Best Auto Insurance for Young Drivers

Young drivers face some of the highest insurance premiums on the road. At Insurance Brokers of Arizona®, we know finding the best auto insurance for young drivers requires understanding what drives up costs and where you can save.

This guide walks you through the real numbers, practical strategies to lower your rates, and how to pick a policy that actually fits your situation.

Why Young Drivers Pay Higher Premiums

The Crash Risk Factor

Teens and young adults face insurance premiums that far exceed what older drivers pay. The reason is straightforward: data shows they crash more. The CDC reports that drivers aged 16–19 are more likely to be in crashes than any other age group, which insurers translate directly into higher risk and higher rates. The Insurance Information Institute notes that crash rates for teen drivers aged 16–19 are nearly three times higher per mile than drivers 20 and older. This statistical reality explains why premiums are so aggressive at the youngest ages.

Real Numbers for Teen and Young Adult Drivers

A 16-year-old added to a parent’s full-coverage policy can push premiums from around $2,671 to as high as $5,910 per year, according to Bankrate data from October 2025. For teens buying their own policy, the numbers climb even higher-an 18-year-old male on a standalone full-coverage plan averages around $7,611 per year. These figures shock most families, but they reflect the actual risk profile insurers assess.

How Rates Drop With Age and Experience

The good news is that rates drop consistently as you age and gain experience. According to Bankrate’s analysis, a 20-year-old pays significantly less than a 16-year-old, and rates continue falling through your mid-twenties. A 20-year-old on a parent’s policy averages around $3,728 per year, while a 25-year-old on the same policy averages about $2,550 per year-a decline of roughly 41% over five years. This pattern holds across most carriers and states, making age one of the most predictable factors in your premium calculation.

