How Much Does Small Business Liability Insurance Cost?

Small business general liability insurance cost varies dramatically based on your industry, company size, and coverage needs. Most businesses pay between $400 and $1,500 annually, but high-risk industries can face premiums exceeding $3,000.

We at Insurance Brokers of Arizona® help business owners navigate these costs daily. Understanding the key factors that drive pricing helps you budget effectively and find the right protection for your company.

What Drives Your Liability Insurance Costs

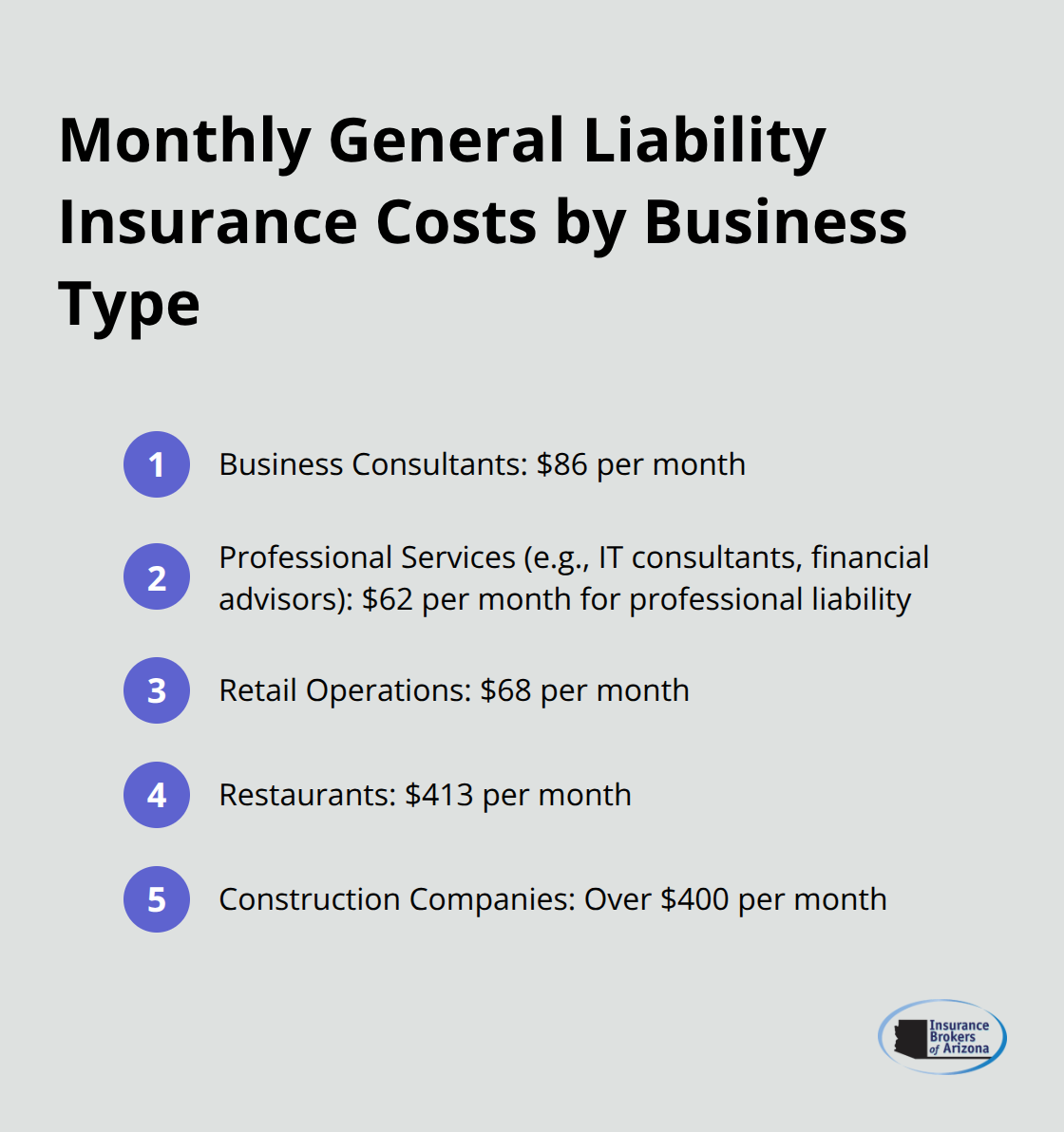

Your liability insurance premium depends on three primary factors that insurers evaluate when they calculate risk. Construction companies face the highest costs and pay an average of $413 monthly according to The Hartford, while business consultants pay just $86 monthly. This massive difference reflects the stark reality that insurers price policies based on actual claim data and loss history within each industry.

Industry Risk Classification Sets Base Rates

Insurers use specific classification codes to categorize your business and assign risk levels. Restaurants average $413 monthly due to slip-and-fall incidents and food poisoning claims, while IT consultants pay significantly less because they rarely face bodily injury lawsuits. Manufacturing businesses pay premium rates because machinery accidents and product liability claims cost insurers an average of $75,000 per business liability claim. Your industry classification locks in your base rate before other factors come into play.

