How to Find the Lowest Cost Auto and Home Insurance

Insurance costs continue rising across the United States, with the average American household spending over $2,400 annually on auto and home coverage combined.

We at Insurance Brokers of Arizona® know that finding the lowest cost auto and home insurance requires more than just comparing prices. Smart consumers focus on coverage quality, carrier stability, and long-term value when making these important financial decisions.

What Factors Control Your Insurance Costs

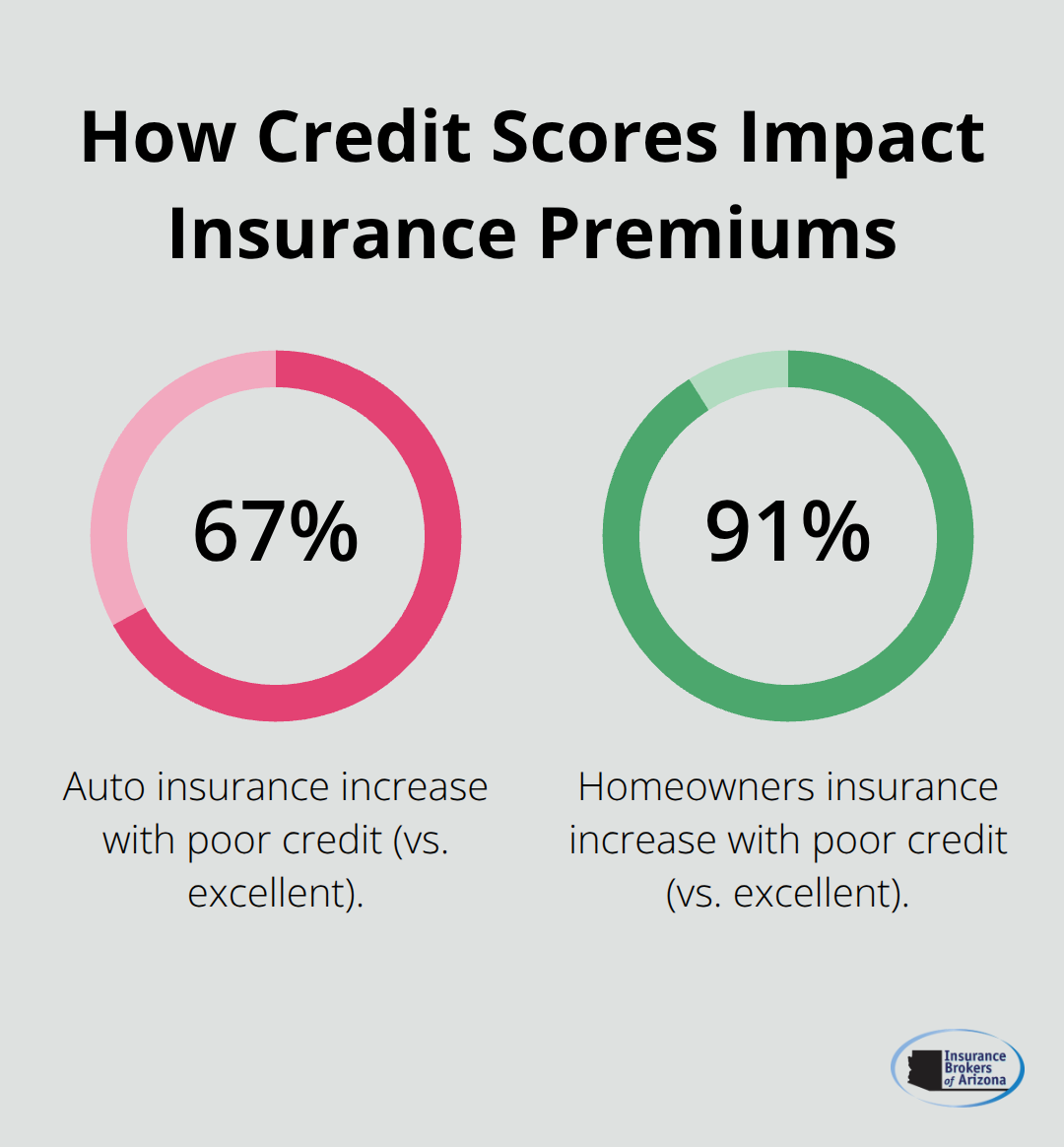

Your credit score impacts insurance premiums more than most people realize, with insurers in 47 states using credit-based insurance scores to calculate rates. A poor credit score can increase your auto insurance by 67% and homeowners coverage by 91% according to the Insurance Information Institute. The difference between excellent and poor credit translates to over $1,400 annually in extra premiums for combined auto and home coverage.

