Liability Auto Insurance Arizona: What It Covers

Liability auto insurance in Arizona is mandatory, yet many drivers don’t fully understand what it actually covers. At Insurance Brokers of Arizona®, we’ve seen firsthand how confusion about coverage limits leads to serious financial exposure.

This guide breaks down exactly what your liability protection includes and why getting it right matters for your wallet and your future.

What Liability Coverage Actually Protects

Liability auto insurance in Arizona covers two distinct types of damage you cause to others: bodily injury and property damage. When you’re at fault in an accident, your liability coverage pays medical bills, lost wages, and legal fees for injured parties, up to your policy limits. It also covers damage you cause to someone else’s vehicle, fence, building, or other property. Arizona law requires a minimum of $25,000 per person for bodily injury, $50,000 per accident when multiple people are injured, and $15,000 for property damage, according to the Arizona Department of Insurance and Financial Institutions. These minimums exist because Arizona operates under a fault-based system, meaning the at-fault driver bears financial responsibility for damages. Driving without liability coverage is illegal and can result in license suspension, registration suspension, and an SR-22 requirement that stays on your record for three years.

Bodily Injury Liability Covers Real Medical Costs

Bodily injury liability pays for injuries or death you cause to other people. This includes emergency room visits, surgery, physical therapy, lost wages while someone recovers, and even funeral expenses if someone dies from your accident. If you hit another vehicle and the driver needs spinal fusion surgery costing $150,000, your bodily injury liability covers it up to your limit. The per-person limit applies to each injured individual, while the per-accident limit caps total payouts regardless of how many people get hurt. Many Arizona drivers choose limits higher than the state minimum because $25,000 barely covers a serious injury anymore. If your limit is exhausted and damages exceed it, the injured party can pursue a lawsuit against your personal assets, which is why adequate limits matter significantly more than the minimum requirement.

Property Damage Liability Stops at Other People’s Stuff

Property damage liability covers damage to vehicles, property, and belongings you damage in an accident, but it stops short of your own vehicle. If you rear-end someone at a red light and cause $8,000 in damage to their car, your property damage liability pays for repairs up to your limit. This coverage also handles damage to mailboxes, fences, storefronts, or parked vehicles you hit. Arizona’s $15,000 minimum property damage limit covers most single-vehicle damage claims, but multiple vehicles or expensive vehicles can exceed this quickly. Importantly, your own vehicle damage requires separate collision or comprehensive coverage, not liability. This distinction confuses many drivers who assume liability protects their own car, then face unexpected repair bills when their vehicle is damaged in an accident they caused.

Why Your Coverage Limits Matter More Than You Think

The gap between Arizona’s minimum limits and what you actually need can cost you thousands. A serious accident involving multiple injuries or expensive property can quickly exhaust the state minimums, leaving you personally liable for the remainder. Many drivers underestimate how fast medical bills accumulate-a single hospitalization with follow-up care often exceeds $50,000. Your assets (home, savings, future wages) become vulnerable if a judgment against you surpasses your policy limits. Choosing higher limits than the minimum protects your financial future and provides peace of mind that one bad accident won’t destroy your life.

What Coverage Limits Actually Cost You

Arizona’s $25,000 per person and $50,000 per accident bodily injury minimums sound reasonable until you face a real injury claim. A single hospitalization with surgery and follow-up care easily exceeds $100,000 in today’s healthcare system. The National Highway Traffic Safety Administration reported that the average cost of a serious injury crash involving hospitalization runs between $80,000 and $250,000 depending on severity. If you hit someone and cause injuries that cost $120,000 to treat, your $25,000 limit covers only 21% of the actual damages. The injured party’s attorney will pursue the remaining $95,000 directly from your personal assets-your home, bank account, and future wages become fair game. Property damage limits of $15,000 seem adequate until you hit a newer luxury vehicle. Repairing a 2024 luxury sedan can easily run $25,000 to $40,000 for frame damage and component replacement. You become personally responsible for any amount exceeding your limit, and that bill arrives fast.

Why Higher Limits Protect Your Real Assets

Minimum limits of $100,000 per person and $300,000 per accident for bodily injury, with $100,000 for property damage, offer substantially better protection than state minimums. This approach costs roughly 20 to 30% more than state minimums but protects your actual wealth. The difference between a $50,000 limit and a $100,000 limit typically adds only $15 to $25 monthly to your premium. If you own a home or have savings, that difference is worth every dollar. A judgment against you doesn’t disappear after a few years-Arizona allows creditors to pursue wage garnishment and asset seizure for up to six years. Choosing limits based solely on state minimums treats your financial security as an afterthought. Consider your net worth, income level, and what you’d lose in a lawsuit. Someone with a $300,000 home and stable employment needs substantially more protection than someone renting an apartment.

