Is Commercial Auto Insurance More Expensive than a Personal Policy?

At Insurance Brokers of Arizona®, we often hear this question from business owners: Is commercial auto insurance more expensive than personal insurance?

The answer isn’t always straightforward. It depends on various factors unique to your business and vehicles.

In this post, we’ll break down the key differences between commercial and personal auto insurance, explore the factors that influence costs, and help you understand which option might be best for your situation.

What Is Commercial Auto Insurance?

Commercial auto insurance is a specialized policy that protects businesses that use vehicles for work-related purposes. This type of coverage is essential for many companies, from small local businesses to large corporations.

Vehicles and Businesses Covered

Commercial auto insurance covers a wide range of vehicles used for business purposes. This includes:

- Company cars

- Trucks

- Vans

- Specialized vehicles (e.g., food trucks or construction equipment)

The policy applies to businesses across various sectors, such as:

- Delivery services

- Construction

- Landscaping

- Professional services (where employees use vehicles for client visits)

Key Differences from Personal Auto Insurance

The main distinction between commercial and personal auto insurance is the scope and extent of coverage. Commercial policies often have higher liability limits to protect businesses from potentially costly lawsuits. For instance, a typical personal policy might offer liability coverage up to $300,000, while commercial policies can provide coverage in the millions.

Additional Coverage Options

Commercial auto insurance offers unique coverage options that aren’t typically available in personal policies. These include:

- Non-owned auto coverage: This protects your business if an employee uses their personal vehicle for work purposes.

- Hired auto coverage: This covers vehicles your business rents or leases for short-term use.

- Loading and unloading coverage: This is particularly useful for businesses that transport goods.

Tailoring Policies to Business Needs

Every business is unique, and cookie-cutter solutions often fall short. That’s why it’s important to work with an insurance provider who takes the time to understand your operations and recommend coverage that truly protects your business assets.

As we move forward, let’s explore the factors that influence the cost of commercial auto insurance and how they compare to personal policies.

What Drives Commercial Auto Insurance Costs?

Commercial auto insurance costs depend on several key factors. Let’s explore the main drivers of these costs.

