Is Commercial Auto Insurance More Expensive?

Commercial auto insurance often comes with a higher price tag than personal auto coverage. At Insurance Brokers of Arizona®, we frequently field questions about how much more expensive commercial auto insurance is compared to personal policies.

This blog post will explore the factors that influence commercial auto insurance costs, compare it to personal auto coverage, and provide strategies to help businesses reduce their premiums while maintaining adequate protection.

What Drives Commercial Auto Insurance Costs?

Commercial auto insurance rates depend on several key factors. Businesses that understand these elements can make informed decisions about their coverage and potentially reduce their premiums.

Vehicle Type and Usage

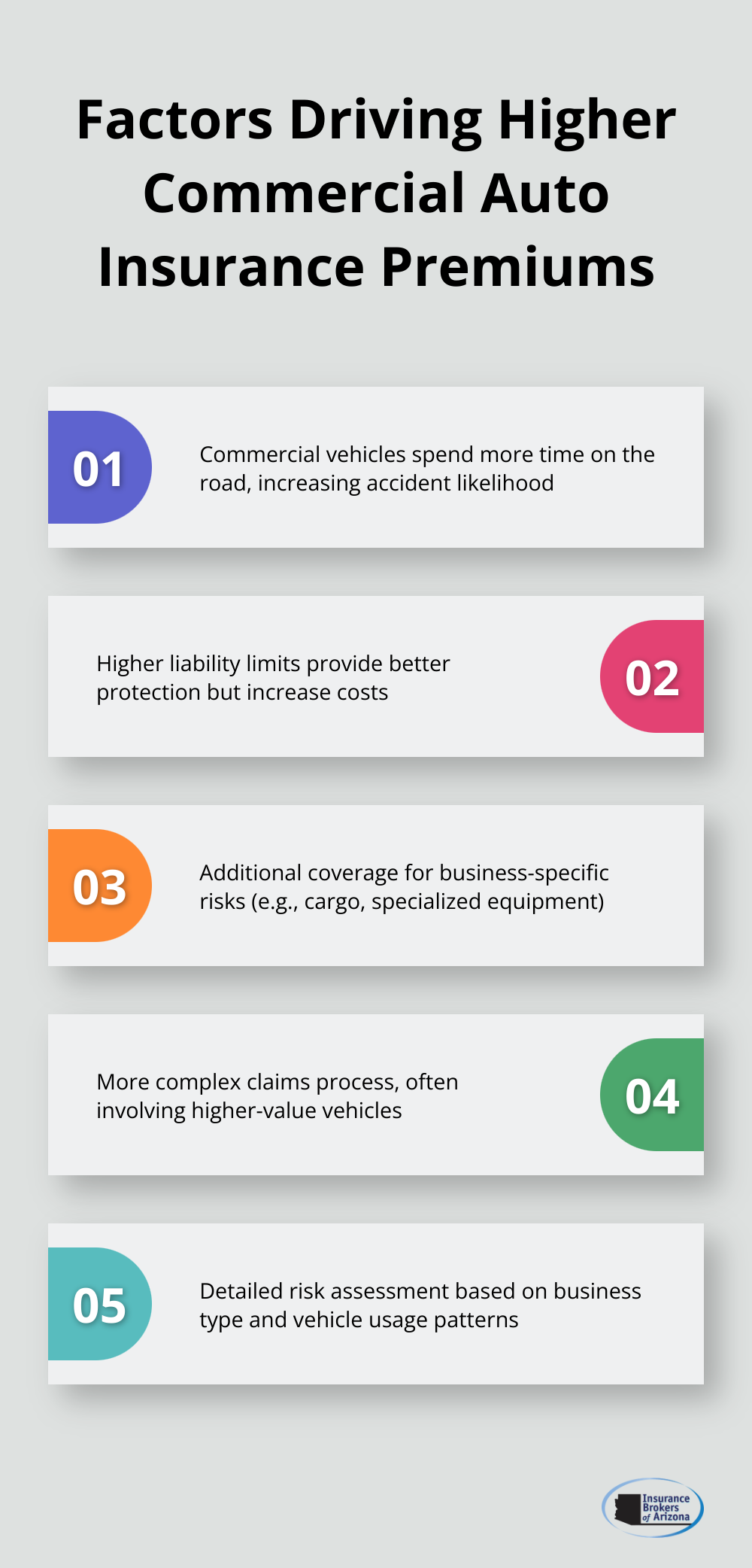

The type of vehicle and its use significantly influence insurance costs. Larger vehicles, such as trucks or vans, typically cost more to insure due to their higher potential for damage in accidents. The Insurance Information Institute reports that commercial vehicles often spend more time on the road than personal vehicles, which increases the likelihood of accidents and claims.

Driver Experience and Safety Record

Driver experience and safety records directly impact insurance rates. A study by the American Transportation Research Institute found that drivers with clean records help businesses secure lower premiums. Strict hiring criteria and ongoing driver training programs can lead to substantial savings for businesses (though individual results may vary).

Coverage Limits and Risk Factors

The level of coverage a business chooses and the specific risks associated with its operations affect premiums. Higher liability limits provide better protection but increase costs. The National Association of Insurance Commissioners reports that typical commercial policies start at $1 million of liability coverage (a significantly higher amount than personal auto policies).

Location and Industry-Specific Risks

Business location and industry play crucial roles in determining insurance costs. Urban areas generally have higher premiums due to increased traffic and accident rates. Additionally, businesses in high-risk industries (such as construction or transportation) often face higher insurance costs due to the nature of their operations.

