How to Get Auto Insurance Without Owning a Car

Getting auto insurance no car might sound impossible, but several coverage options exist for people who don’t own vehicles. Whether you frequently borrow cars, rent vehicles, or use car-sharing services, you still need protection.

We at Insurance Brokers of Arizona® help clients navigate these unique insurance situations daily. The right coverage protects you from liability and financial risk, even without vehicle ownership.

What Non-Owner Car Insurance Actually Covers

Non-owner car insurance provides liability coverage for bodily injury and property damage when you drive vehicles you don’t own. This coverage typically ranges from $25,000 to $100,000 per person for bodily injuries, with property damage limits that start at $25,000. The Insurance Information Institute reports that these policies cost between $200 to $500 annually, which makes them 40-60% cheaper than standard auto insurance policies.

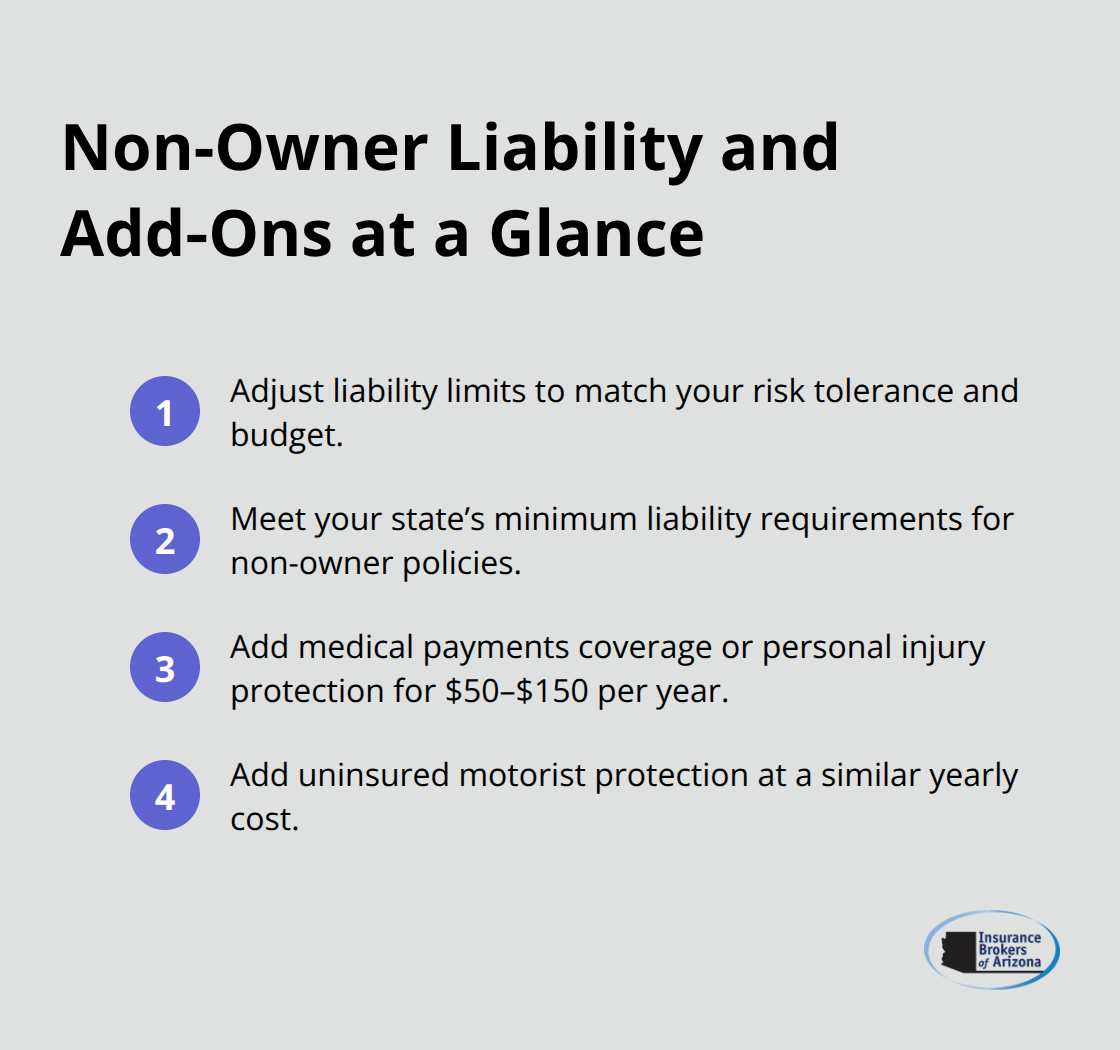

Coverage Limits and Protection Scope

Most insurers offer flexible liability limits that you can adjust based on your risk tolerance and budget. State minimum requirements apply to non-owner policies just like traditional coverage (meaning you must meet your state’s mandatory liability thresholds). Medical payments coverage and personal injury protection add $50-150 extra per year to your premium, while uninsured motorist protection costs roughly the same amount.