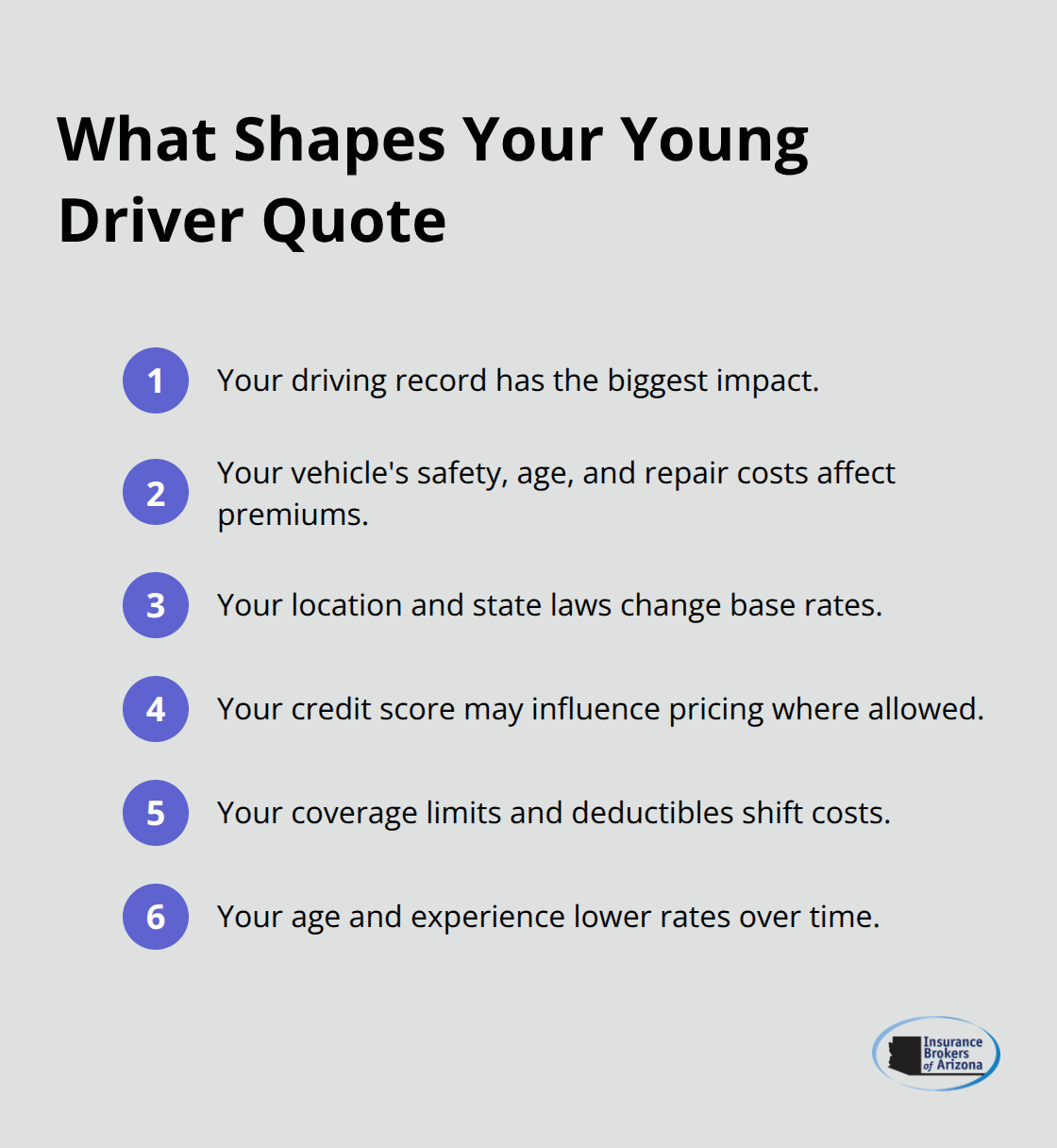

What Else Shapes Your Quote

Several factors beyond age drive your specific quote: your driving record, the vehicle you choose, your location, your credit score (where permitted by state law), and the coverage limits you select. A vehicle matters more than many young drivers realize-choosing an affordable, reliable car with strong safety ratings costs far less to insure than a luxury model. Your state also plays a huge role in pricing; Louisiana averages around $5,468 to add a 16-year-old to a parent’s policy, while North Carolina is substantially cheaper for the same coverage.

Getting Accurate Quotes

When shopping for a quote, you’ll need to provide details like your date of birth, GPA if eligible for student discounts, your license information, and the vehicle’s make and model. Pricing varies dramatically even for identical coverage-some insurers offer premiums in the mid-$3,000 range for young drivers while others charge significantly more for the same protection. This variation makes it essential to compare multiple carriers before you commit to a policy.

How to Cut Your Young Driver Insurance Costs

Keep Your Driving Record Clean

Your driving record is the single most controllable factor in your insurance rate, and it matters far more than most young drivers realize. One accident or ticket raises your premium by hundreds of dollars annually, while a clean record qualifies you for accident forgiveness programs that protect you from rate increases after your first claim. State Farm’s Drive Safe & Save program cuts premiums by up to 30% for low-mileage and safe drivers. Progressive offers accident forgiveness with three tiers, meaning your first accident won’t automatically trigger a rate hike. The math is clear: avoiding even one collision over three years saves you more money than most discount combinations combined. If you already have a violation on your record, focus on maintaining a clean slate going forward-insurers typically review your driving history over the past three to five years, so older incidents gradually lose their impact.

