Does Your Home Insurance Cover Water Damage?

Water damage strikes one in 50 homes annually, making it the second most common homeowners insurance claim. The question “does home insurance cover water damage” has a complex answer that depends on the source and circumstances.

We at Insurance Brokers of Arizona® see homeowners struggle with coverage gaps daily. Understanding what’s covered and what’s excluded can save you thousands when disaster strikes.

What Water Damage Does Home Insurance Actually Cover

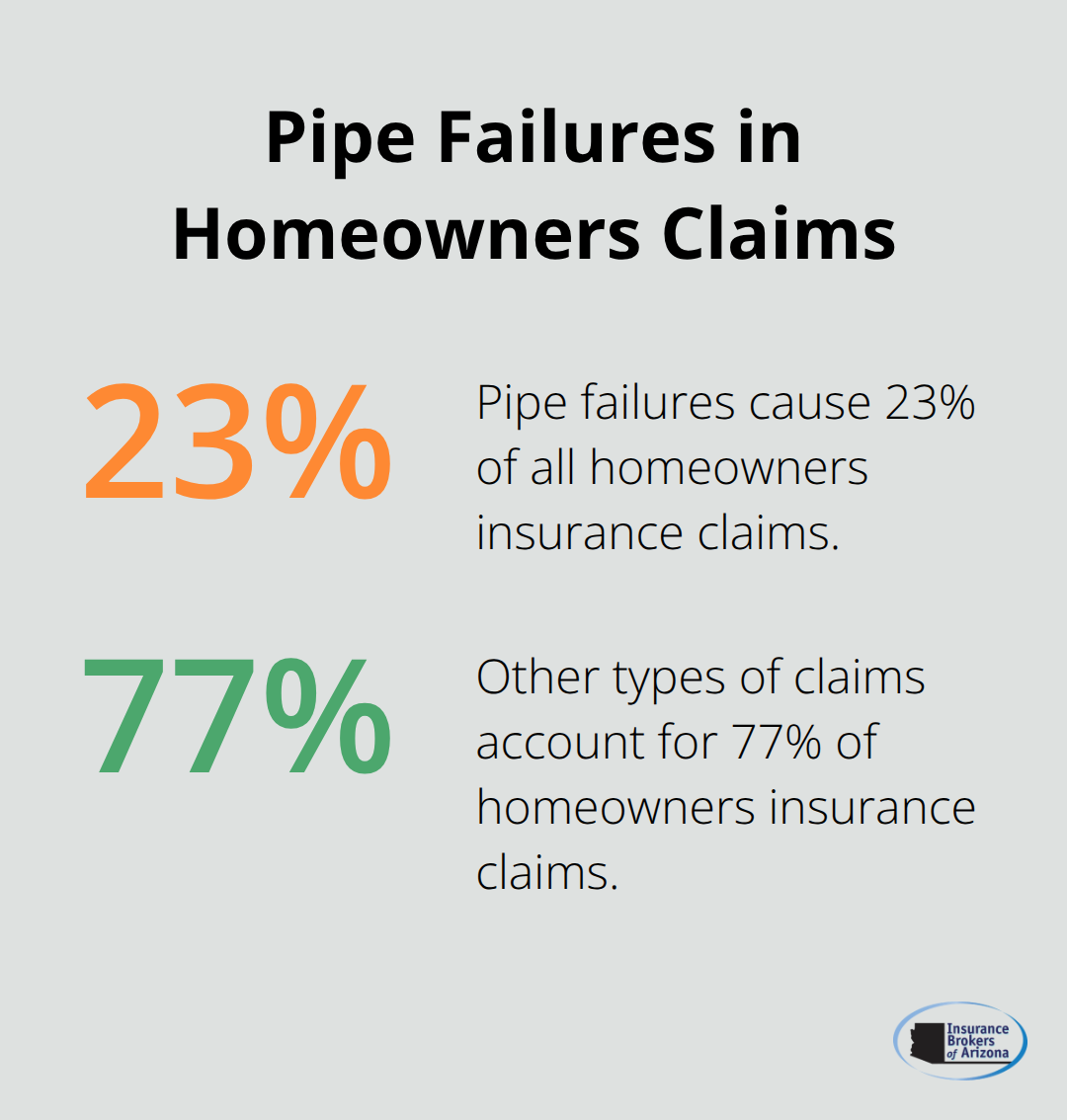

Your standard homeowners policy protects against three specific water damage scenarios that catch most homeowners off guard. The Insurance Information Institute reports that pipe failures cause 23% of all homeowners claims, with burst pipes as the most common covered water damage. The key factor is timing – your policy covers sudden and accidental pipe bursts but excludes gradual leaks that develop over weeks or months.