What This Insurance Won’t Cover

Non-owner policies exclude physical damage to the vehicle you drive and your own medical expenses after an accident. The coverage acts as secondary protection when you borrow cars, which means the vehicle owner’s insurance pays first. If their limits fall short, your non-owner policy covers the remaining costs. Comprehensive and collision coverage remain unavailable with these policies, regardless of how much you’re willing to pay.

Prime Candidates for Non-Owner Coverage

Frequent car borrowers, regular rental car users, and car-sharing service members gain the most value from non-owner policies. People who need to file SR-22 forms after license suspensions can maintain coverage without owning vehicles. However, household members who share vehicles should skip non-owner insurance and get added to the family policy instead.

When Non-Owner Insurance Doesn’t Make Sense

The math works against infrequent drivers who rent cars less than twice per year, as rental company coverage costs less for occasional use. Company car drivers already receive protection through their employer’s commercial auto insurance. Understanding these scenarios helps you determine whether alternative coverage solutions might better serve your specific situation.

Alternative Insurance Solutions for Non-Car Owners

Family members can add you as a named driver to their policy for $300-800 annually, which costs less than most non-owner policies. Progressive and State Farm charge an average of $450 per year to add an adult child to their parents’ coverage, while Geico typically charges $520. This option works best when you live in the same household and drive the family vehicle at least once monthly. The coverage follows you when you drive other family-owned vehicles, but excludes rental cars and borrowed vehicles from friends.

Rental Car Coverage Options That Work

Rental companies charge $15-30 daily for their liability coverage, which adds up to $450-900 for monthly renters. Your personal credit card often provides collision damage waiver protection, but offers zero liability coverage for injuries or property damage you cause. American Express Platinum cards cover up to $50,000 in collision damage, while Chase Sapphire Preferred caps at $100,000. Frequent renters save money with annual rental car policies from companies like Allianz (which cost $89 yearly and cover liability gaps that credit cards miss).

