bundling discounts work and why they don’t always deliver the lowest total cost, you need to prepare for the actual quote process. The information you collect before requesting quotes determines whether you receive accurate comparisons or inflated estimates that waste your time.

Steps to Get Bundled Home and Auto Insurance Quotes

Collect the Right Information Before You Request Quotes

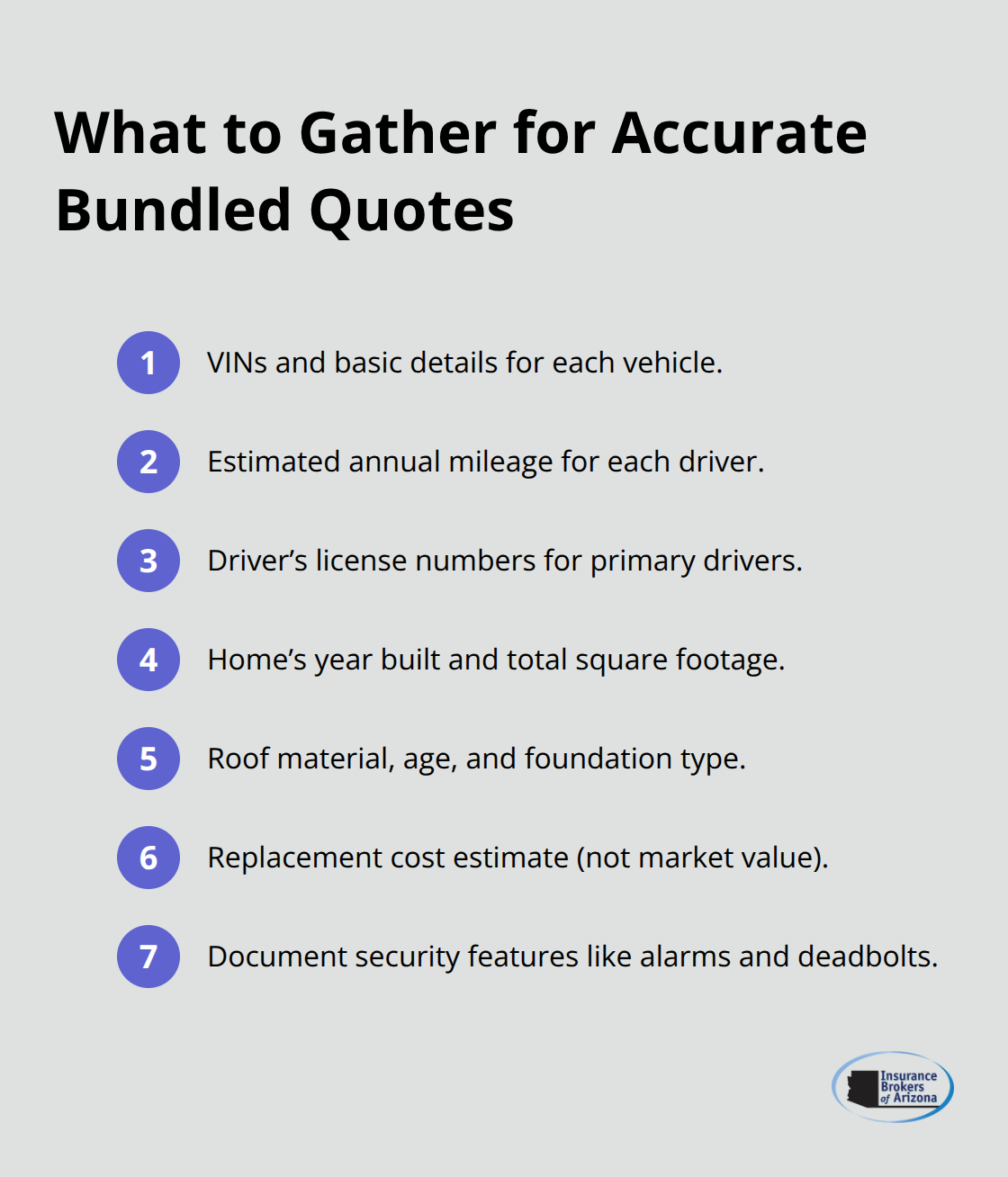

Requesting quotes without proper preparation wastes everyone’s time and produces useless comparisons. You need specific details about your home and vehicles before contacting insurers, and the information you collect determines whether quotes are accurate or wildly off. For your auto policy, collect the Vehicle Identification Number (VIN) for each car you want to insure, current mileage, the primary driver’s license number, and how many miles you drive annually. Insurers use mileage data heavily-driving 5,000 miles per year versus 15,000 miles per year changes your premium significantly. Include information about any safety features like anti-lock brakes, airbags, or anti-theft devices, as these lower your costs.

For your home, gather the year it was built, total square footage, roof material and age, foundation type, and the replacement cost estimate (not the market value). This matters because a 1,200-square-foot home built in 1975 with an asphalt roof costs far more to rebuild than the purchase price suggests. Document your current security features-alarms, deadbolts, fire extinguishers, sprinkler systems-since these qualify for discounts.

