Auto Insurance Tips for New Drivers

Getting auto insurance as a new driver feels overwhelming with countless coverage options and confusing terms. Arizona requires specific minimum coverage, but many new drivers don’t understand what they actually need.

We at Insurance Brokers of Arizona® see new drivers make costly mistakes that could easily be avoided. The right knowledge can save you hundreds of dollars annually while protecting you properly on the road.

Understanding Auto Insurance Basics for New Drivers

What Coverage Do Arizona Drivers Actually Need?

Arizona mandates liability insurance with minimum limits of $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 for property damage. These minimums provide inadequate protection. A single accident can easily exceed $25,000 in medical costs and leaves you financially exposed.

We recommend 100/300/100 coverage instead – $100,000 per person, $300,000 per accident, and $100,000 property damage. This higher coverage costs roughly $200-300 more annually but protects your assets from lawsuits. The extra cost proves minimal compared to potential financial devastation from a serious accident.

How Insurers Calculate Your Premium

Insurance companies use specific factors to determine your rates. Age plays the biggest role – 16-year-old drivers pay an average of $6,701 annually for males and $5,969 for females (according to The Zebra). Your ZIP code significantly impacts costs, with urban areas like Phoenix seeing higher premiums due to accident frequency.

Vehicle choice matters tremendously. Sports cars can increase premiums by 40-60% compared to sedans. Credit score affects rates in Arizona, with poor credit adding $1,000-2,000 annually. Insurers also consider your grades if you’re a student, with B averages qualifying for discounts.

