Top Commercial Truck Insurance Questions Answered

Commercial truck insurance questions keep business owners awake at night. The wrong coverage can cost thousands in claims or regulatory fines.

We at Insurance Brokers of Arizona® see trucking companies make expensive mistakes daily. This guide answers the most pressing questions about protecting your fleet and business.

What Insurance Do You Actually Need for Your Truck?

Federal Requirements Set the Floor

The Federal Motor Carrier Safety Administration sets specific minimums based on cargo weight and type. Non-hazardous freight under 10,001 pounds requires $300,000 in liability coverage, while freight over 10,001 pounds jumps to $750,000. Hazardous materials transportation demands between $1 million and $5 million in coverage (depending on the specific materials transported). These federal minimums represent bare-bones protection that leaves most operators dangerously underinsured.

State requirements add another layer of complexity. Alabama requires only $7,500 for light freight, while California matches this figure, but most states set liability minimums at $1.5 million for hazmat operations.

Weight and Distance Drive Your Premium

Cargo weight directly impacts your insurance costs through increased liability exposure. Heavy equipment transport generates significantly higher premiums than fresh produce transport due to potential damage severity. Your radius affects rates more than most truckers realize. Local operations within 50 miles cost substantially less than cross-country routes because longer distances increase accident probability and claim frequency.

Interstate operations require additional forms like BMC-91, which add regulatory complexity and cost. Refrigerated goods need specialized coverage for spoilage protection, while oversize loads demand infrastructure damage liability coverage.

