How Much Does General Liability Insurance Cost for SMBs?

Small business owners frequently ask: how much is general liability insurance for small business? The answer varies dramatically based on your industry, company size, and coverage needs.

We at Insurance Brokers of Arizona® see premiums ranging from $400 to $3,000 annually for most small businesses. Understanding the key cost factors helps you budget effectively and find the right protection for your company.

Factors That Affect General Liability Insurance Costs

Industry Type Creates the Largest Premium Differences

Your industry determines your general liability premiums more than any other factor. Construction companies pay an average of $2,408 annually according to Insureon data, while accounting firms typically pay just $675. Healthcare providers and restaurants face higher premiums due to frequent slip-and-fall claims and professional errors.

Manufacturing businesses with heavy machinery see elevated rates because equipment accidents create expensive bodily injury claims. Professional services like consultants average $780 per year, which reflects their lower physical risk profile. High-risk industries pay substantially more because insurers expect more frequent and costly claims.

Business Size and Annual Revenue

Insurance carriers calculate premiums based on your annual revenue because higher sales volumes correlate with increased claim exposure. Companies that earn under $300,000 annually pay significantly less than those that generate $1 million or more. Insureon research shows businesses with revenues between $500,000 and $1 million face premiums 40-60% higher than smaller operations.

Employee count amplifies this effect – each additional worker increases your liability exposure and premium costs accordingly. More employees mean greater chances of workplace accidents and customer interactions that could lead to claims.

Coverage Limits and Deductible Choices

Standard $1 million per occurrence and $2 million aggregate limits cost around $500-800 annually for most small businesses. When you double these limits to $2 million per occurrence, premiums typically increase by 25-35%. Your deductible choice significantly affects costs – a $2,500 deductible instead of $500 can reduce premiums by 15-20%.

Higher deductibles mean more out-of-pocket expenses when claims occur, so you must balance upfront savings against potential future costs. Most small businesses (according to Insureon data) select $500 deductibles to keep claim costs manageable.

These cost factors work together to create your unique premium rate, but smart business owners can take specific steps to reduce their insurance expenses.