Sudden Pipe Failures and Pressure Events

When pipes burst from temperature drops or sudden pressure changes, insurance typically pays for both the water damage and temporary repairs needed to stop the flow. Coverage applies when the failure happens without warning, but insurers deny claims for pipes that show signs of deterioration over time. A pipe that bursts during a cold snap receives full coverage, while one that leaks slowly due to corrosion faces denial.

Appliance Malfunctions That Qualify for Coverage

Water heater ruptures, washer overflows, and dishwasher malfunctions fall under covered perils when they happen unexpectedly. The National Association of Insurance Commissioners data shows appliance-related water claims average $5,092 per incident. Your policy covers damage when appliances fail suddenly without maintenance issues. A 10-year-old water heater that bursts without warning gets coverage, while one that shows rust and corrosion for months before failure does not.

Storm-Related Water Intrusion Parameters

Wind-driven rain through damaged windows and doors receives coverage under your policy’s windstorm provisions (assuming the water enters through storm-created openings rather than existing roof problems). Frozen pipe coverage applies when temperatures drop below normal capacity, but pipes that freeze due to inadequate insulation face potential denial. Ice dam coverage works similarly – sudden roof damage from ice buildup qualifies for protection.

These covered scenarios represent just one side of water damage protection. Standard policies exclude several major water sources that homeowners often assume receive coverage.