Credit Score Creates the Biggest Premium Gaps

Credit score improvement from fair to good can cut insurance costs by 15-25% within six months. Pay down credit card balances below 30% utilization, dispute errors on your credit report, and set up automatic payments for all bills. Insurance companies view credit scores as predictors of claim frequency, which makes this the single most impactful factor you can control.

Deductible Selection Determines Your Premium Base

Higher deductibles reduce your premiums substantially. A $1,000 deductible instead of $500 reduces homeowners insurance by approximately 25% and auto coverage by 15-30%. However, choose deductibles you can afford during emergencies. Most financial advisors recommend keeping three to six months of expenses in emergency savings before you select higher deductibles (this strategy works best for responsible drivers and homeowners with minimal claim histories).

Location Risk Drives Regional Rate Variations

Insurance companies analyze ZIP code data that includes crime rates, weather patterns, and traffic accident frequency. A move of just a few miles can change your rates significantly. Los Angeles saw nearly 20% increases in home insurance rates during 2024 due to wildfire risks, while North and South Carolina experienced 7% jumps from flood concerns. Urban areas typically cost 20-40% more for auto coverage than rural locations due to higher theft and accident rates.

Coverage Limits Shape Your Base Rates

Higher coverage limits increase premiums but provide better protection against major losses. State minimum liability coverage costs less upfront but leaves you vulnerable to lawsuits that exceed basic limits. Full coverage with comprehensive and collision protection costs more but protects your vehicle investment (especially important for newer cars with outstanding loans).

These cost factors work together to determine your final premium, but smart strategies can reduce these expenses significantly.