Matching Limits to Your Actual Risk Profile

Your location in Arizona significantly impacts your accident risk and therefore your coverage needs. Phoenix drivers face higher traffic density and accident rates compared to rural areas, meaning higher limits make stronger financial sense. Your vehicle type also matters-driving a large truck or SUV that causes more damage in collisions argues for higher property damage limits. Drivers with teenagers or multiple household members using the vehicle should increase limits because more drivers mean more accident exposure. If you have assets to protect, adequate limits function as insurance for your insurance. The cost difference between adequate limits and inadequate ones becomes irrelevant after a major accident leaves you financially exposed. One serious crash can wipe out years of financial progress, making the premium increase a bargain investment in your future stability.

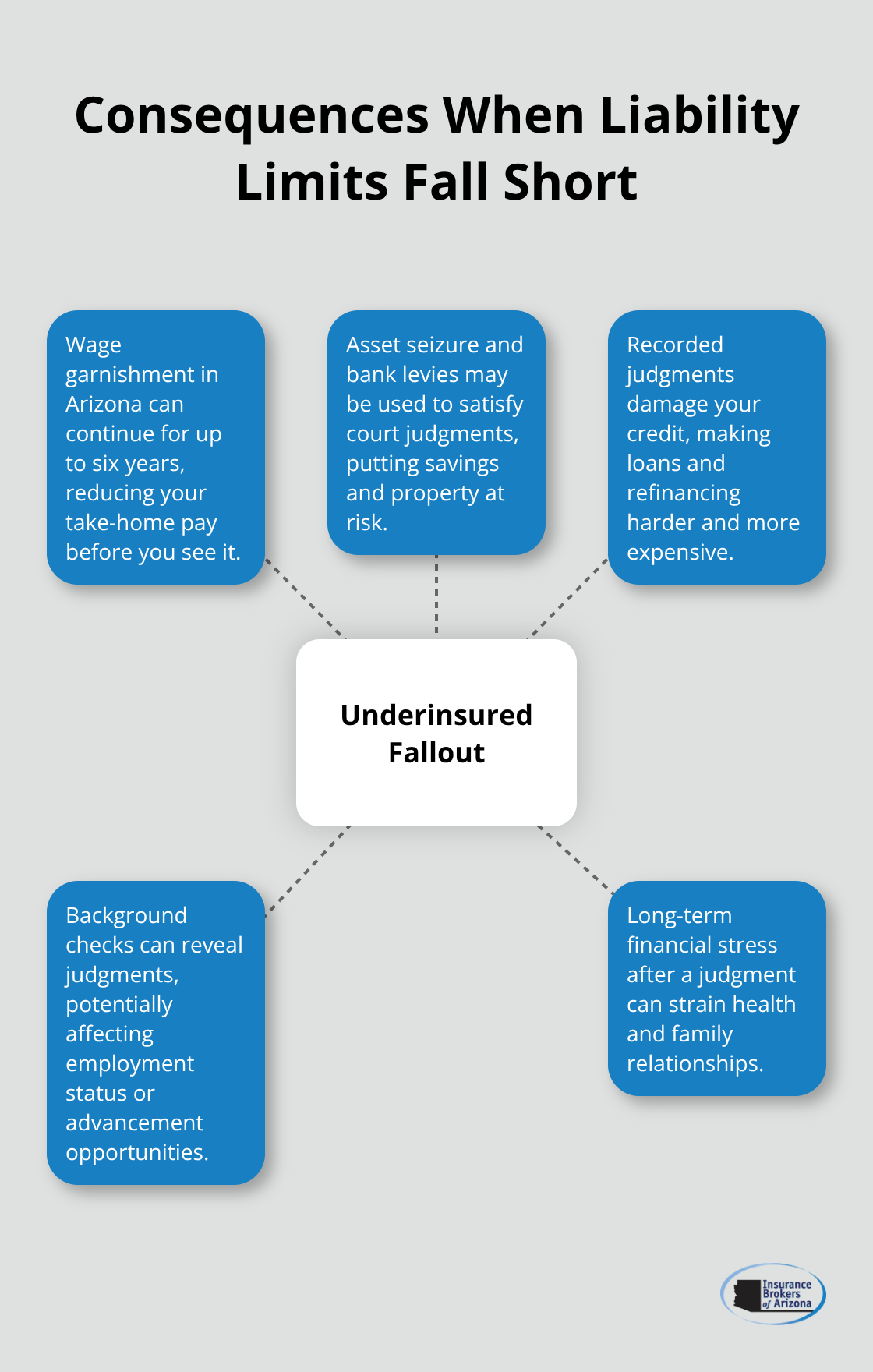

What Happens When Your Limits Fall Short

Underinsured drivers face devastating consequences that extend far beyond the accident itself. A lawsuit judgment can attach to your wages, bank accounts, and property for years, creating financial hardship long after the crash.

