Commercial Property Insurance Rates: What Affects Your Premium

Commercial property insurance rates vary wildly depending on where your building sits, what it’s made of, and what happens inside it. We at Insurance Brokers of Arizona® see firsthand how one business pays half what another pays for nearly identical coverage.

The good news is that your premium isn’t set in stone. Understanding what drives these costs gives you real leverage to negotiate better rates and cut unnecessary expenses.

What Drives Your Commercial Property Insurance Premium

Location hits your premium first, and it’s non-negotiable. Properties in areas prone to wildfires, hail, or severe convective storms pay substantially more than those in low-risk zones. Proximity to fire stations and hydrants directly lowers your rate-insurers track this data and reward properties near strong fire protection infrastructure. Arizona properties in wildfire-prone regions face premiums that reflect the real exposure, while downtown Phoenix locations with excellent fire departments receive better terms. Beyond natural disasters, local crime rates matter. High-theft areas trigger higher premiums because theft claims are frequent and costly. If your building sits in a neighborhood with rising crime statistics, your rate reflects that risk profile.

Building Construction Shapes Your Fire Rating

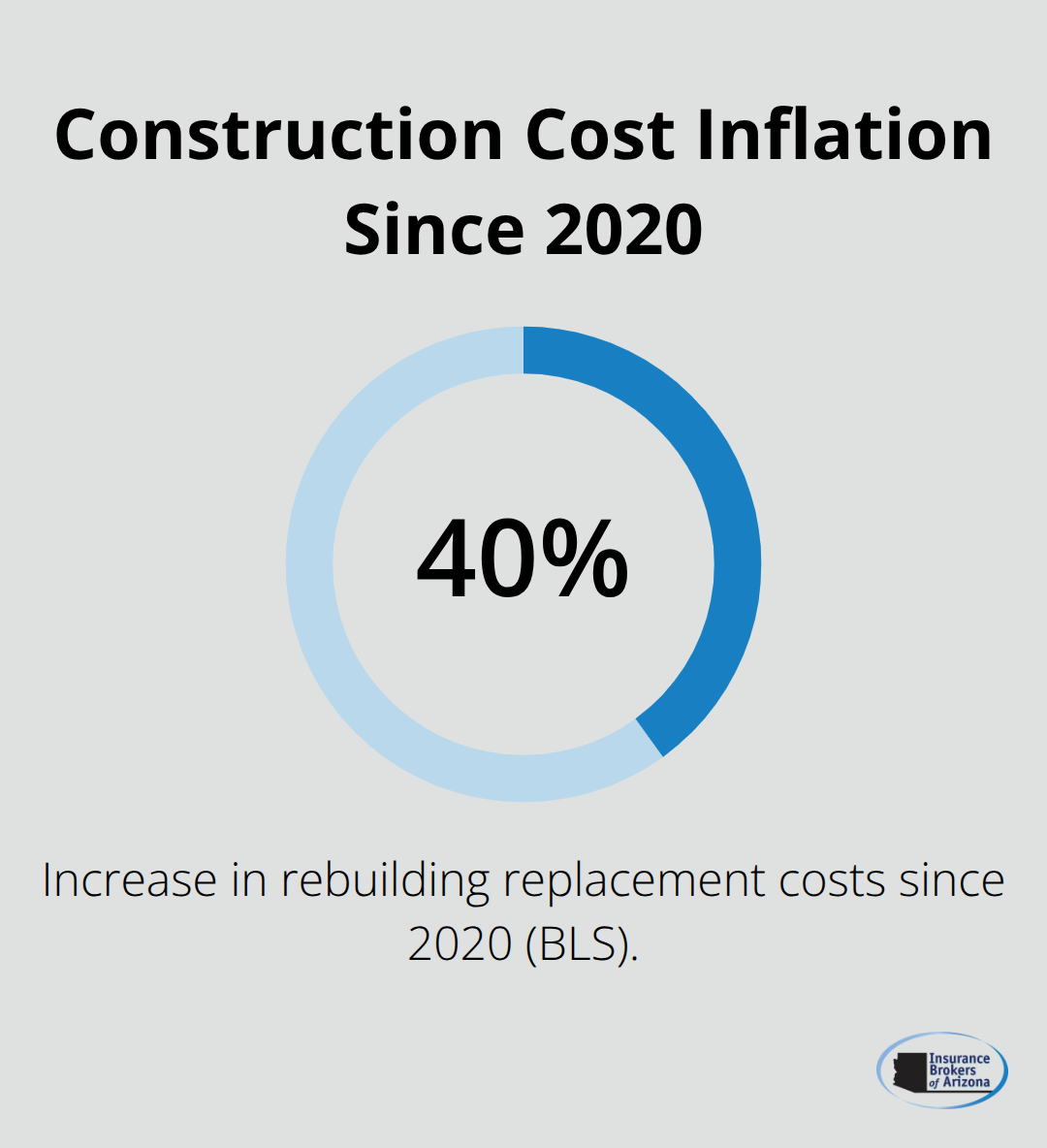

What your building is made of determines your fire rating, which then determines your rate. Non-combustible materials like steel and concrete earn better rates than wood-frame structures. If you occupy an older building with combustible elements, your premium reflects that exposure. Remodeling to upgrade fire ratings-such as installing fire-resistant drywall or upgrading to non-combustible roofing-can lower your premium over time. Carriers use ISO fire ratings that account for building materials, so even internal structural choices impact your cost. Wood partitions in a supposedly fire-resistant building undermine the rating and keep premiums high. Age compounds the problem. Buildings constructed before modern fire codes were implemented typically cost more to insure because they lack safety features newer buildings have standard. Replacement cost for rebuilding has climbed nearly 40 percent since 2020, according to Bureau of Labor Statistics data, so older buildings often require higher coverage limits to reflect true replacement value. This inflation in construction costs pushes premiums upward across the board.