How Can You Cut Your Insurance Costs

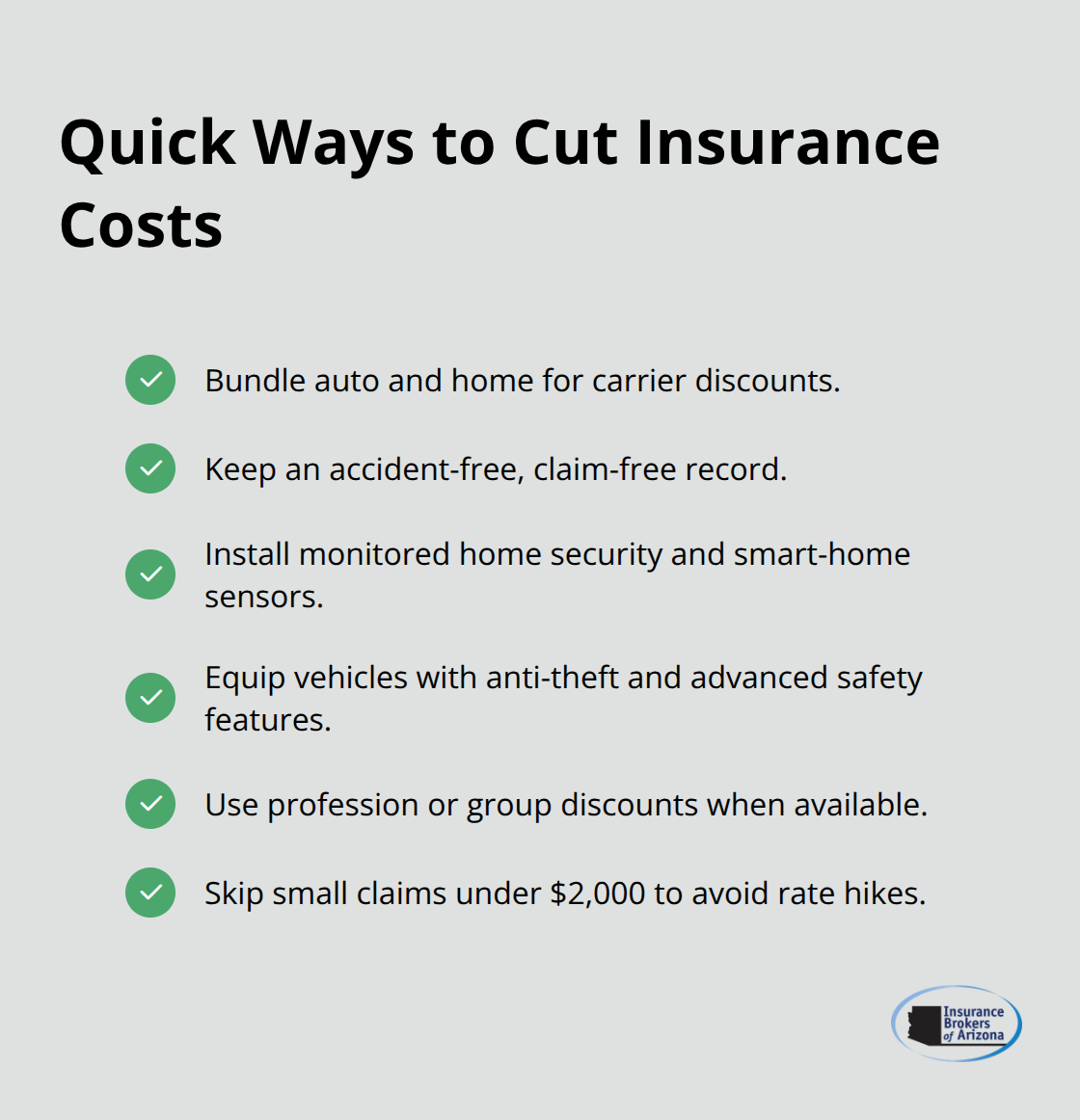

Bundled auto and home insurance delivers the most immediate savings, with State Farm offering nearly 25% off combined policies and Amica providing up to 30% discounts when you add umbrella and life coverage. Customers save $950 annually on average through bundled policies, according to Liberty Mutual data. However, bundled coverage only makes sense when the combined discount exceeds what you would pay for separate policies from different carriers. Compare bundled rates against individual quotes from companies like Geico for auto coverage and Amica for homeowners protection.

Clean Records Generate Compound Savings

Insurance companies reward customers with spotless records through substantial discounts that increase over time. Progressive offers up to 13% off for accident-free periods, while most carriers provide 5-15% reductions after three claim-free years. Small claims actually hurt you financially since Bankrate research shows premiums rise 6% after theft, liability, or fire claims. Skip claims under $2,000 and pay out of pocket to protect your rates. The Insurance Information Institute confirms that fewer claims keep premiums lower long-term, making this strategy worth thousands over a decade.

Security Features Cut Rates Through Risk Reduction

Monitored security systems reduce homeowners premiums by 5-20% depending on the system sophistication. Smart home technology like water leak detectors and security cameras qualify for additional discounts at many carriers. Vehicle safety features including anti-theft systems, backup cameras, and automatic emergency braking lower auto rates by 10-25%. Farmers Insurance specifically rewards professional drivers like teachers and firefighters with specialized discounts (anti-lock brakes, airbags, and electronic stability control are standard features that many insurers factor into lower base rates automatically).

Professional and Group Discounts Add Extra Value

Many carriers offer profession-specific discounts that stack with other savings opportunities. Teachers, firefighters, and military personnel often qualify for 5-10% additional reductions through specialized programs. Group insurance through employers can provide access to rates not available to individual consumers (BenefitHub data shows employees save around $1,092 annually through employer-provided policies). These discounts combine with safety features and clean records to maximize your total savings.

Smart quote comparison becomes essential once you understand these cost-reduction strategies.