Decide Your Coverage Preferences Now

Most importantly, decide your coverage preferences before you request quotes. Higher deductibles reduce premiums but increase your out-of-pocket costs after a claim, so determine what deductible amount you can actually afford to pay. Choose whether you want replacement cost coverage (pays to rebuild or replace items at current prices) or actual cash value (pays depreciated amounts) for your home, as this choice significantly impacts your premium.

Request Identical Quotes from Multiple Insurers

When you request quotes from multiple insurers, use identical information across all of them. This is non-negotiable. If you tell one insurer your home has a 2,000-square-foot replacement cost and another that it has 2,100 square feet, you’re comparing apples to oranges. Request quotes from at least three different carriers using the exact same deductibles, liability limits, and coverage options. Many insurers offer online quote tools that let you enter information directly, but some require phone conversations with agents or brokers. Online quotes often move faster, but agent-based quotes sometimes uncover discounts you’d miss otherwise.

Create a Detailed Comparison Spreadsheet

After you collect quotes, create a spreadsheet comparing premium costs, bundling discounts applied, total annual costs, coverage limits, and available add-on discounts like autopay or paperless billing. Don’t just look at the bundled price-also request separate quotes for auto alone and home alone from each carrier, then add those numbers together to verify whether bundling actually saves you money at that company. Some carriers bundle aggressively on marketing but apply discounts inconsistently, so seeing the math yourself prevents surprises.

Ask each insurer specifically how they calculate their multi-policy discount and whether additional discounts (loyalty, claims-free, security features) stack on top of the bundling discount. This information reveals which carriers truly reward bundling and which ones use it as a marketing tactic without substantial savings. Once you understand the discount structure and have your spreadsheet complete, you’re ready to evaluate which quotes actually meet your coverage needs and fit your budget.

What Actually Matters in Your Bundled Quotes

Your spreadsheet is complete, but now comes the harder part: deciding which quote actually protects you and your finances. Premium price is only one factor, and focusing solely on the lowest number is how people end up underinsured or paying for coverage they don’t need.

Compare Coverage Limits, Not Just Premiums

Start with coverage limits across all your quotes, not just the premium amounts. If one insurer quotes $1,500 annually with $100,000 in liability coverage and another quotes $1,600 with $300,000 in liability, the cheaper option leaves you dangerously exposed if you cause a serious accident. Arizona doesn’t mandate minimum liability limits, but liability limits should match your assets plus future earnings. Someone with a house and savings should carry at least $300,000 in liability coverage, while someone with significant assets should consider $500,000 or more.

Your deductible choice matters just as much as the premium. A $1,000 deductible reduces your annual premium compared to a $500 deductible, but only select the higher deductible if you can actually pay it after a loss without financial strain. Too many people select high deductibles to save $200 annually, then face a $2,000 water damage claim and cannot afford to pay it.

Financial Strength Determines Whether the Company Pays Your Claim

An insurer’s financial strength rating reveals whether they will actually pay when you file a claim. Check each company’s rating from A.M. Best, the industry standard for assessing insurer stability. State Farm, Nationwide, and USAA all maintain A ratings (Excellent) from A.M. Best, meaning they have the reserves to pay claims even during catastrophic events. Smaller regional carriers sometimes offer competitive prices but carry lower ratings, which creates real risk.

NAIC complaint data shows actual customer experiences with claims handling. Auto-Owners has exceptionally low complaint levels for both auto and home policies, while Nationwide sits just below the industry average. State Farm occasionally runs slightly above average in complaint categories, so do not assume the largest carrier automatically delivers the best claims experience.

Request information about how each company handles claims-specifically whether you can file online, through an app, or only by phone. Progressive and State Farm both offer mobile app claims filing, which matters when you need to document damage quickly after an incident. Ask how long claims typically take to resolve and whether the company offers rental car coverage while your vehicle is being repaired or replacement coverage while your home is being rebuilt. These details separate insurers that actually support you during difficult times from those that simply collect premiums.