Courts in Arizona can order wage garnishment that reduces your paycheck before you ever see it. Your credit score suffers when judgments appear on your record, making it harder to borrow money or refinance existing debt. Some employers conduct background checks that reveal judgments, potentially affecting your employment status or advancement opportunities. The stress of financial liability often exceeds the stress of the accident itself, affecting your health and family relationships. Adequate coverage prevents this cascade of problems before they start.

When Liability Insurance Actually Pays Out

At-Fault Accidents Trigger Immediate Coverage

At-fault accidents activate liability coverage immediately, but understanding exactly what gets paid separates smart drivers from those facing unexpected bills. When you hit another vehicle and the other driver files a claim, your liability insurance covers their medical treatment, vehicle repairs, lost income while they recover, and legal costs if they hire an attorney. The National Highway Traffic Safety Administration reports that emergency room visits for crash injuries average $3,500 to $15,000 depending on severity, and that’s before imaging, surgery, or hospitalization. If the injured driver needs an MRI ($2,000 to $4,000), physical therapy ($150 per session for 20+ sessions), or time off work at $60,000 annually, your bodily injury liability covers all of it up to your policy limit.

Property Damage Claims Move Faster But Still Surprise You

Property damage claims move faster than injury claims but can still exceed expectations. A rear-end collision into a 2024 luxury sedan easily generates $8,000 to $15,000 in repair costs just for frame alignment and bumper replacement, and your $15,000 property damage minimum covers the full amount but leaves zero margin if a second vehicle is involved. Multiple vehicles compound the problem quickly. A three-car pileup where you’re at fault could generate $12,000 in damage to car one, $18,000 to car two, and $9,000 to car three, totaling $39,000 against your $15,000 property damage limit, leaving you personally responsible for $24,000.

Multiple Injuries Exhaust Limits Fast

The harsh reality emerges when multiple injuries or expensive property damage exhausts your limits. If you cause an accident with three injured passengers where medical bills total $95,000 and your limit is $50,000 per accident, you personally owe the remaining $45,000. Arizona law allows creditors to garnish your wages and seize assets for up to six years to satisfy that judgment, meaning your paycheck gets reduced before you see it and your bank account faces levies without warning. A construction worker earning $65,000 annually could lose $500 to $800 monthly in garnishments, disrupting their ability to pay rent or mortgage.

Your Personal Assets Face Direct Attack

Underinsured drivers face devastating consequences that extend far beyond the accident itself. A lawsuit judgment attaches to your wages, bank accounts, and property for years, creating financial hardship long after the crash. Courts in Arizona can order wage garnishment that reduces your paycheck before you ever see it. Your credit score suffers when judgments appear on your record, making it harder to borrow money or refinance existing debt. Some employers conduct background checks that reveal judgments, potentially affecting your employment status or advancement opportunities. The stress of financial liability often exceeds the stress of the accident itself, affecting your health and family relationships.

Higher Limits Protect What You’ve Built

Adequate coverage prevents this cascade of problems before they start. Financial experts recommend liability limits of at least $100,000 per person and $300,000 per accident to protect against these scenarios. One serious crash can wipe out years of financial progress, making the premium increase a bargain investment in your future stability. Review your coverage limits annually and adjust them based on your current assets and income level, because the cost of higher limits pales compared to the cost of underinsurance.

Final Thoughts

Liability auto insurance in Arizona protects your financial future far more than it protects your vehicle. The state minimums of $25,000 per person and $50,000 per accident for bodily injury, combined with $15,000 for property damage, meet legal requirements but leave you dangerously exposed to personal liability. Real accidents generate real costs that quickly exceed these minimums, and when they do, your wages, home, and savings become targets for collection.

The gap between minimum coverage and adequate protection costs surprisingly little. Increasing your limits to $100,000 per person and $300,000 per accident typically adds only $15 to $25 monthly to your premium, yet it shields your actual assets from judgment. That modest increase becomes the smartest financial decision you make if you ever cause a serious accident, which is why we recommend reviewing your liability auto insurance Arizona coverage today.

Your coverage needs depend on what you own and what you earn. Someone with a home, retirement savings, or stable employment faces far greater risk from underinsurance than someone with minimal assets. Contact us at Insurance Brokers of Arizona® to discuss your specific situation and receive a personalized quote that protects what you’ve built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.