Terms That Impact Your Wallet

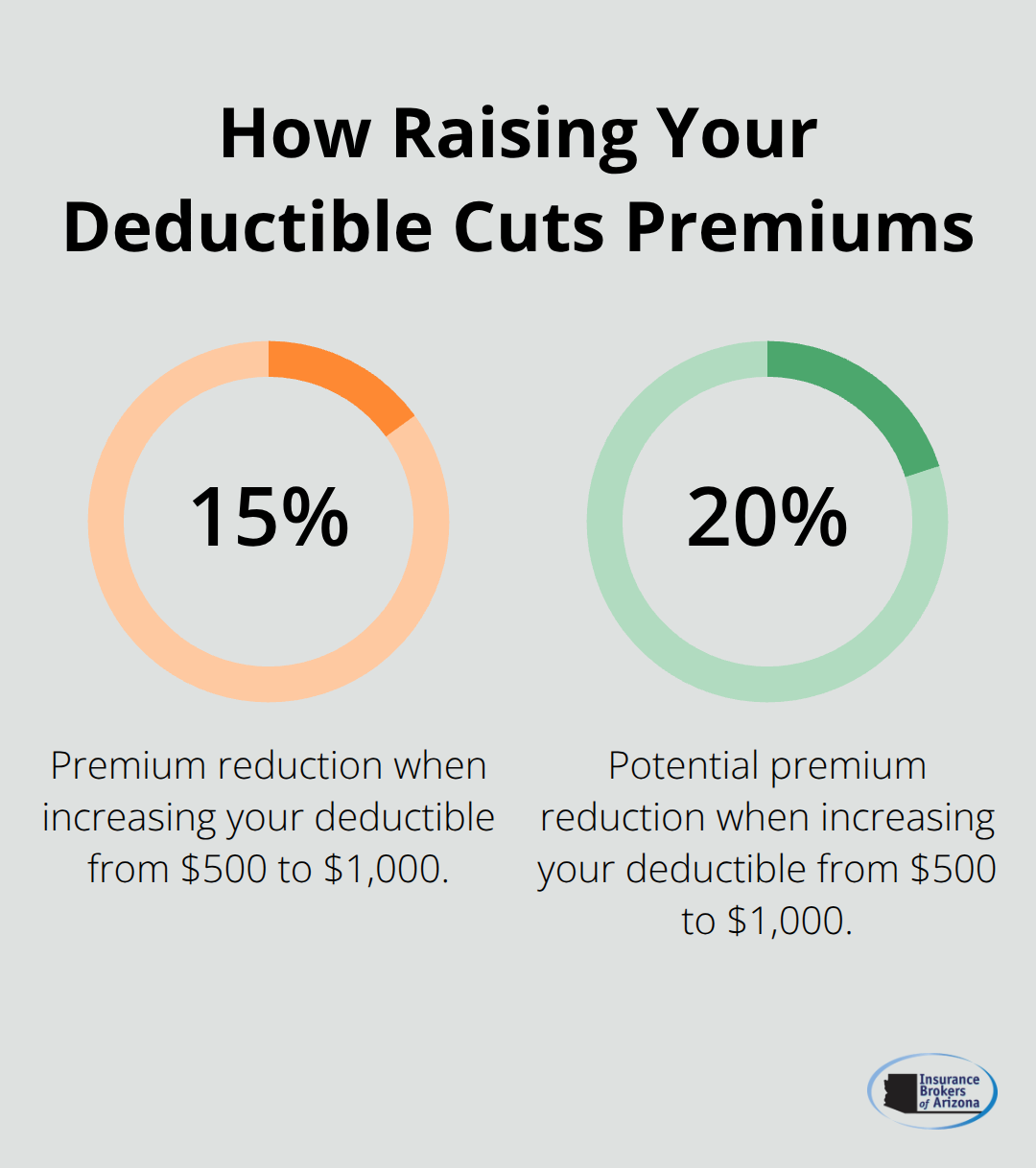

Deductibles directly affect your premium and out-of-pocket costs. Raising your deductible from $500 to $1,000 typically reduces premiums by 15-20%. Collision coverage pays for your vehicle damage regardless of fault, while comprehensive covers theft, vandalism, and weather damage.

Uninsured motorist coverage protects against Arizona’s estimated 13% uninsured drivers. Personal injury protection covers medical expenses regardless of fault. These terms help you make informed decisions rather than accept whatever an agent suggests.

Smart coverage choices set the foundation, but new drivers can take additional steps to reduce their insurance costs significantly.