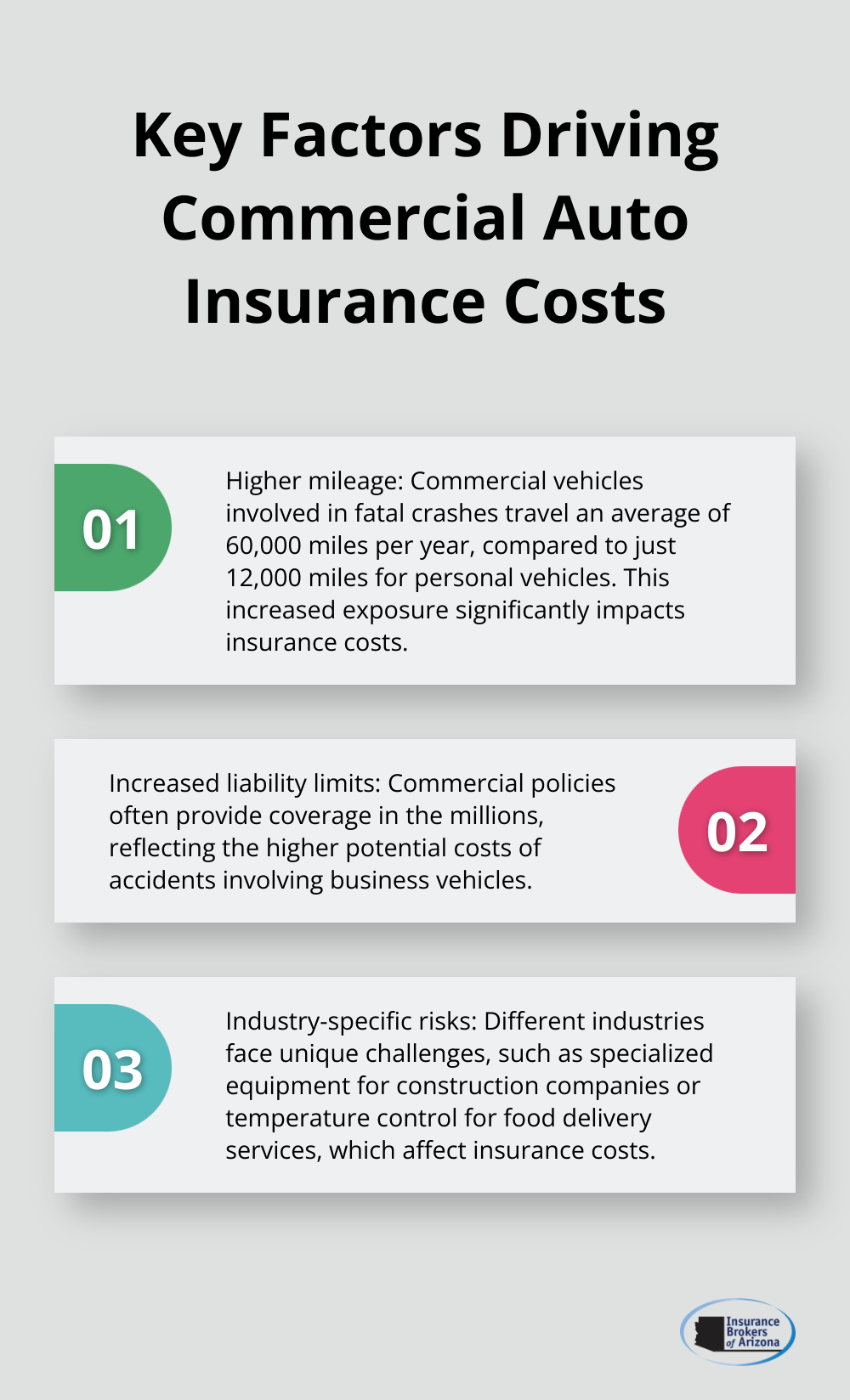

Higher Liability Limits and Risk Exposure

Commercial auto policies typically offer higher liability limits than personal policies. While a personal policy might cap liability coverage at $300,000, commercial policies often provide coverage in the millions. This increased coverage protects businesses from potentially devastating lawsuits.

A delivery truck involved in a multi-car accident, for instance, could result in significant property damage and medical expenses. The higher liability limits of a commercial policy shield the business from financial ruin in such scenarios.

Vehicle Type and Usage Patterns

The type of vehicle and its use significantly impact insurance costs. Larger vehicles (like trucks or vans) often cost more to insure due to their potential for causing more damage in accidents. Vehicles that travel long distances or in high-traffic areas face increased risk and thus higher premiums.

A Federal Motor Carrier Safety Administration study found that commercial vehicles involved in fatal crashes traveled an average of 60,000 miles per year, compared to 12,000 miles for personal vehicles. This increased exposure directly affects insurance costs.

Driver Qualifications and History

The qualifications and driving history of employees operating company vehicles significantly affect insurance rates. Businesses with experienced drivers with clean records often enjoy lower premiums. Those employing younger or less experienced drivers may face higher costs.

Implementing a comprehensive driver training program and regular safety checks can potentially lower insurance costs and improve overall fleet safety.

Business Location and Operating Radius

A business’s location and the distance its vehicles travel also impact insurance costs. Urban areas with higher traffic density and accident rates typically result in higher premiums compared to rural locations. Businesses that operate across state lines or cover large territories may face increased costs due to expanded risk exposure.

An Insurance Information Institute report showed that insurance claim frequency is about 40% higher in urban areas compared to rural regions, directly affecting commercial auto insurance rates.

Industry-Specific Risks

Different industries face unique risks that influence their commercial auto insurance costs. For example:

- Construction companies may need coverage for specialized equipment.

- Food delivery services might require temperature control failure coverage.

- Trucking companies often need higher cargo coverage limits.

Understanding these industry-specific factors helps businesses work with their insurance providers to find ways to mitigate risks and potentially reduce their insurance costs.

Now that we’ve explored the factors influencing commercial auto insurance costs, let’s compare these costs to personal auto insurance policies to give you a clearer picture of what to expect.