Current Market Rates Tell the Story

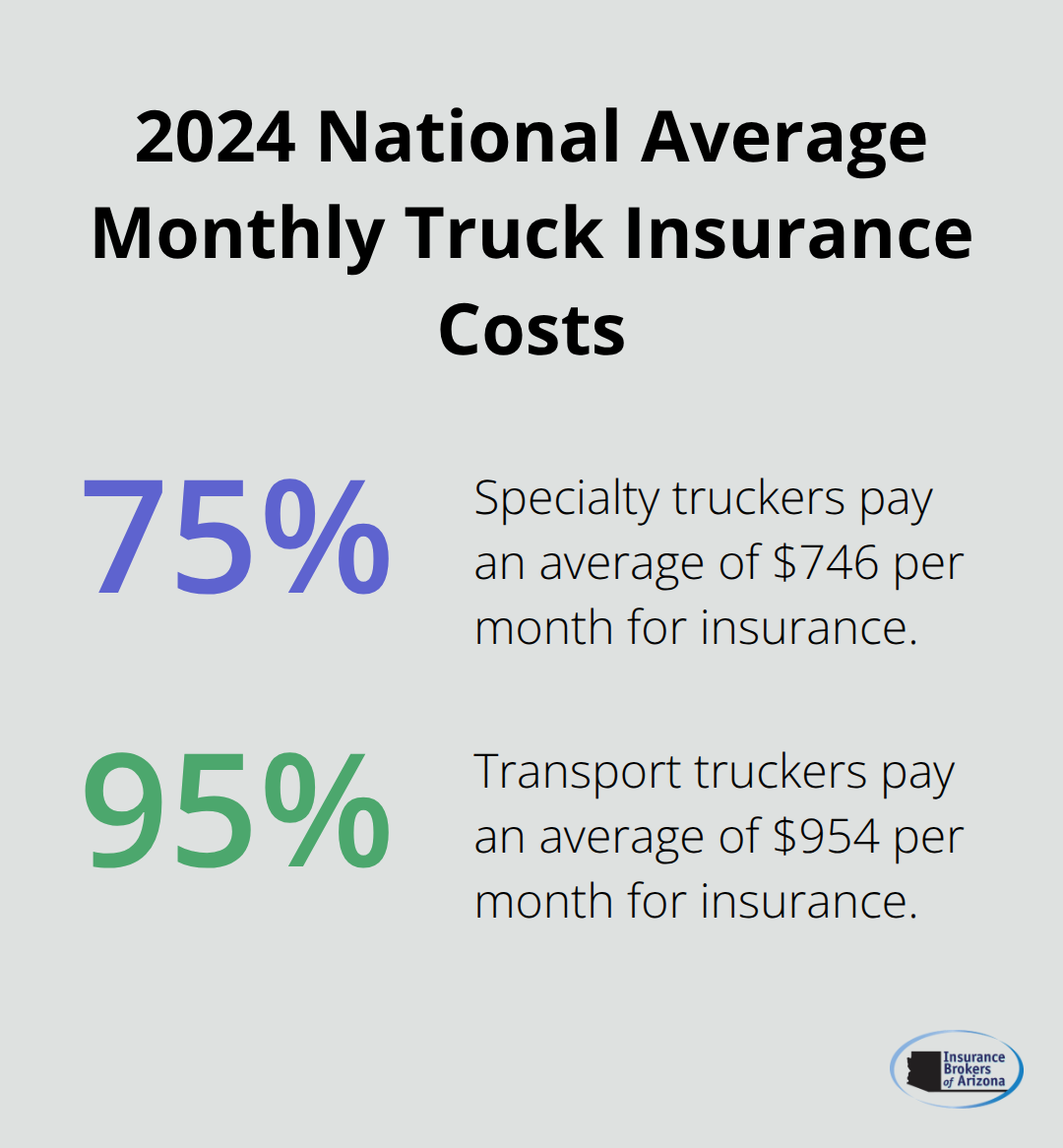

The national average monthly cost reaches $746 for specialty truckers and $954 for transport truckers according to 2024 data. Commercial auto insurance typically ranges from $1,200 to $2,400 per year, but this can vary significantly based on your specific operation. Smart operators match coverage types to actual operations rather than buy generic policies that waste money on unnecessary protection.

Your next challenge involves understanding exactly which factors insurance companies use to calculate these rates and how you can influence them to reduce your premiums.

What Drives Your Insurance Costs Up or Down

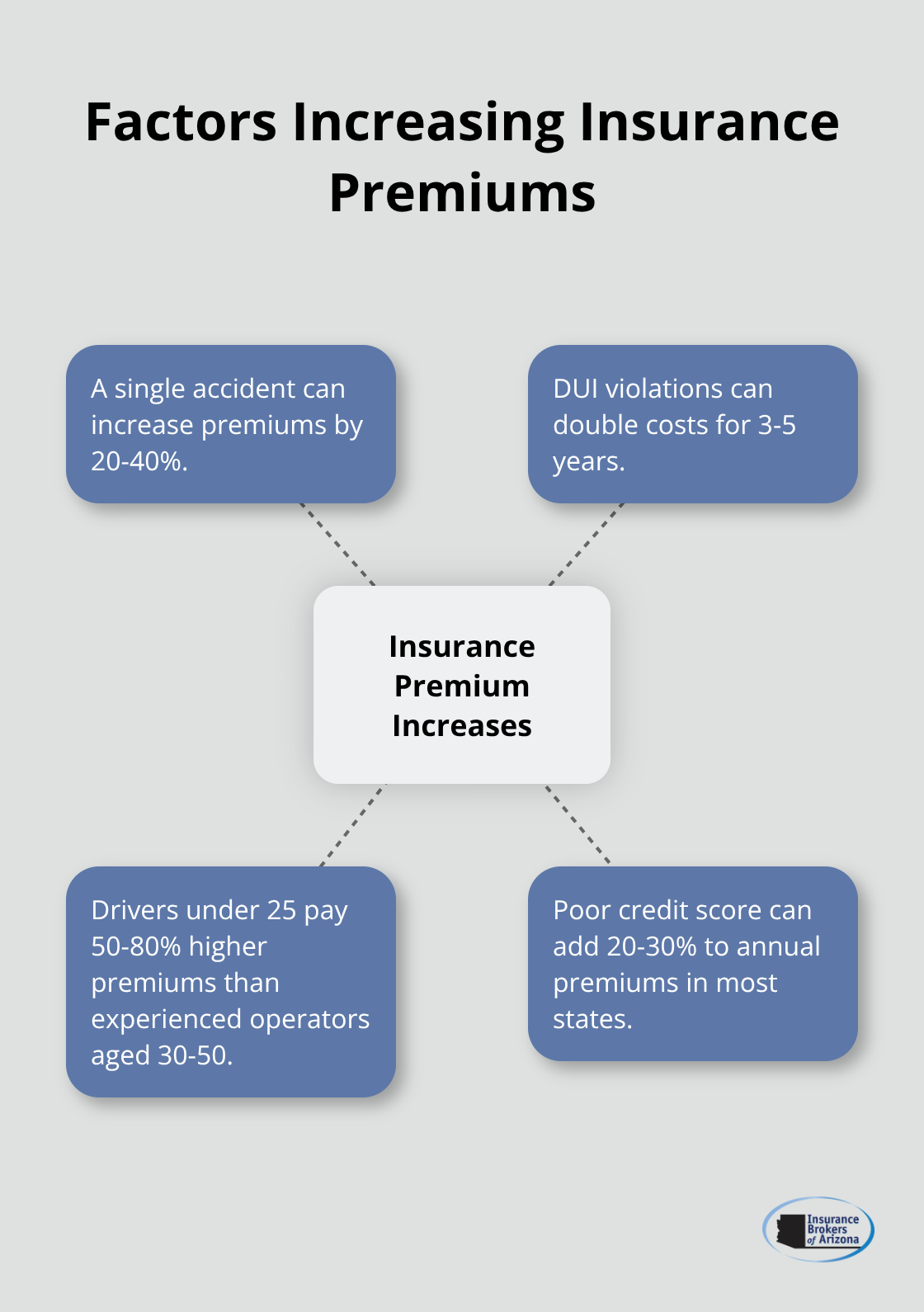

Insurance companies calculate your rates with hard data points that directly reflect your risk profile. Your record behind the wheel carries the heaviest weight in rate calculations. A single accident increases premiums by an average of 20-40%, while DUI violations can double your costs for three to five years. Age matters significantly too – drivers under 25 pay premiums that are 50-80% higher than experienced operators aged 30-50. Your credit score affects rates in most states, with poor credit adding 20-30% to annual premiums.