Ways to Lower Auto Insurance Costs as a New Driver

Academic Performance Pays Real Money

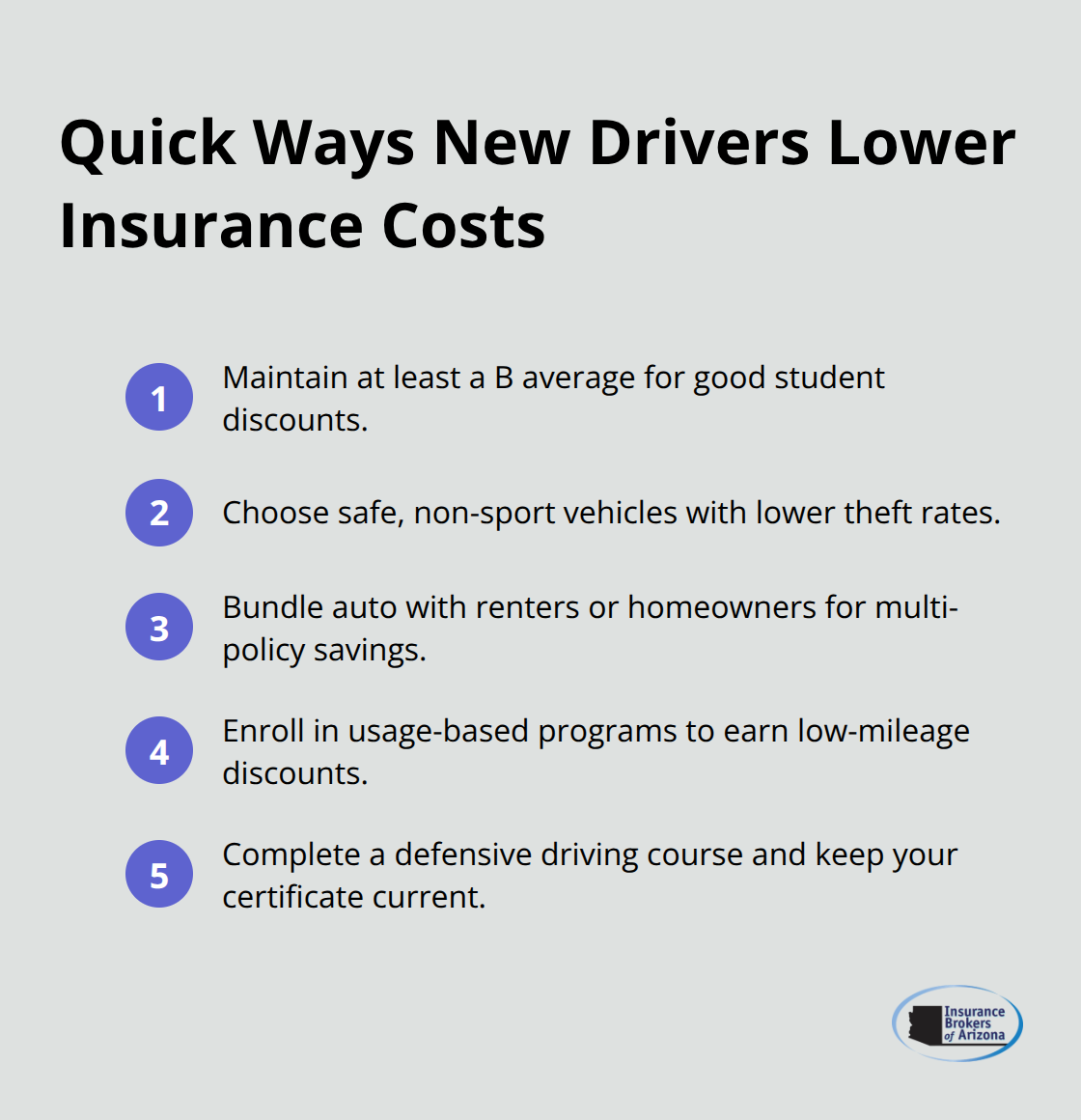

Good student discounts offer substantial savings that many new drivers overlook. Students who maintain a B average or 3.0 GPA qualify for discounts that range from 10-25% with most insurers. State Farm provides some of the largest good student discounts, which potentially save families $500-800 annually. Erie offers competitive rates for teen drivers with strong academic performance and often beats national averages by significant margins.

The discount typically applies until age 25, which makes academic achievement financially rewarding for years. Students must provide report cards or transcripts as proof, but this small effort yields major savings. Some insurers extend discounts to honor roll students or those in the top 20% of their class.

Vehicle Selection Makes or Breaks Your Budget

Your car choice dramatically impacts insurance costs more than most new drivers realize. Sports cars like Mustangs or Camaros can increase premiums by 60-80% compared to sedans. Luxury vehicles with high theft rates also carry expensive premiums. The Mazda MX-5 Miata and Subaru Outback average around $2,640-2,735 annually for insurance (significantly below sports car averages).

Older vehicles with strong safety ratings provide the sweet spot for new drivers. Cars over 5-7 years old typically cost less to insure while they still offer modern safety features. Avoid modified vehicles entirely, as customizations can increase premiums by hundreds of dollars annually.

Multi-Policy Bundling Creates Immediate Savings

Auto insurance combined with renters or homeowners policies generates automatic discounts of 15-25%. Most major insurers offer multi-policy discounts, which makes bundling one of the easiest ways to reduce costs. Renters insurance added for $150-200 annually while you save 20% on auto premiums creates net savings for most new drivers.

USAA provides exceptional bundling discounts for eligible members, while other insurers compete aggressively for bundled business. The savings compound when parents bundle teen drivers with existing home and auto policies (creating family-wide discounts that benefit everyone).

Even with these cost-cutting strategies, new drivers often make expensive mistakes that completely undermine their savings efforts.