How Commercial and Personal Auto Insurance Costs Compare

The Price Gap: Commercial vs. Personal Auto Insurance

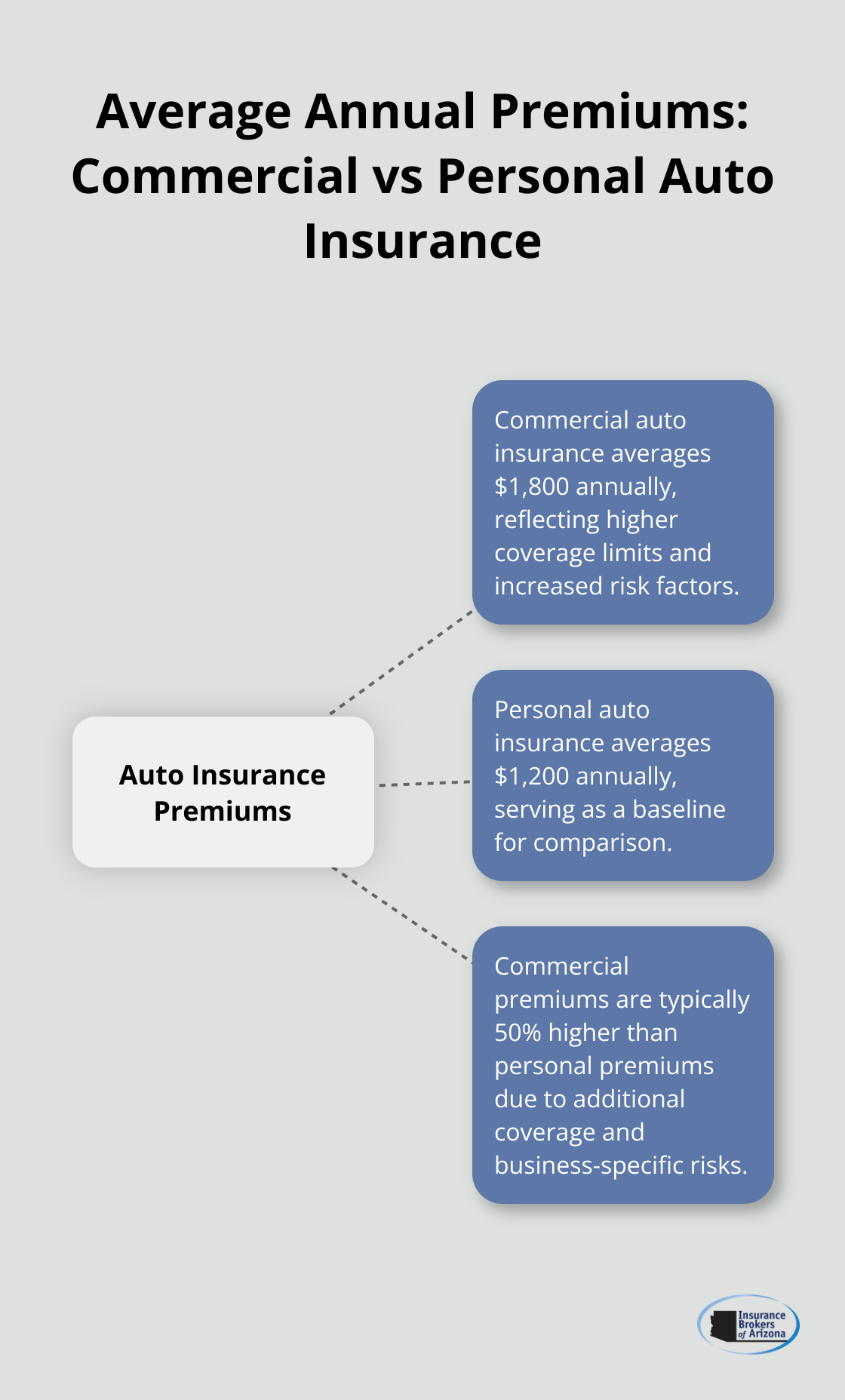

Commercial auto insurance typically costs more than personal auto insurance. A 2023 report by the National Association of Insurance Commissioners (NAIC) reveals that the average annual premium for commercial auto insurance is about $1,800, while personal auto insurance averages around $1,200. This 50% difference reflects the additional coverage and risk factors associated with commercial policies.

However, these averages can fluctuate significantly based on individual circumstances. A small business owner who uses a single vehicle for occasional client visits might pay only slightly more than a personal policy. In contrast, a trucking company with a fleet of vehicles could face premiums in the tens of thousands.

Scenarios Where Commercial Insurance Proves More Cost-Effective

Despite the generally higher costs, commercial auto insurance can be more economical in certain situations:

- High-value personal vehicles: A commercial policy might offer better coverage at a lower cost than a personal policy with high limits for expensive cars used for business purposes.

- Multiple vehicles: Commercial fleet policies often provide better rates per vehicle compared to insuring each separately under personal policies for businesses with several vehicles.

- Specialized coverage needs: Some industries require specific coverages that are more cost-effective under a commercial policy. For example, a food truck business might find it cheaper to bundle vehicle and business property coverage under a commercial policy.

Long-Term Cost Considerations and Potential Savings

The upfront costs of commercial auto insurance may be higher, but the long-term financial protection it offers can lead to significant savings. A 2022 study by the Insurance Research Council found that the average commercial auto liability claim was $18,000 (well above most personal policy limits).

To maximize savings on commercial auto insurance:

- Implement a robust safety program: Businesses with strong safety records often qualify for lower premiums.

- Choose appropriate deductibles: Higher deductibles can lower premiums, but ensure they’re manageable for your business.

- Conduct regular policy reviews: As your business evolves, your insurance needs may change. Annual reviews can help ensure you’re not over or under-insured.

- Bundle policies: Combining commercial auto with other business insurance policies often results in discounts.

Understanding these cost factors and working with experienced insurance professionals helps businesses find the right balance between comprehensive coverage and affordable premiums.

Final Thoughts

Commercial auto insurance often costs more than personal insurance due to its broader coverage and higher liability limits. The price difference reflects the increased risks businesses face when using vehicles for work purposes. However, in some cases, commercial policies prove more cost-effective, especially for high-value vehicles or multiple-car fleets.

We at Insurance Brokers of Arizona® understand the complexities of commercial auto insurance. Our team works with over 40 reputable carriers to find the best coverage options for your business needs. We strive to balance comprehensive protection with affordable premiums (tailored to your specific circumstances).

Don’t leave your business vulnerable to potential financial losses. Partner with Insurance Brokers of Arizona® to find the right commercial auto insurance solution. Our personalized approach ensures you get the coverage that best protects your business assets while addressing the question: Is commercial auto insurance more expensive than personal insurance?