Revenue and Employee Count Drive Premium Calculations

Businesses that earn over $1 million annually pay substantially more than smaller operations because higher revenue correlates with greater liability exposure. Companies with larger payrolls face increased premiums since more employees mean higher accident probability. Workers’ compensation costs average $86 monthly for businesses with under $300,000 in payroll but escalate rapidly as employee counts rise. Insurers view revenue and staff size as direct indicators of potential claim severity and frequency.

Coverage Limits Create Your Premium Range

Most Insureon customers select $1 million per occurrence and $2 million aggregate limits (which represents the industry standard for adequate protection). Higher limits like $2 million per occurrence can double your premium, while lower limits save money but create dangerous gaps in coverage. The average $500 deductible that most businesses choose balances affordable premiums with manageable out-of-pocket costs when claims occur.

These three factors work together to create your final premium quote, but smart business owners can take specific steps to reduce these costs without sacrificing protection.

What Do Different Business Types Actually Pay?

Professional service businesses like consultants and accountants pay the lowest liability insurance premiums in the market. Business consultants average just $86 monthly according to The Hartford data, while professional liability insurance costs around $62 monthly for most service providers. These businesses benefit from low physical risk exposure since they work primarily with information rather than equipment or products that could cause bodily injury.

Professional Services Enjoy the Lowest Rates

IT consultants and financial advisors typically fall into this favorable category because their work environments pose minimal slip-and-fall risks. Accounting firms and legal practices also qualify for these reduced rates since they rarely handle hazardous materials or operate dangerous equipment. Professional liability coverage protects these businesses from errors and omissions claims (which average $61 monthly across all professional services).

Retail Operations Face Moderate Premium Costs

Retail businesses occupy the middle ground with general liability premiums that average $68 monthly. Slip-and-fall incidents in retail stores generate average claims between $30,000 and $50,000, which explains why even low-risk retail operations pay substantially more than office-based businesses. Clothing stores, electronics retailers, and similar businesses face consistent customer foot traffic that creates ongoing liability exposure.

Food Service Commands Higher Premium Rates

Restaurants pay significantly more at $413 monthly due to constant customer interaction and food safety risks. Food service establishments face elevated premiums because food poisoning lawsuits and kitchen accidents create severe liability exposure that insurers price aggressively. Fast-food chains and fine restaurants both face similar rate structures since both handle food preparation and serve the public daily.

Construction and Manufacturing Pay Premium Rates

Manufacturing businesses pay the steepest liability insurance costs because machinery accidents and product defects generate claims that average nearly $75,000 per incident. Construction companies face similar premium pressure with monthly costs often exceeding $400 due to workplace injury frequency and property damage potential. These industries cannot escape their high-risk classification regardless of safety measures because historical claim data shows consistent loss patterns.

Smart business owners in all categories can take specific steps to reduce these baseline costs through strategic risk management and policy selection.

How Can You Lower Your Premium Costs

Smart business owners reduce liability insurance premiums through three proven strategies that directly impact their rates. Safety programs cut premiums by 5-15% because insurers reward businesses that actively prevent claims through employee training and hazard reduction protocols.

Implement Comprehensive Safety Programs

Manufacturing companies that implement comprehensive safety training see the biggest premium reductions since their baseline rates start highest. Construction firms that document safety meetings and maintain clean job sites qualify for preferred rates that can save thousands annually. Restaurant owners who train staff on proper lifting techniques and floor maintenance reduce slip-and-fall incidents that cost insurers between $30,000 and $50,000 per claim.

Bundle Policies for Immediate Savings

Bundled general liability with commercial property insurance creates a Business Owner’s Policy that averages $57 monthly compared to separate policies. The Hartford data shows bundled coverage costs significantly less than individual policies while it provides comprehensive protection. Businesses that add cyber insurance to their bundle save additional money since insurers prefer customers who buy multiple products. Commercial umbrella coverage costs just $75 monthly when bundled but provides an extra $1 million in protection above your base limits.

Work with Experienced Brokers for Better Rates

Independent insurance brokers access wholesale markets that direct-buy customers never see, often finding rates 15-25% below retail prices. Brokers compare quotes from multiple insurers simultaneously while direct customers must shop each company individually. Experienced brokers know which carriers offer the best rates for specific industries and can place high-risk businesses with specialty insurers that standard companies reject. Professional brokers also negotiate payment terms and help structure policies to minimize gaps while they keep costs reasonable for businesses (with partnerships spanning over 40 carriers providing competitive options).

Final Thoughts

Small business general liability insurance cost varies dramatically based on your industry risk level, company size, and coverage limits. Professional services pay as little as $86 monthly while restaurants and construction companies face premiums that exceed $400 monthly due to higher claim frequencies. Manufacturing businesses pay premium rates because machinery accidents average $75,000 per claim, while retail operations fall in the middle range at $68 monthly.

Adequate coverage protects your business from financial devastation when lawsuits occur. Even frivolous claims generate substantial legal defense costs that can bankrupt uninsured businesses. The industry standard $1 million per occurrence and $2 million aggregate limits provide solid protection for most operations (with 91% of businesses choosing these limits according to Insureon data).

We at Insurance Brokers of Arizona® help Arizona businesses find competitive rates through our partnerships with reputable carriers. Our team compares quotes from multiple insurers to match your specific risk profile with the best available rates. Document your business operations, employee count, and revenue to get accurate quotes that reflect your actual risk exposure.