How to Find Cheap Auto Liability Insurance

Auto liability insurance protects you financially when you cause an accident, but it doesn’t have to break the bank. Arizona drivers pay an average of $1,200 annually for minimum coverage, yet many overpay by hundreds of dollars.

We at Insurance Brokers of Arizona® see clients cut their premiums by 20-40% using proven strategies. Finding cheap auto liability insurance requires knowing where to look and what factors impact your rates.

Understanding Auto Liability Insurance Requirements

State Minimum Coverage Requirements in Arizona

Arizona law mandates specific minimum liability coverage that costs far less than most drivers realize. You must carry $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $15,000 for property damage per accident. This 25/50/15 structure represents the bare minimum, and the state enforces these requirements strictly. Violations trigger immediate penalties that include license suspension and fines up to $750 plus reinstatement fees.

Difference Between Liability and Full Coverage

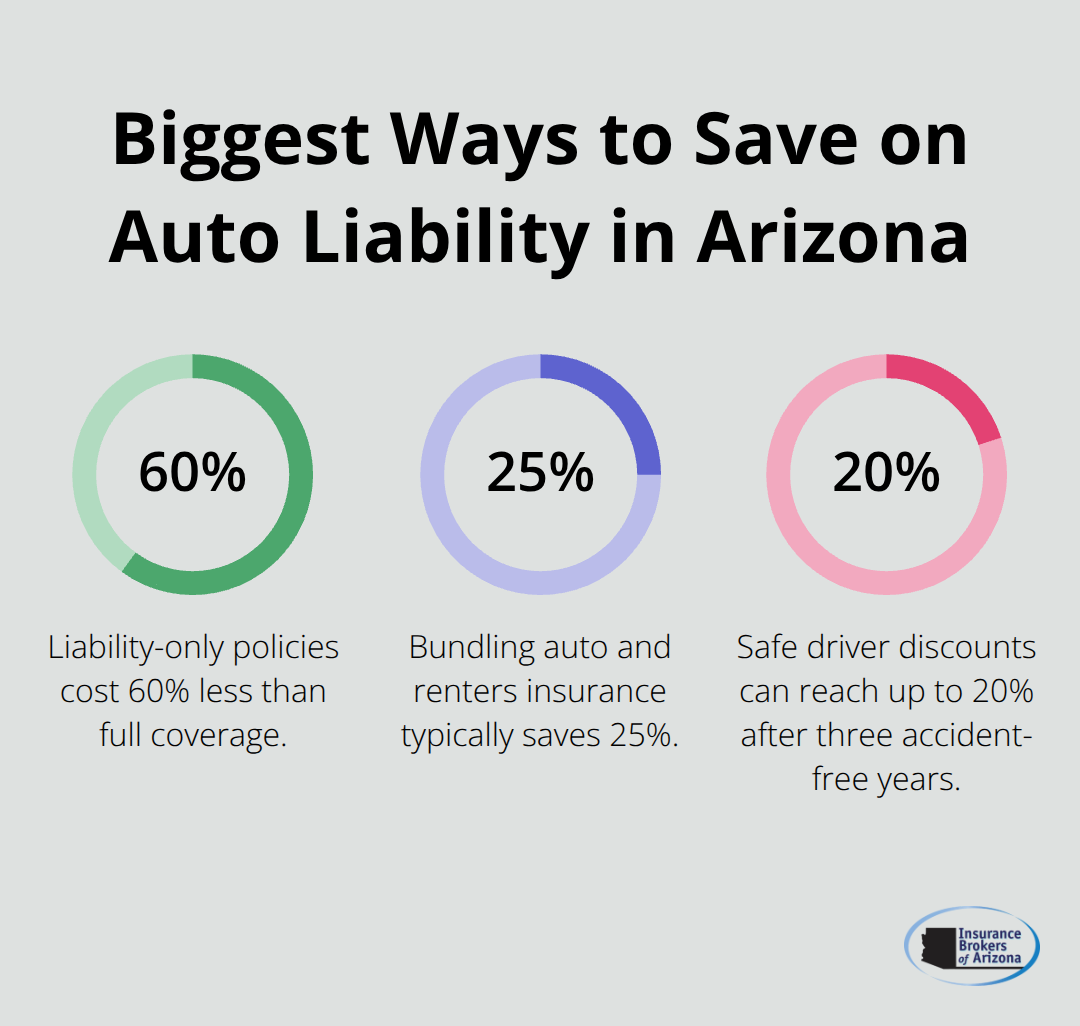

Liability coverage only pays for damage you cause to others, never your own vehicle or medical bills. Full coverage adds comprehensive and collision protection for your car, which typically doubles or triples your premium. Most Arizona drivers need only liability coverage if their vehicle is worth less than $5,000 or they own it outright. The Insurance Information Institute reports that liability-only policies cost 60% less than full coverage, which makes this decision your biggest potential savings opportunity.

Financial Responsibility Laws and Penalties

Arizona’s Motor Vehicle Division imposes harsh consequences for drivers who operate vehicles without insurance. First-time offenders face three-month license suspension, $500 fine, and must file SR-22 proof of insurance for three years. Second violations within three years result in six-month suspension and $750 fine. The state requires immediate proof of coverage when officers conduct traffic stops, and they can impound your vehicle on the spot without insurance verification. These penalties cost thousands more than minimum coverage (which averages just $100 monthly in Arizona).