Fleet Size Creates Exponential Risk

Multiple truck operations multiply your exposure and premium costs. A single truck operation pays base rates, but a second vehicle increases total premiums by 70-80% rather than doubles them due to shared overhead costs. However, fleets of 10 or more trucks face different calculations entirely. Large fleet operators often secure better per-vehicle rates through volume discounts but face higher aggregate costs due to statistical probability of claims.

Vehicle Type and Cargo Influence Rates

Heavy equipment transport generates significantly higher premiums than fresh produce transport due to potential damage severity. Refrigerated trucks require specialized coverage for spoilage protection, which adds 15-25% to base premiums. Oversize load operations demand infrastructure damage liability coverage that can increase costs by 30-50%. Hazmat transport requires the most expensive coverage (ranging from $1-5 million depending on materials transported). The type of vehicle your business uses significantly affects insurance rates.

Proven Cost Reduction Strategies That Work

Smart Haul program participants save an average of $1,056 annually according to Progressive data. Dash cam installation reduces premiums by 10-15% with most carriers because they provide clear accident evidence and encourage safer behavior. Telematics devices that monitor speed, braking, and acceleration patterns can cut rates by 5-20% for consistently safe drivers.

Annual payment instead of monthly eliminates financing fees and often triggers paid-in-full discounts exceeding 13% of total premiums. Deductible increases from $500 to $2,500 reduce monthly costs by 15-25%, though this strategy requires adequate cash reserves for potential claims. Driver training programs certified by the National Safety Council qualify for additional discounts of 5-10% with major insurers. Understanding what drives commercial auto insurance costs helps you make informed decisions about coverage options.

These cost factors matter, but many truck owners still make expensive coverage mistakes that wipe out any premium savings they achieve.

What Coverage Mistakes Cost You Money

Liability Limits That Leave You Exposed

Truck owners consistently underestimate their liability exposure and create financial disasters that destroy businesses overnight. Federal minimums represent bare-bones protection that leaves operators dangerously exposed to lawsuits that exceed their coverage limits. A single severe accident that involves multiple vehicles can generate claims of $2-5 million, yet many truckers carry only the $750,000 federal minimum. Progressive reports that 67% of commercial truck operators carry inadequate liability limits for their actual risk exposure. Owner-operators who haul high-value cargo face the greatest risk because they lack the corporate protection larger fleets enjoy.

Cargo Insurance Gaps Create Massive Exposures

Cargo insurance represents the most overlooked coverage among independent truckers, with only 43% who carry adequate protection according to American Trucking Association data. Electronics shipments require coverage of $100,000-250,000 per load, while pharmaceutical cargo demands $500,000-1 million in protection. Refrigerated goods need specialized spoilage coverage that standard cargo policies exclude. Temperature excursions during a single cross-country trip can destroy $50,000-100,000 in pharmaceutical products. Freight brokers increasingly require proof of cargo coverage before they assign loads, which makes this protection essential for profitable contracts.

Deductible Decisions That Backfire

High deductibles seem attractive for premium savings, but they create cash flow problems during claims. Truckers who choose $5,000-10,000 deductibles save 20-30% on premiums but struggle to pay repair costs after accidents. Physical damage claims average $15,000-25,000 for major truck repairs, making moderate deductibles of $1,000-2,500 more practical. Fleet operators with strong cash reserves can handle higher deductibles, but single-truck operations need lower amounts to maintain operations during repairs. The first mistake involves purchasing minimal liability coverage to save money upfront, which backfires when lawsuits exceed policy limits.

Final Thoughts

Commercial truck insurance questions become simple when you understand the core requirements and cost factors. Federal minimums provide inadequate protection for most operations, while proper liability limits prevent business-destroying lawsuits. Cargo insurance protects your revenue stream, and reasonable deductibles maintain cash flow during claims.

Professional guidance eliminates expensive mistakes that cost thousands in premiums and claims. We at Insurance Brokers of Arizona® work with multiple carriers to find competitive rates that match your specific operations. Our expertise helps trucking companies avoid coverage gaps while securing the best possible rates for their risk profile.

The right coverage starts with an honest assessment of your operations, cargo types, and risk exposure (including both federal and state requirements). Insurance Brokers of Arizona® provides personalized solutions that protect your business without waste on unnecessary coverage. Contact us today to review your current policy and identify opportunities for better protection at competitive rates.