Average General Liability Insurance Costs by Business Type

Professional Services Pay the Lowest Premiums

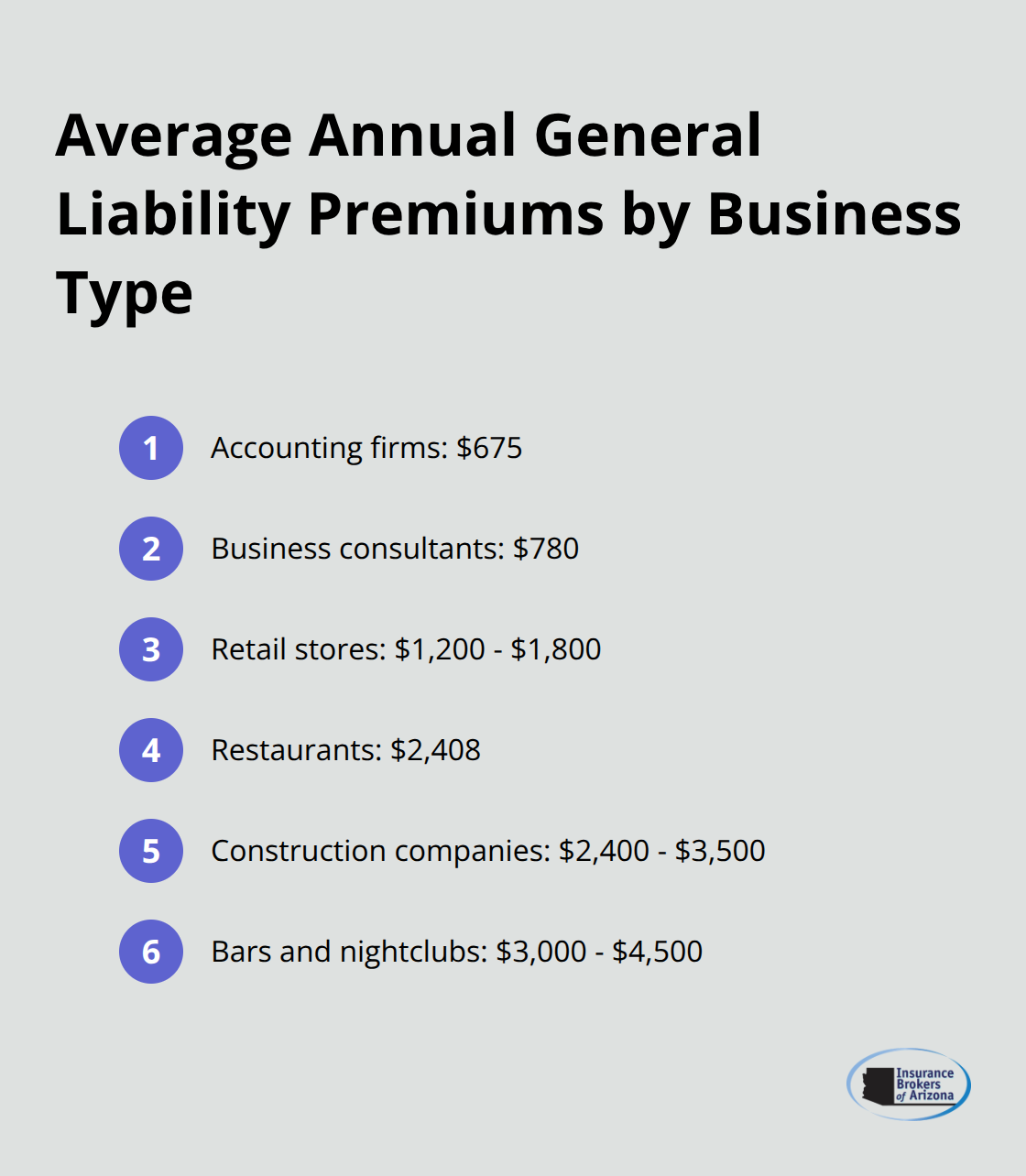

Professional services and consultants pay the lowest general liability premiums among all business categories. Accounting firms average $675 annually according to Insureon data, while business consultants pay around $780 per year. These low rates reflect minimal physical risks – most claims involve minor property damage or personal injury during client visits.

Technology consultants and marketing firms typically fall within this $600-900 range because their work environments pose limited liability exposure. Law firms and financial advisors also benefit from these reduced rates since their operations rarely involve physical hazards that lead to expensive claims.

Retail Businesses Face Moderate Premium Costs

Retail businesses encounter higher premiums due to constant customer traffic and slip-and-fall risks. Small retail stores pay approximately $1,200-1,800 annually for general liability coverage. Clothing stores and gift shops typically pay less than electronics retailers because expensive merchandise creates higher property damage exposure.

Grocery stores and pharmacies fall into the middle range at $1,400-2,000 annually. These businesses handle more foot traffic than specialty retailers but maintain safer environments than restaurants or bars.

Restaurants Represent High-Risk Retail Operations

Restaurants represent the highest-risk retail category, with average premiums that reach $2,408 per year according to industry data. Food service businesses face frequent slip-and-fall claims, foodborne illness lawsuits, and burns from hot equipment. Fast-casual restaurants typically pay less than full-service establishments because they have fewer servers and simpler operations.

Bars and nightclubs pay even higher premiums (often $3,000-4,500 annually) due to alcohol-related incidents and late-night operations that increase liability exposure.

Construction Companies Pay the Highest Rates

Construction and trade contractors face the steepest general liability costs in any industry. General contractors average $2,400-3,500 annually, while specialized trades like plumbers or electricians range from $1,800-2,800. These elevated rates stem from constant injury risks, expensive equipment damage, and potential structural problems that create massive liability exposure.

Roofing contractors pay even higher premiums because falls from heights generate severe injury claims that can exceed $500,000. These significant cost differences highlight why contractors must implement comprehensive safety programs to control their insurance expenses.

Ways to Reduce General Liability Insurance Premiums

Safety Programs Deliver Immediate Premium Reductions

Insurance carriers offer substantial discounts to businesses that implement documented safety programs. Restaurants that install slip-resistant floors and train staff on spill response protocols can reduce premiums by 10-15% according to industry data. Construction companies with OSHA-compliant safety programs and regular toolbox talks often receive 20-25% discounts from carriers like The Hartford and Liberty Mutual.

Workers’ compensation claims directly impact general liability rates because injured employees sometimes file additional liability claims. Manufacturing businesses that reduce their workers’ comp claims by 50% through safety measures typically see general liability premiums drop by 15-20% within two years. Document all safety initiatives with photos, records, and incident reports – insurers require proof of active risk management to approve discounts.

Bundle Policies for Maximum Savings

Business Owner’s Policies that combine general liability with commercial property insurance cost around $684 annually according to Insureon data – significantly less than separate policy purchases. This approach saves most small businesses 20-30% compared to individual policy purchases. Professional liability insurance bundled with general liability creates additional savings of 10-15% for consultants and service providers.

Commercial auto insurance bundled with general liability generates even larger discounts for businesses with vehicles. Insureon research shows that businesses that purchase three or more policies from the same carrier receive average savings of 25% on their total premiums. Pay annual premiums upfront instead of monthly payments to avoid fees that add 8-12% to your total costs.

Aggressive Quote Comparison Cuts Costs

General liability premiums vary by 40-60% between carriers for identical coverage according to industry studies. Businesses pay $1,200 with one insurer and $750 with another for the same $1 million limits. Request quotes from at least five carriers because regional insurers often beat national companies on rates for specific industries. Independent agents who represent multiple carriers can streamline this comparison process and identify the lowest rates quickly.

Newer insurance companies like Next Insurance and Thimble often offer 20-30% lower rates than established carriers to gain market share. However, financial stability ratings matter – stick with carriers rated A- or better by A.M. Best to avoid payment delays during claims.

Final Thoughts

General liability insurance costs for small businesses range from $400 to $3,000 annually, with industry type creating the largest premium differences. Professional services pay around $675-780 per year, while construction companies face costs of $2,400 or more. Your business size, revenue, coverage limits, and claims history all influence final premiums.

The question “how much is general liability insurance for small business” depends on these specific factors that work together. Safety programs, policy bundling, and aggressive quote comparison can reduce costs by 20-40%. Premium variations of 40-60% between carriers make professional guidance valuable for most business owners.

We at Insurance Brokers of Arizona® help businesses across all industries secure competitive rates through our network of reputable carriers. Start by collecting your business information including annual revenue, employee count, and prior claims history (if any). Request quotes from multiple carriers or contact an experienced broker who can streamline the comparison process and negotiate better rates on your behalf.