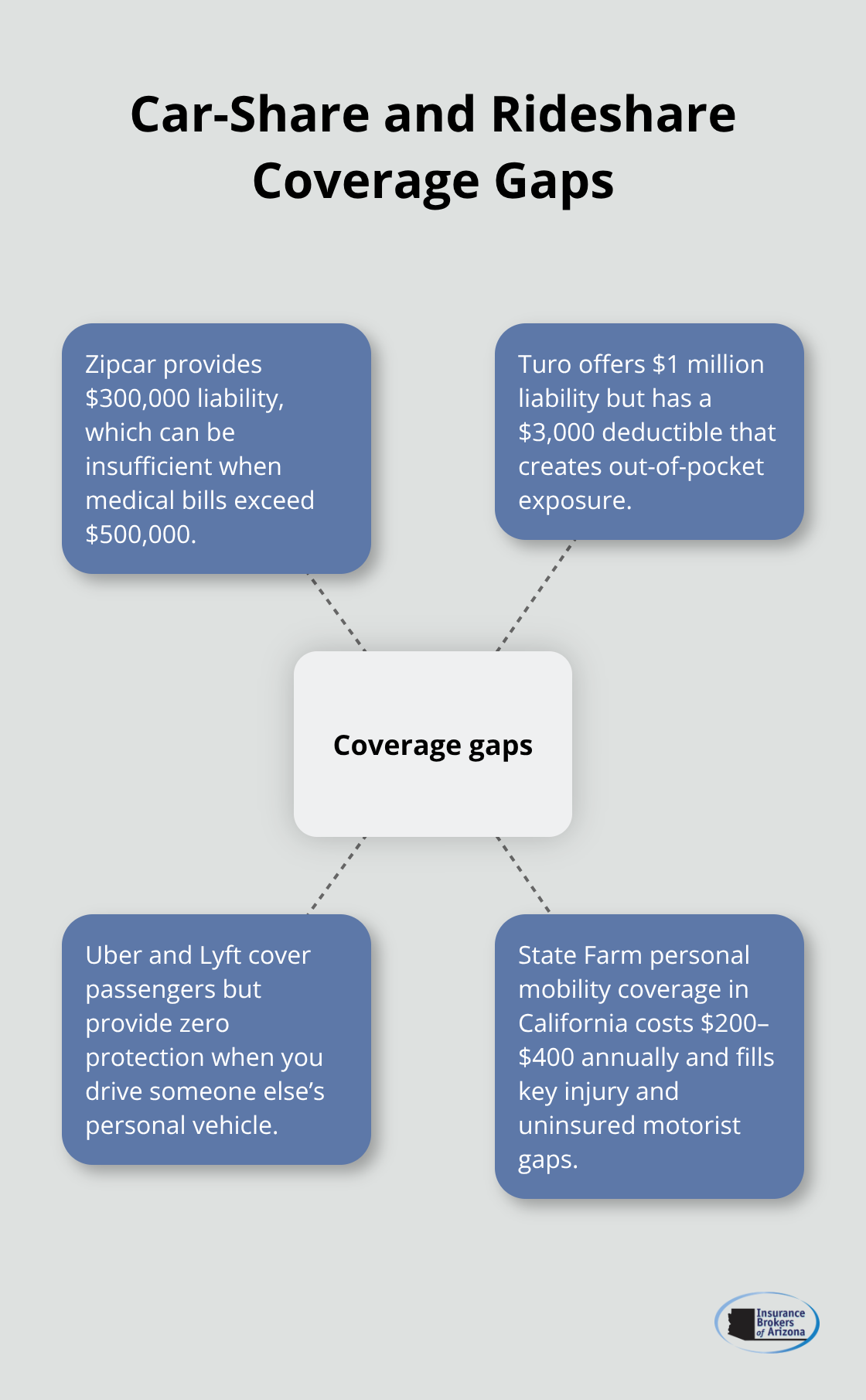

Car-Share and Rideshare Protection Gaps

Zipcar provides only $300,000 liability coverage, which falls short in serious accidents where medical bills exceed $500,000. Turo offers $1 million liability protection, but their $3,000 deductible leaves drivers exposed to significant out-of-pocket costs. Uber and Lyft cover passengers but provide zero protection when you drive someone else’s personal vehicle through their platforms. Personal mobility coverage from State Farm fills these gaps for California residents at $200-400 annually, which covers injuries while you enter or exit rideshare vehicles plus uninsured motorist protection for bicycle and scooter accidents.

Commercial Auto Insurance for Business Use

Company vehicles fall under commercial auto insurance policies that employers maintain for business purposes. These policies typically provide higher liability limits than personal coverage and include protection for employees who drive company vehicles. However, personal use restrictions may apply, and coverage might not extend to your personal vehicle or rental cars outside of business activities.

Once you understand these alternative options, you need to know the specific steps and documentation required to secure any type of auto insurance without vehicle ownership.

How to Purchase Auto Insurance Without a Vehicle

Non-owner car insurance requires specific documentation that differs from standard auto policies. You need a valid driver’s license, Social Security number, and complete records from the past five years. Insurance companies also request your address history and employment information. State Farm and Geico require credit checks for non-owner policies, while Progressive focuses more heavily on your record. Most insurers want to see three years of continuous coverage history, but they make exceptions for new drivers or those who return from military deployment.