Common Mistakes New Drivers Make with Auto Insurance

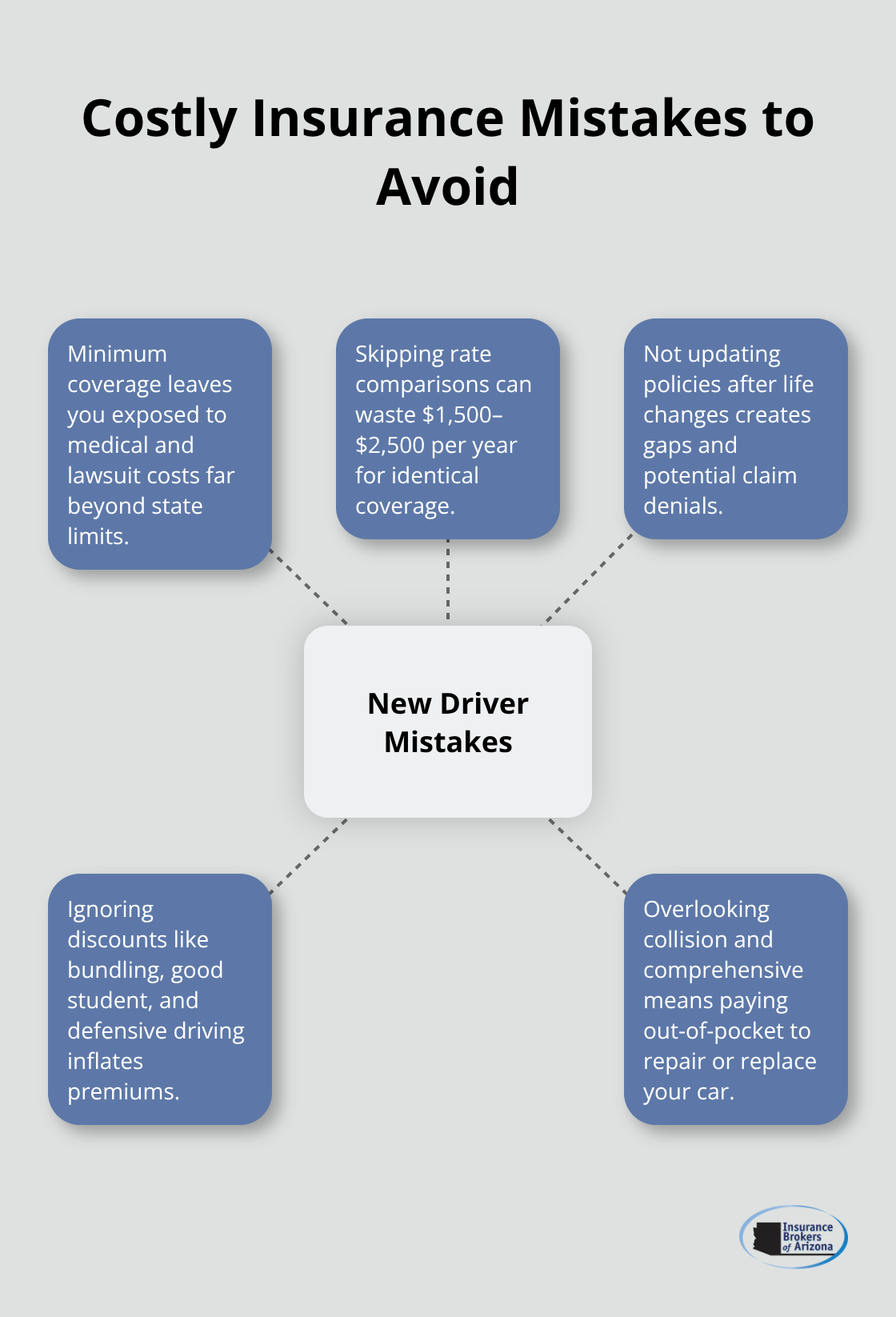

Minimum Coverage Creates Maximum Financial Risk

Arizona’s minimum liability limits of $25,000/$50,000/$15,000 provide dangerously inadequate protection that exposes new drivers to financial ruin. A single emergency room visit after an accident averages $35,000-50,000, which immediately exceeds state minimums. Medical costs from serious injuries routinely reach $200,000-500,000, which leaves drivers personally liable for amounts that could bankrupt them for decades.

Erie and USAA data shows that drivers with minimum coverage face lawsuit settlements that average $150,000 above their policy limits in moderate accidents. New drivers with minimum coverage also lack collision and comprehensive protection, which means they pay out-of-pocket for vehicle repairs or replacement. A totaled $15,000 vehicle becomes a complete loss without collision coverage.

Rate Comparison Failures Cost Thousands Annually

New drivers who accept their first insurance quote without comparison waste an average of $1,500-2,500 annually according to industry data. Premium differences between insurers can exceed 200% for identical coverage. State Farm might quote $4,200 while Erie offers $2,800 for the same new driver profile.

USAA provides the cheapest rates for eligible young adults but requires military connections that many families overlook. Geographic variations compound these differences dramatically. Phoenix drivers pay 30-40% more than Tucson residents with identical profiles (despite similar risk factors). Online comparison tools reveal these disparities instantly, yet most new drivers never use them.

Coverage Update Neglect Creates Claim Denials

New drivers who fail to adjust coverage after major life changes create coverage gaps that insurers exploit to deny claims. Students who take vehicles to out-of-state schools without notification may find themselves completely uninsured during accidents. Marriage, job changes, and vehicle purchases all trigger necessary coverage adjustments that many drivers ignore until claim time.

Usage-based insurance programs offer substantial discounts for low-mileage drivers, but students must actively enroll rather than assume automatic qualification. Defensive driving course completion reduces premiums by 10-15% with most carriers, but certificates expire and require renewal (typically every three years). These proactive updates separate financially protected drivers from those who face claim denials and premium penalties.

Final Thoughts

New drivers who approach auto insurance strategically save thousands annually while they secure proper protection. The data reveals that smart coverage selection, sensible vehicle choices, and discount optimization reduce premiums by 30-50% compared to uninformed decisions. Academic performance, defensive courses, and policy bundling create immediate savings that compound over time.

Professional guidance eliminates the costly mistakes that trap many new drivers in expensive policies. We at Insurance Brokers of Arizona® help clients navigate complex coverage options and secure competitive rates from multiple carriers. Our experience identifies discounts and coverage combinations that independent shoppers often miss.

Auto insurance as a new driver transforms from an overwhelming expense into manageable protection through proper preparation. Gather quotes from multiple insurers while you focus on adequate liability limits above state minimums (rather than accepting bare-bones coverage). Document your grades, research vehicle safety ratings, and complete defensive courses to maximize your savings potential.