Now that you understand Arizona’s requirements, the next step involves finding ways to reduce these costs without sacrificing protection.

Strategies to Lower Your Auto Liability Insurance Costs

The most effective strategy for reducing your auto liability insurance costs involves comparing quotes from at least five different insurers, as rates vary dramatically between companies for identical coverage. The National Association of Insurance Commissioners found that drivers who shop around save an average of $1,000 annually, yet 73% of Arizona drivers stick with the same insurer for over three years without comparing alternatives. Progressive might quote you $150 monthly while GEICO offers $95 for identical 25/50/15 coverage based on your specific risk profile.

Shop Around and Compare Multiple Quotes

Smart drivers request new quotes twice yearly because insurance companies adjust their pricing algorithms constantly, and your personal risk factors change over time. The Zebra’s analysis of 74 million quotes shows that rates fluctuate by 15-30% quarterly for the same driver profile. State Farm might offer your best rate in January, but Farmers could beat them by $400 in July. Online comparison tools streamline this process, but direct calls to insurers often yield additional discounts not available through third-party websites.

Take Advantage of Available Discounts

Arizona insurers offer dozens of discounts that can reduce your liability premiums by 35% or more when you combine them strategically. Bundling auto and renters insurance typically saves 25%, while maintaining accident-free records for three years earns safe driver discounts up to 20%. Military members, federal employees, and college graduates qualify for exclusive discounts with companies like GEICO and USAA. Installing anti-theft devices, completing defensive driving courses, or paying premiums annually instead of monthly can each knock 5-10% off your rates.

Improve Your Credit Score

Credit score improvements above 700 trigger significant rate reductions, as insurers view good credit as a predictor of responsible driving behavior according to Insurance Information Institute research. Poor credit can increase your car insurance rates by hundreds of dollars annually compared to good credit (with exceptions in California, Hawaii, and Massachusetts where credit scores cannot affect rates). Most insurers check your credit score when you apply for coverage and at renewal periods.

Your driving record and vehicle choice also play major roles in determining your final premium rates.

Factors That Affect Your Auto Liability Insurance Rates

Age and Experience Drive Premium Differences

Your age dramatically impacts liability insurance costs, with drivers under 25 paying 60% more than those over 25 according to Insurance Information Institute data. Teen drivers face the highest rates because they cause accidents at three times the rate of experienced drivers, while rates drop significantly at age 25 when brain development completes and risk-taking behavior decreases.

Drivers over 50 receive the lowest rates until age 70, when premiums increase again due to slower reaction times and vision changes. Insurance companies price policies based on actuarial tables that show 16-year-old drivers cost insurers $4,500 annually in claims compared to $1,200 for 45-year-old drivers.

Vehicle Choice Affects Your Premium More Than You Think

Sports cars and luxury vehicles cost 40-80% more to insure than practical sedans because they attract theft, cost more to repair, and encourage aggressive behavior. A Honda Civic costs an average of $1,100 annually to insure while a Chevrolet Corvette runs $2,400 for identical coverage in Arizona. Safety features like automatic emergency braking, blind spot monitoring, and anti-theft systems can reduce your rates by 10-15% because they prevent accidents and theft. Older vehicles worth less than $5,000 make excellent choices for liability-only coverage since comprehensive and collision become unnecessary expenses.

Credit Score Impact Varies by State

Arizona allows insurers to factor credit scores into rate calculations, and poor credit increases premiums by $800-1,200 annually compared to excellent credit according to NerdWallet research. Insurance companies correlate credit responsibility with responsibility behind the wheel, though this practice faces scrutiny. Better credit scores from fair to good can reduce your liability insurance costs by 20-30% within six months. Payment history accounts for 35% of your credit score (the largest factor), so you should pay all bills on time to create the fastest improvement path for insurance savings.

Location and Mileage Matter

Your ZIP code determines a significant portion of your premium because insurers analyze accident rates, theft statistics, and repair costs by geographic area. Urban drivers in Phoenix pay 25-40% more than rural Arizona residents due to higher traffic density and crime rates. Annual mileage also affects your rates, with low-mileage drivers (under 7,500 miles yearly) qualifying for discounts up to 15% through usage-based insurance programs that track your actual miles.

Final Thoughts

Cheap auto liability insurance requires a systematic approach that combines smart shopping with strategic decisions. Request quotes from at least five insurers every six months, as rates fluctuate constantly and companies adjust their pricing algorithms regularly. Focus on maximizing available discounts through policy bundling, clean driving records, and credit scores above 700.

Arizona’s 25/50/15 requirements protect you legally but may not cover major claims that exceed these limits. Consider increasing your liability limits to 100/300/50 if your net worth exceeds $50,000 (this additional protection costs only $15-25 monthly but prevents potential bankruptcy from large judgments). Choose practical vehicles with strong safety ratings while avoiding sports cars and luxury models that inflate premiums unnecessarily.

We at Insurance Brokers of Arizona® help Arizona drivers secure optimal coverage while maintaining affordability through strategic carrier selection and discount optimization. Our personalized approach connects you with competitive rates that match your specific needs and budget. Contact us today to explore your options for affordable liability coverage.