What Makes Quote Comparison Actually Work

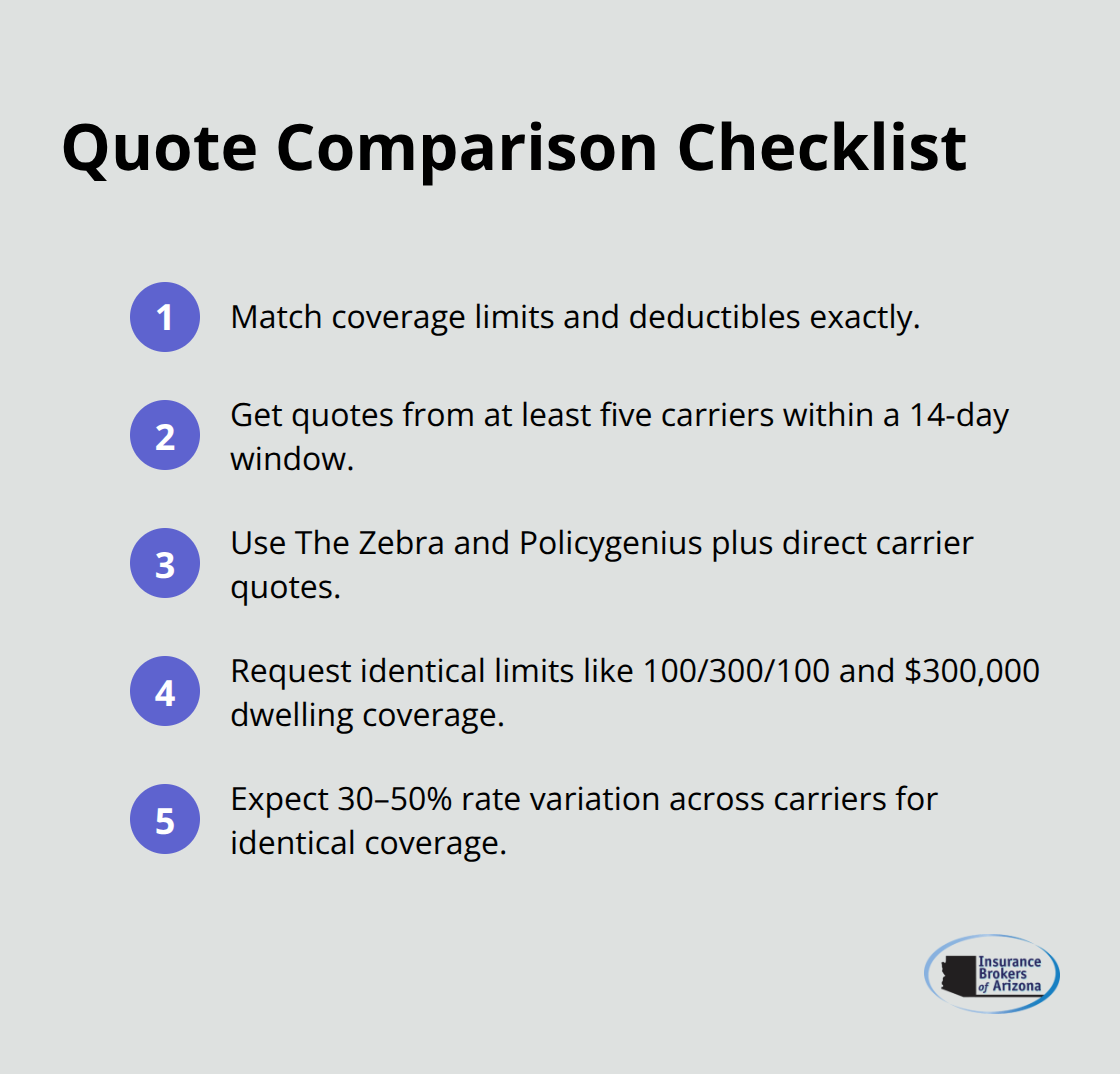

Accurate insurance quotes require identical coverage limits and deductibles from at least five different carriers within a 14-day window. Rate variations of 30-50% between companies for identical coverage are common, with some drivers seeing differences that exceed $1,000 annually. Online comparison tools like The Zebra and Policygenius streamline this process, but direct carrier quotes often reveal additional discounts that comparison sites miss. Request quotes for the same coverage amounts, such as $100,000/$300,000/$100,000 liability limits for auto insurance and $300,000 dwelling coverage for homeowners policies.

Financial Strength Ratings Prevent Future Problems

A.M. Best ratings of A- or higher indicate carriers with strong financial stability to pay claims during catastrophic events. Companies rated B+ or lower face higher risks of delayed claim payments or coverage disputes during major disasters. Liberty Mutual holds an A rating from A.M. Best, while smaller regional carriers may offer lower premiums but lack the financial reserves for widespread claims. The 2017 hurricane season revealed how financially weaker insurers struggled with claim volume and left policyholders waiting months for settlements. Check multiple rating agencies including Standard & Poor’s and Moody’s, as ratings can vary between agencies.

Coverage Details Determine Real Value

Policy language differences create coverage gaps that cheap quotes often hide. Replacement cost coverage for homeowners insurance costs 20-30% more than actual cash value but pays full replacement without depreciation deductions. Auto policies with original equipment manufacturer parts cost more upfront but prevent inferior aftermarket repairs that reduce vehicle value. Deductible structures vary significantly between carriers (some offer disappearing deductibles that decrease over claim-free years while others maintain fixed amounts). Compare coverage territories, as some carriers restrict coverage during travel or exclude certain high-risk activities that standard policies cover.

Quote Timing Affects Rate Accuracy

Insurance rates change frequently based on market conditions and carrier profitability targets. Quotes remain valid for 30-60 days depending on the carrier, but rates can shift during this period. Shop for quotes during renewal periods rather than mid-policy to avoid cancellation fees and coverage gaps. Most carriers offer their best rates to new customers (existing policyholders often pay higher renewal premiums than identical new customer rates). Request all quotes within the same week to maintain rate consistency across carriers.

Final Thoughts

Smart consumers secure the lowest cost auto and home insurance through systematic comparison and strategic choices. Credit score improvement creates the largest premium reductions, while bundled policies save money when combined discounts exceed separate coverage costs. Clean records and security features compound these savings over time.

Quote comparison from five carriers with identical coverage limits reveals rate differences that often exceed $1,000 annually. Financial stability matters more than rock-bottom prices since weak insurers delay claim payments during disasters. Policy details determine real value beyond premium costs (replacement cost coverage prevents depreciation deductions that cheap policies often exclude).

Annual policy reviews catch rate increases and identify better options before renewal periods arrive. Insurance markets shift constantly as carriers adjust rates based on profitability and regional risks. We at Insurance Brokers of Arizona® help clients compare options from multiple reputable carriers to find competitive rates that match specific coverage needs.