Stack Discounts and Rewards Programs

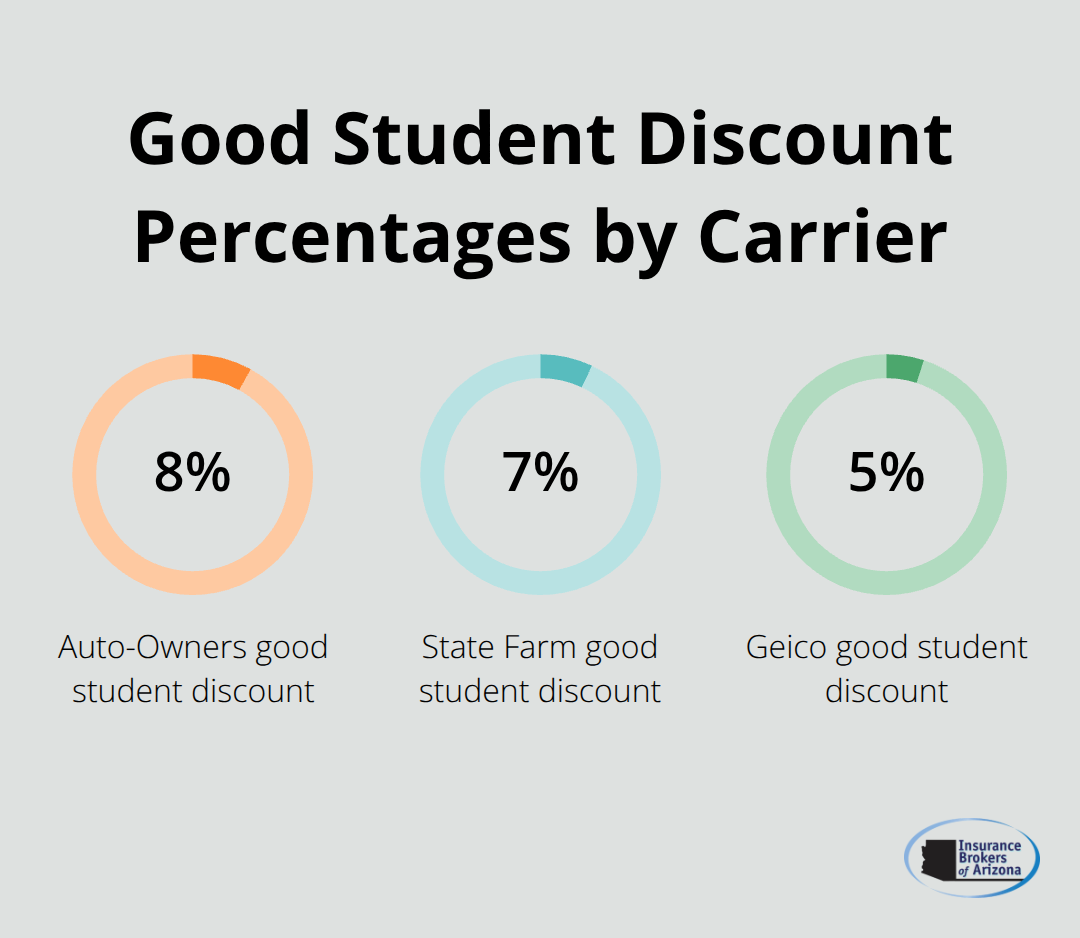

Discounts are where most young drivers leave money on the table. Good student discounts range from 3% to 8% depending on the carrier-State Farm offers 7%, Auto-Owners offers 8%, and Geico offers 5%-so if you maintain a B average or higher, apply immediately. Usage-based insurance programs like Nationwide SmartRide, USAA SafePilot, or Geico DriveEasy reward safe driving behavior and can save 15% to 30% at renewal based on your actual driving patterns rather than age alone.

Bundling auto with renters or homeowners insurance saves over $950 annually according to Liberty Mutual data. Completing a certified teen driving program knocks another 5% off your premium at most carriers.

Choose Your Vehicle and Coverage Strategically

The vehicle itself dramatically affects your rate-a reliable, affordable sedan with strong safety ratings costs far less to insure than a sports car or luxury vehicle. Collision and comprehensive coverage are essential if your car is financed or leased, but if you own an older vehicle outright, raising your deductible from $500 to $1,000 lowers your monthly cost substantially. Coverage limits matter too: carrying liability at 100/300/100 instead of your state’s minimum protects you from catastrophic financial loss if you cause a serious accident, and this protection costs less than you expect when bundled with other discounts. Shopping for the right combination of vehicle choice, deductible level, and coverage limits transforms your premium from unaffordable to manageable.

Finding the Right Insurance for Your Situation

Compare Quotes Across Multiple Carriers

Shopping for auto insurance as a young driver means comparing prices across multiple carriers because rate differences are substantial. Bankrate’s data from late 2025 shows that identical coverage can range from the mid-$3,000s to well over $5,000 annually depending on which company quotes you. Start with at least three to five carriers using the same coverage limits and deductibles so you compare apples to apples.

When you request quotes, have your license information, vehicle details, and GPA ready if you qualify for student discounts. Progressive, Geico, Auto-Owners, and Travelers consistently appear in young driver comparisons, but your specific rate depends entirely on your location, driving record, and vehicle choice. Many carriers let you build quotes online in minutes, though some like Auto-Owners require agent contact. The variation is real: a 20-year-old in one state might pay $3,500 annually while the same driver in Louisiana could face nearly $5,500 for identical protection. The time spent comparing quotes takes an hour but often uncovers $500 to $1,000 in annual savings.

Select Coverage Levels That Protect Your Future

Coverage levels deserve careful attention because state minimums often leave you financially exposed. Most states require liability coverage, but minimums are dangerously low-many sit at 25/50/25, meaning if you cause a serious accident, you’re personally liable for costs exceeding those limits. Carrying 100/300/100 instead costs only marginally more but protects your future earnings if you cause significant damage. Collision and comprehensive coverage are essential if your car is financed or leased, but if you own an older vehicle outright, dropping collision while keeping comprehensive saves money without leaving you stranded.

Evaluate Claims Support and Service Quality

Customer service matters more than young drivers typically admit because claims happen when you least expect them. Progressive offers accident forgiveness and Deductible Savings Bank features that reward safe driving, while State Farm’s Drive Safe & Save program monitors behavior and cuts premiums up to 30% for low-mileage drivers. USAA delivers exceptional service for military families with pay-per-mile options and SafePilot telematics. Check each carrier’s claims process before committing-look for online claim filing, 24-hour support, and favorable repair network ratings through CRASH Network. Some insurers handle claims in hours while others take days, and that difference matters when you need your car back quickly.

Final Thoughts

Finding the best auto insurance for young drivers requires three straightforward actions: understand why you pay more, identify where to cut costs, and compare options across multiple carriers. Your age and driving record shape your premium, but discounts, vehicle selection, and coverage strategy put real control in your hands. A clean driving record saves more money than any discount combination, usage-based programs reward safe behavior with 15% to 30% savings, and bundling your auto policy with renters or home coverage cuts over $950 annually.

We at Insurance Brokers of Arizona® match your specific situation-your age, vehicle, location, and driving record-to coverage and pricing that work for your budget. Our team works with over 40 reputable carriers to find options tailored to your needs rather than pushing unnecessary add-ons, and we handle the comparison work so you avoid contacting multiple insurers yourself. Whether you’re 16 and adding to a parent’s policy or 25 buying your own coverage, we’ve helped thousands of Arizona drivers find policies that protect them without breaking the bank.

Get a personalized quote from our team today and bring your license information, vehicle details, and GPA if you qualify for student discounts. The difference between shopping alone and working with an agent often means hundreds of dollars in annual savings plus coverage tailored to your actual needs. Contact us to see how much you can save on the best auto insurance for young drivers.