Stack Discounts to Reveal True Savings

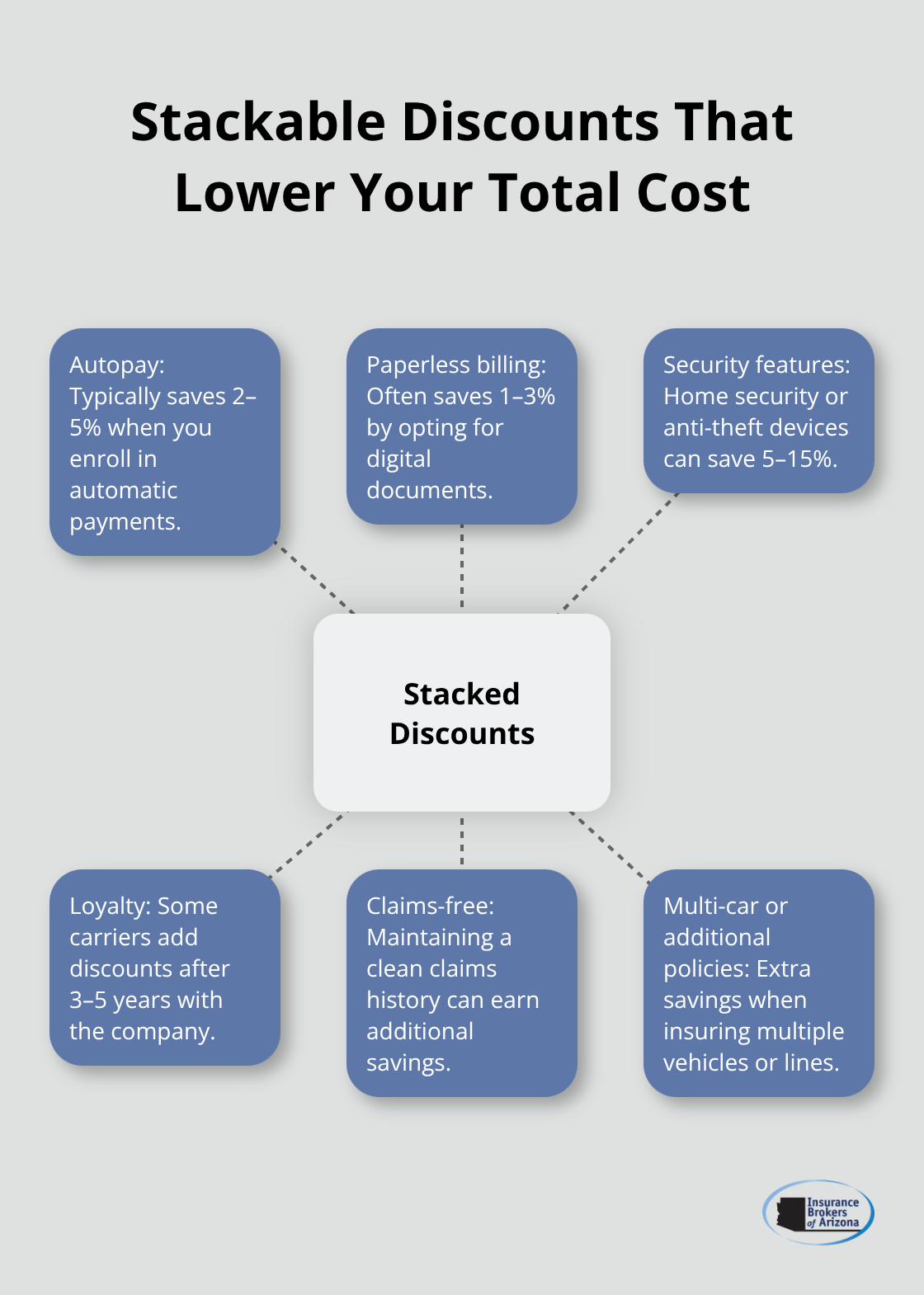

The multi-policy discount is just the beginning. Ask each insurer about additional discounts that stack on top of bundling. Autopay discounts typically save 2 to 5 percent, paperless billing saves another 1 to 3 percent, and safety features like home security systems or anti-theft devices save 5 to 15 percent depending on the carrier.

Some insurers offer loyalty discounts after you have been with them for three or five years, while others reward claims-free records.

Liberty Mutual’s multi-car discount rewards customers who insure more than one vehicle, with bigger savings as you add more cars. Progressive often delivers multi-policy savings exceeding 20 percent for new customers bundling multiple policies, while their typical multi-policy savings run around 7 percent.

Calculate your actual annual cost by applying these stacked discounts to the base premium, not just looking at the headline bundling percentage. A 15 percent bundling discount plus 3 percent autopay plus 5 percent security features equals 23 percent off, which is substantially different from the 15 percent headline number. Ask whether discounts apply permanently or reset annually, since some carriers reduce discounts after the first year to gradually raise your rate.

Final Thoughts

Bundled home and auto insurance quotes require systematic comparison to deliver real financial benefits, but the effort pays off when you approach it strategically. Gather your VINs, mileage, home square footage, roof material, and desired deductibles, then request quotes from at least three carriers using identical coverage levels. Request both bundled and separate quotes from each company to verify whether bundling actually saves you money at that specific carrier.

Coverage limits and deductible amounts matter far more than fixating on the lowest premium, since underinsurance creates greater financial risk than paying slightly more for adequate protection. Pay attention to each insurer’s financial strength rating and complaint history rather than assuming the largest carrier delivers the best claims experience. Stack additional discounts like autopay and security features on top of the bundling discount to reveal your true annual cost.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers and can request bundled home and auto insurance quotes across multiple insurers simultaneously, compare coverage options side by side, and identify which policies fit your needs and budget. Contact Insurance Brokers of Arizona® to let our team handle the comparison process so you move forward with confidence knowing your home and vehicles are properly insured.