Water Damage Exclusions in Standard Home Insurance

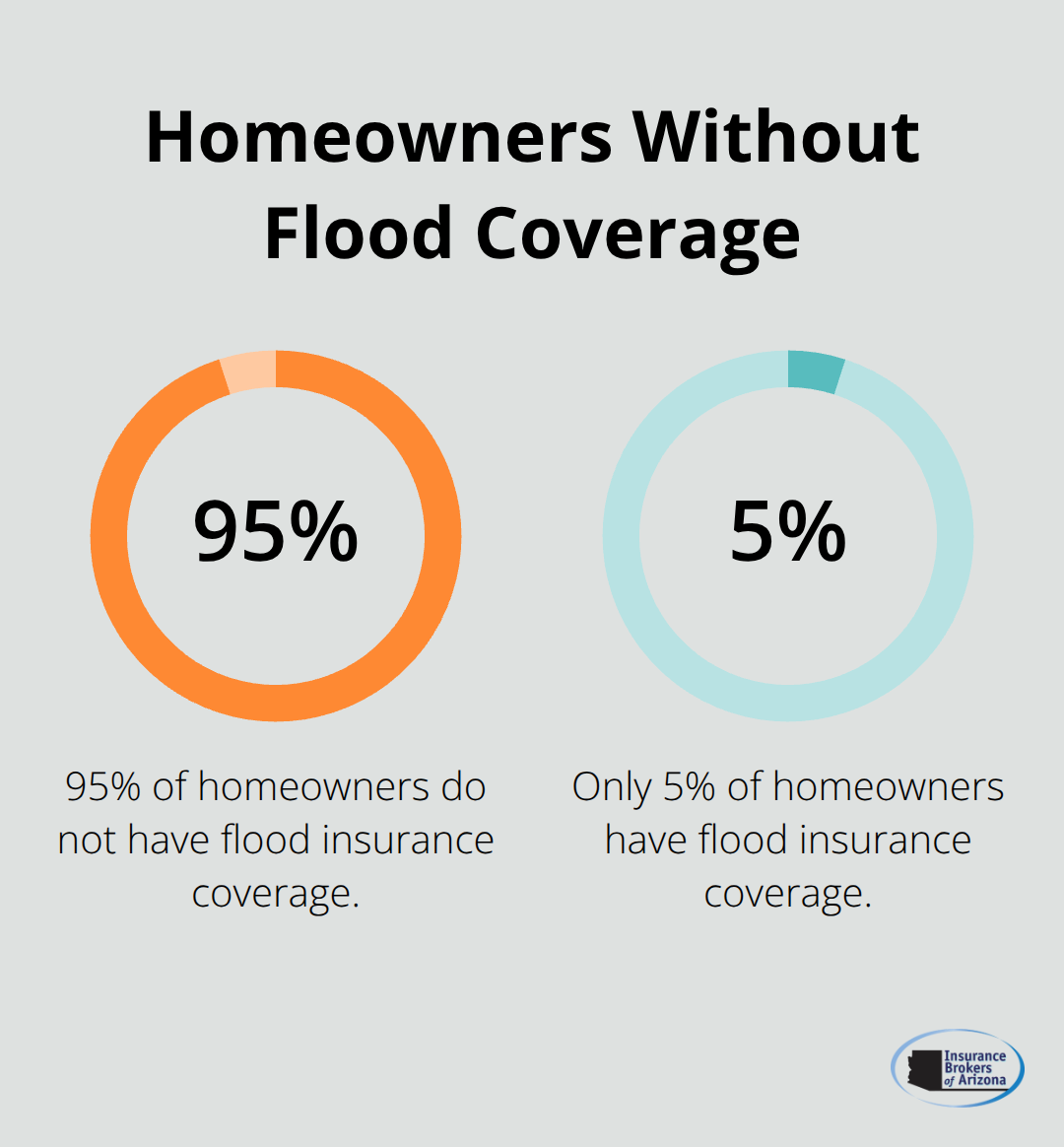

Standard homeowners policies exclude three major water damage categories that catch most homeowners unprepared. The National Flood Insurance Program reports that floods cause $8.2 billion in annual damage, yet 95% of homeowners lack flood coverage. Your policy specifically excludes groundwater, surface water, and any water that touches the ground before it enters your home. This means burst pipes get covered, but basement floods from heavy rain face denial. The Federal Emergency Management Agency defines floods as water that covers two or more acres of normally dry land, which automatically triggers the flood exclusion in your standard policy.

Flood Damage Requires Separate Coverage

Your homeowners policy treats flood damage as a completely separate risk that requires additional insurance. Standard policies exclude all water that originates from outside sources and touches the ground first. Heavy rainfall that pools around your foundation and seeps through basement walls faces automatic denial. Storm surge from hurricanes, river overflow, and rapid snowmelt all fall under flood exclusions regardless of the damage amount.

Gradual Leaks and Maintenance Issues

Insurance companies deny 37% of water damage claims due to maintenance issues, according to the Property Casualty Insurers Association of America. A toilet that leaks for weeks before it causes floor damage will face denial, while a sudden pipe burst gets full coverage. Roof leaks from missing shingles or clogged gutters fall under maintenance exclusions. Insurers expect annual inspections and prompt repairs to prevent gradual damage that develops over time.

Sewer and Drain Backup Limitations

Standard policies exclude water backup from sewers, drains, and sump pumps unless you purchase specific endorsements. The Insurance Information Institute data shows sewer backup claims average $3,000 per incident, making this exclusion expensive for unprepared homeowners. Heavy rainfall that overwhelms municipal systems causes most backup events, but your base policy provides zero protection. Water backup endorsements cost $40-60 annually but cover damage from external sewer systems and internal drain failures.

These exclusions create significant coverage gaps that smart homeowners address through additional protection options and proper documentation strategies.