Vehicle Fleet Size

The number of vehicles in a business’s fleet also impacts insurance costs. Larger fleets typically require more comprehensive coverage and may face higher overall premiums. However, some insurers offer fleet discounts for businesses with multiple vehicles under one policy.

These factors help insurance professionals find the right balance between comprehensive coverage and affordable premiums. The next section will compare commercial auto insurance to personal auto coverage, highlighting the key differences that contribute to their cost disparities.

How Commercial and Personal Auto Insurance Differ

Commercial and personal auto insurance policies serve different purposes and come with distinct features that impact their costs and coverage. These differences explain why commercial policies typically come with higher premiums.

Coverage Scope and Liability Limits

Commercial auto insurance offers broader coverage and higher liability limits than personal policies. A typical personal auto policy might provide liability coverage of $100,000 to $300,000, while commercial policies often start at $1 million. This increased protection is essential for businesses, as they face greater financial risks in the event of an accident.

The Insurance Information Institute reports that commercial vehicles have a higher likelihood of involvement in accidents due to increased time on the road. This higher risk exposure necessitates more comprehensive coverage, which drives up premiums.

Additional Endorsements and Specialized Coverage

Commercial auto policies often include endorsements not typically found in personal policies. These may cover hired and non-owned vehicles, cargo, or specialized equipment. For example, a construction company might need coverage for tools and materials transported in their vehicles, while a catering business might require protection for refrigeration units.

These additional coverages reflect the diverse needs of businesses and contribute to the overall cost of commercial auto insurance. However, they also provide essential protection that can save businesses from significant financial losses.

Claims Process and Business Interruption

The claims process for commercial auto insurance differs from personal policies. Business claims often involve more complexity, with multiple parties, higher-value vehicles, or specialized equipment. Additionally, commercial policies may include coverage for business interruption, which compensates for lost income if a vehicle crucial to operations is out of commission due to an accident.

According to the National Association of Insurance Commissioners, the average commercial auto insurance claim significantly exceeds personal auto claims. This difference stems from factors such as more expensive vehicles, potential cargo loss, and the impact on business operations.

Risk Assessment and Pricing

Insurance companies assess risk differently for commercial and personal auto policies. Factors such as the type of business, vehicle usage patterns, and driver qualifications play a more significant role in commercial auto insurance pricing. This detailed risk assessment often results in higher premiums for commercial policies.

Flexibility and Customization

Commercial auto insurance policies offer more flexibility and customization options than personal policies. Businesses can tailor their coverage to specific needs, adding or removing endorsements as their operations change. This flexibility allows for more comprehensive protection but can also contribute to higher costs.

The stark differences between commercial and personal auto insurance highlight the importance of choosing the right coverage for your business needs. In the next section, we will explore strategies to reduce commercial auto insurance costs without compromising on essential protection.

How to Lower Commercial Auto Insurance Costs

Commercial auto insurance represents a significant expense for many businesses. However, several effective strategies can reduce costs without compromising essential coverage. This chapter explores proven methods to lower your premiums while maintaining adequate protection.

Prioritize Driver Safety

A comprehensive fleet safety program is one of the most effective ways to reduce insurance costs. The National Safety Council reports that companies which prioritize driver safety can reduce accident rates by up to 15%. This reduction directly translates to lower insurance premiums.

To improve driver safety:

- Conduct regular driver training sessions that focus on defensive driving techniques and proper vehicle handling.

- Use telematics devices to monitor driver behavior and provide feedback. Many insurance companies offer discounts for businesses that effectively use these technologies.

- Implement a strict cell phone policy while driving. The National Highway Traffic Safety Administration reports that distracted driving causes thousands of accidents each year. A no-phone policy can significantly reduce your risk profile.

Optimize Your Coverage

A careful review of your policy ensures you’re not over-insured. While adequate coverage is important, paying for unnecessary extras can inflate your premiums. Work with your insurance agent to identify areas where you can adjust coverage without exposing your business to undue risk.

One strategy involves choosing higher deductibles. An increase in your deductible from $500 to $1,000 could potentially lower your premium by 10% to 20%. However, ensure your business can comfortably cover the higher out-of-pocket expense in case of a claim.

Leverage Policy Bundling

Many insurance providers offer discounts when you bundle multiple policies together. A combination of your commercial auto insurance with other business coverages (like general liability or property insurance) could save up to 15% on your total insurance costs.

Invest in Vehicle Maintenance

Regular vehicle maintenance not only extends the life of your fleet but also reduces the likelihood of accidents due to mechanical failures. The U.S. Department of Transportation estimates that about 12% of crashes involve vehicle-related factors.

To maintain your vehicles effectively:

- Implement a strict maintenance schedule for all your vehicles.

- Include regular oil changes, tire rotations, and brake inspections.

- Address any issues promptly.

- Keep detailed records of all maintenance activities (some insurance providers offer discounts for well-maintained fleets).

These strategies can significantly reduce your commercial auto insurance costs while maintaining robust coverage. The key is to work closely with your insurance provider to find the right balance between cost savings and adequate protection.

Final Thoughts

Commercial auto insurance costs more than personal coverage due to increased risks and higher liability limits. Businesses face greater financial exposure, which justifies the higher premiums. The question of how much more expensive commercial auto insurance is depends on various factors specific to each business.

Companies can reduce their insurance costs without sacrificing protection. Implementing safety programs, optimizing coverage, and maintaining vehicles regularly will help lower premiums. These strategies allow businesses to balance comprehensive coverage with affordable rates.

Insurance Brokers of Arizona® offers expert guidance to navigate commercial auto insurance complexities. Our team works with over 40 carriers to find competitive options tailored to your needs (ensuring the best protection for your business). We strive to secure optimal coverage at the most favorable rates for our clients.