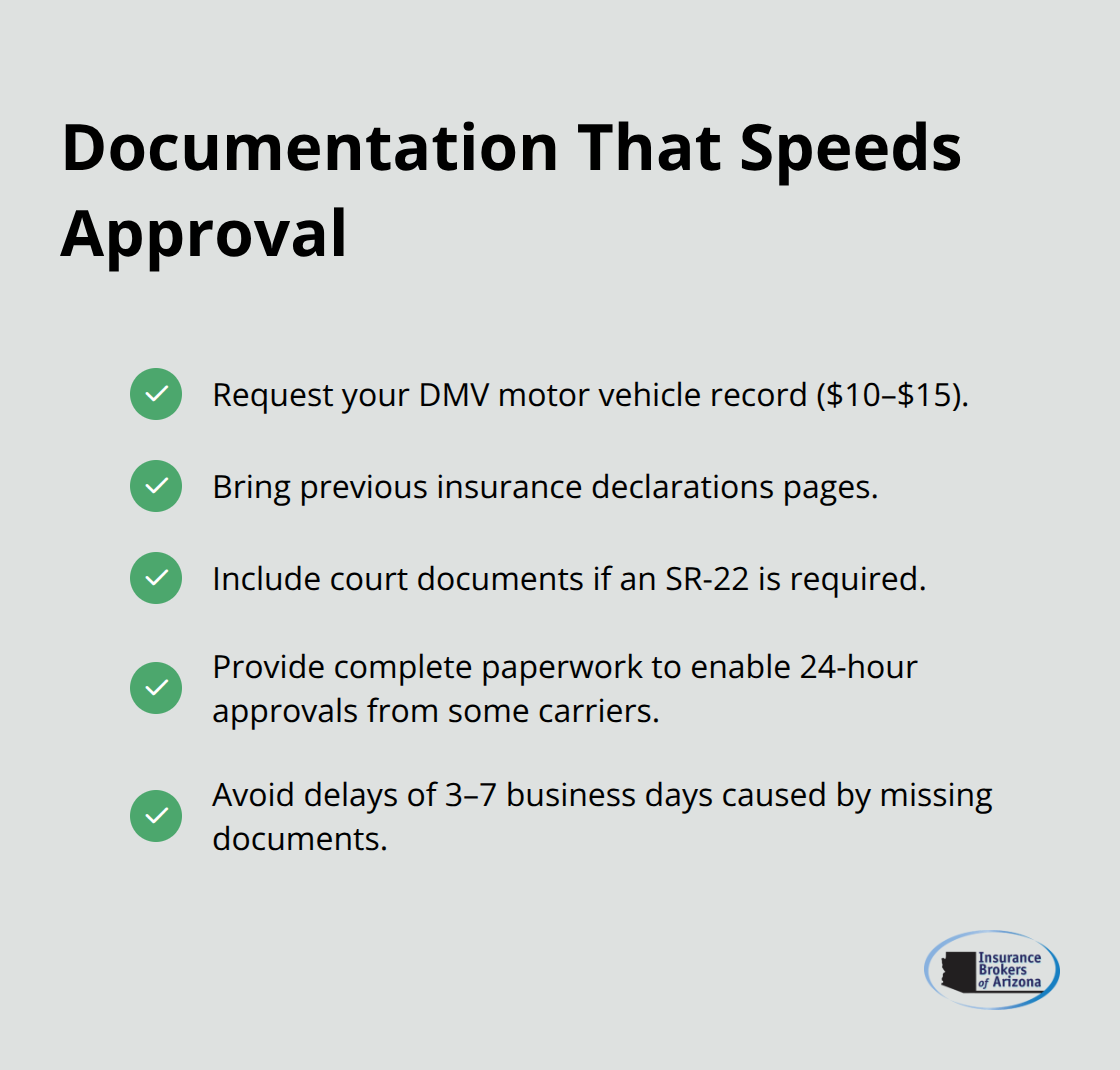

Documentation That Speeds Up Your Application

Your motor vehicle record from the DMV costs $10-15 and shows violations, accidents, and license status that insurers verify anyway. Previous insurance declarations pages prove your coverage history and help secure better rates. If you need SR-22 forms, bring court documents that specify your requirements. Companies like Travelers and Farmers often approve applications within 24 hours when you provide complete documentation upfront.

Missing paperwork delays approval for 3-7 business days and sometimes results in higher premiums.

Quote Comparison Across Multiple Carriers

Non-owner policies aren’t available through online quote systems at most companies. You must call agents directly or visit local offices to get accurate rates. Geico charges $180-320 annually for basic coverage, while State Farm ranges from $250-450. Progressive offers the most competitive rates for drivers with violations at $200-380 yearly. Compare identical coverage limits across carriers because base quotes often include different liability amounts. Request quotes for $100,000 per person and $300,000 per accident to make fair comparisons.

Professional Broker Assistance

Insurance brokers work with multiple carriers to find the lowest rates for non-owner coverage (which saves clients an average of $150 annually compared to single-company shopping). We at Insurance Brokers of Arizona® partner with over 40 reputable carriers to provide competitive options and exceptional customer service. Professional brokers understand state requirements and can match your specific needs with appropriate coverage limits and optional protections.

Final Thoughts

Auto insurance no car situations demand careful evaluation of your habits and financial priorities. Non-owner policies provide substantial value for frequent borrowers and renters, with liability protection that costs 40-60% less than traditional coverage. Annual savings of $300-600 compared to standard policies make this coverage attractive for people who drive regularly without vehicle ownership.

Your decision hinges on how often you drive, your household situation, and specific coverage needs. Family members benefit more from named driver additions to existing policies, while occasional drivers might find rental company coverage sufficient. Car-sharing users face coverage gaps that non-owner policies address effectively (especially when standard rideshare protection falls short).

The application process requires complete documentation and direct contact with insurance agents, as online systems don’t handle these specialized policies. Insurance Brokers of Arizona® partners with multiple reputable carriers to provide personalized coverage solutions for individuals, families, and businesses throughout Arizona. Our expertise in non-owner policies helps clients find the right protection at competitive rates.