How to Maximize Your Water Damage Coverage

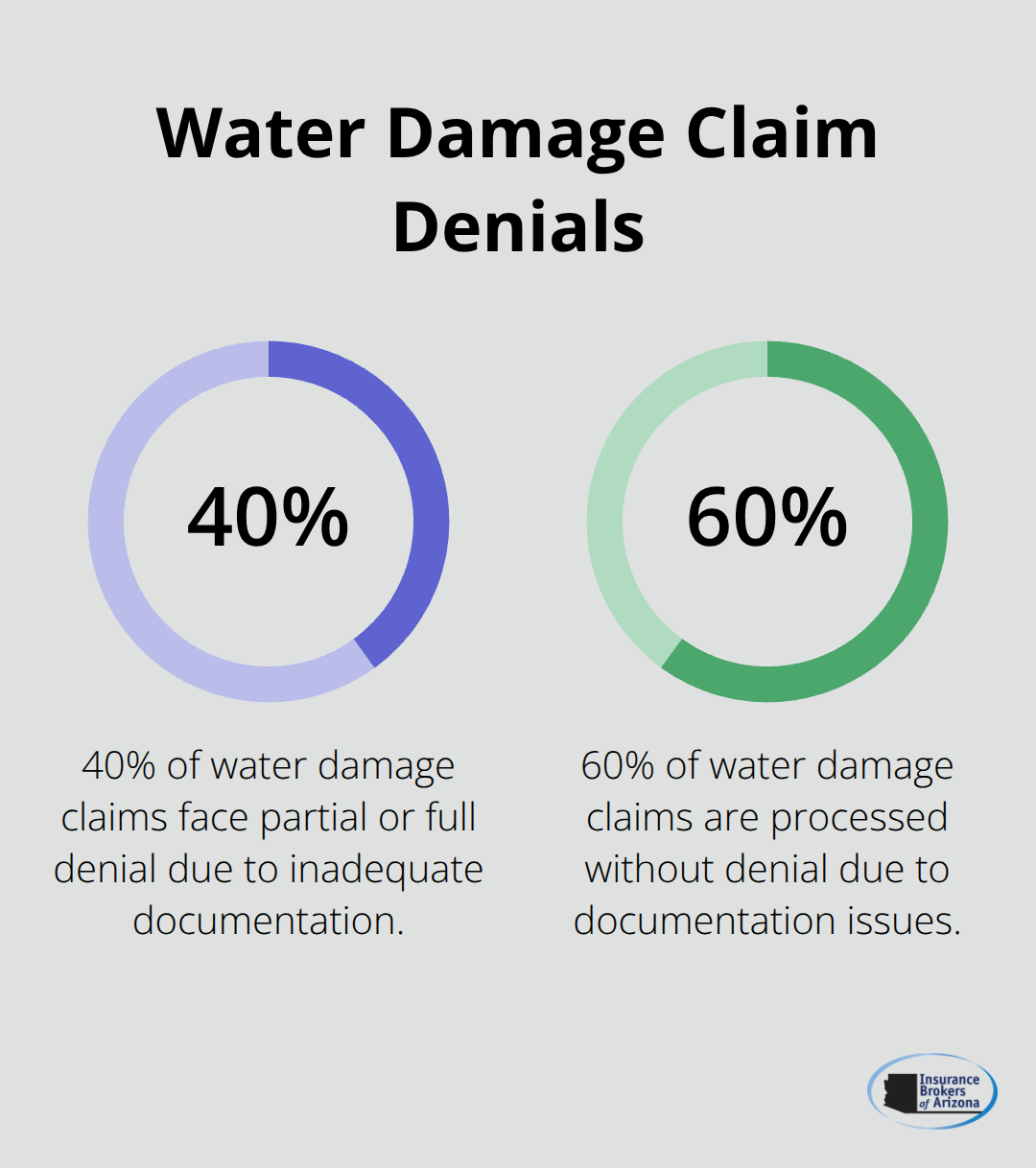

Smart homeowners take three specific actions that prevent claim denials and coverage gaps. The Insurance Information Institute reports that 40% of water damage claims face partial or full denial due to inadequate documentation, while homeowners who maintain detailed records receive 94% faster claim processing. Your protection strategy starts with quarterly home inspections that document appliance conditions, plumbing status, and potential problem areas.

Document Your Property and Belongings Systematically

Take dated photos of water heaters, washing machines, and visible pipes every three months to establish maintenance patterns. The Federal Emergency Management Agency data shows that homeowners with photographic evidence receive settlements that average 23% higher than those without documentation. Create a digital inventory that includes serial numbers, purchase dates, and current conditions of all water-connected appliances. Store these records in cloud storage so water damage cannot destroy your documentation when you need it most.

Know Your Policy Limits and Deductibles

Standard homeowners policies carry water damage deductibles that range from $500 to $2,500, but most homeowners cannot identify their specific deductible amount when they file claims. The National Association of Insurance Commissioners reports that 67% of homeowners underestimate their actual coverage limits for personal property water damage. Your policy likely caps water damage coverage at 10-20% of your dwelling coverage (meaning a $300,000 home receives only $30,000-$60,000 for contents damage). Review your declarations page annually to identify sub-limits that could leave you underinsured.

Purchase Strategic Coverage Endorsements Before You Need Them

Water backup coverage becomes worthless after heavy rains start, since most endorsements require 30-day waiting periods before activation. Water backup endorsements cost $40-60 per year but provide $5,000-$25,000 in additional protection for sewer and drain failures. Service line coverage protects underground utility connections from your home to the street and covers repairs that average $3,000-$8,000 per incident according to HomeAdvisor data. Equipment breakdown endorsements cover water heater and HVAC system failures that cause secondary water damage. Property owners should calculate their potential losses carefully and select coverage that meets their needs for at least 12 months.

Final Thoughts

The answer to “does home insurance cover water damage” depends entirely on the source and timing of the water intrusion. Your standard policy covers sudden pipe bursts, appliance failures, and storm-related damage but excludes floods, gradual leaks, and sewer backups. These exclusions create expensive gaps that catch unprepared homeowners.

Review your current policy declarations page to identify your water damage deductible and coverage limits. Most policies cap personal property water damage at 10-20% of dwelling coverage (which may leave you underinsured). Check whether you have water backup coverage, service line protection, and equipment breakdown endorsements that prevent costly surprises.

The complexity of water damage coverage makes professional guidance valuable. We at Insurance Brokers of Arizona® help identify coverage gaps before they become expensive problems. Water damage strikes without warning, but proper coverage protects your financial security when disaster hits your home.