Accurate Valuation Prevents Costly Penalties

Underinsuring is the most expensive mistake businesses make. If your building and contents are worth $1.5 million but you only insure $1 million, a total loss triggers coinsurance penalties that force you to absorb a portion of the claim yourself. Carriers penalize underinsured properties heavily, and this gap becomes catastrophic when you need it most. Accurate valuation is not optional-it’s the foundation of appropriate premiums. Properties with higher replacement values naturally carry higher premiums because the carrier’s maximum exposure is larger. A warehouse with $500,000 in inventory pays more than an office with $50,000 in equipment. The coverage limits you select directly correlate to your rate.

Deductibles and Coverage Choices Lower Your Cost

Raising your deductible from $2,500 to $10,000 can substantially reduce your annual premium, but only if you can actually pay that deductible when a claim occurs. Try aligning your deductible with what your business can afford to cover out of pocket. Location, construction quality, and accurate valuation work together to determine your baseline premium. Carriers assess all three factors simultaneously, not in isolation. Once you understand how these elements shape your rate, you can identify which industry-specific risks apply to your operation and where you have real opportunities to cut costs.

How Your Industry and Safety Record Shape What You Pay

Your Occupancy Classification Sets Your Baseline Rate

Your industry classification predicts your commercial property insurance premium more accurately than almost any other factor after location and building condition. Restaurants and auto repair shops pay substantially more than accounting offices because their operations create higher exposure to fire, theft, and liability claims. Manufacturing facilities with hazardous materials face premiums that reflect catastrophic loss potential. Retail operations with high customer traffic and frequent inventory turnover sit in the middle-higher risk than offices but lower than restaurants or industrial operations.

Your carrier assigns your business to a specific occupancy class, and that classification determines your baseline rate before any other factors are considered. If you operate in a multi-tenant building where another tenant runs a high-risk operation, your entire building’s premium can increase because the carrier assesses the collective exposure. A restaurant sharing a plaza with your office means your premium reflects the fire and liability risks that the restaurant introduces.

Multi-Tenant Buildings Amplify Your Risk Profile

Shared buildings create shared risk. Your carrier doesn’t evaluate your office in isolation-they evaluate the entire property and all its tenants. A hazardous tenant (restaurant, auto shop, chemical storage) raises premiums for every business in that building. This is why understanding your occupancy classification matters. It’s not subjective, and it’s not negotiable within your industry category, but it does explain why identical businesses in different buildings pay different rates.

Claims History Acts as a Rate Multiplier

Your claims history and safety record multiply your baseline rate up or down. A business with zero claims over five years receives better renewal pricing than one with two theft claims and a minor fire loss. Carriers use loss history to predict future claims, and that prediction directly affects what you pay. If your business experienced $50,000 in claims over the past three years, your renewal premium reflects the probability that similar losses will recur.

Safety Investments Reduce Your Premium

Installing monitored security systems, fire sprinklers, and fire alarms demonstrates that you take loss prevention seriously, and carriers reward this investment with lower premiums. A documented safety program that your staff actually follows lowers your rate because it reduces claim frequency. Businesses that invest in risk management see measurable premium reductions at renewal because their loss experience improves. This is not theoretical-carriers track which businesses make safety investments and which ones don’t, and they adjust pricing accordingly.

Business Continuity Planning Signals Risk Discipline

The AGC 2025 Construction Hiring and Outlook report highlights that skilled labor shortages extend rebuilding timelines after disasters, which increases business interruption exposure. Carriers price this risk into premiums for businesses without strong continuity plans. Implementing a formal business continuity plan signals to your carrier that you’ve thought through recovery and reduces their perception of your operational risk. Your safety record becomes your negotiating position at renewal, and it directly influences what happens when you shop for new coverage or renew your existing policy.

How to Cut Your Commercial Property Insurance Premium

Security and Fire Protection Systems Deliver Immediate Savings

Security and fire protection systems lower your premium faster than almost any other investment. Monitored fire alarms, sprinkler systems, and security cameras signal to underwriters that you take loss prevention seriously, and they reduce your rate accordingly. The National Fire Protection Association and ISO guidelines directly tie these protections to premium reductions because they demonstrably lower claim frequency. A business that installs a monitored sprinkler system sees a measurable rate reduction at the next renewal because the carrier’s risk exposure drops. Fire stations and hydrants matter less if your building has internal suppression. Proximity to fire protection infrastructure still counts, but active fire suppression systems inside your building override some of that location disadvantage. If you’re in a building with poor fire protection proximity, upgrading your internal systems pays for itself through premium savings within a few years.

Security systems work the same way. A documented alarm system with 24-hour monitoring reduces theft claims, and carriers price this protection into your renewal quote. The investment typically costs between $1,000 and $5,000 for installation (depending on building size), and the annual premium savings often recover that cost within two to three years.

Maintenance Records Lower Your Renewal Rate

Regular property inspections and maintenance prevent small problems from becoming expensive claims that destroy your loss history. A roof inspection every two years catches deterioration before water damage spreads through your building. HVAC maintenance prevents equipment breakdown claims. Electrical system inspections identify fire hazards before they ignite. This preventive approach directly impacts your renewal premium because carriers review your maintenance records and adjust pricing based on property condition. A business with documented maintenance schedules and completed repairs on file receives better renewal rates than one with deferred maintenance and reactive repairs. Carriers track which businesses maintain their properties and which ones defer repairs, and that distinction shows up in your renewal quote.

Bundling Policies Generates Substantial Discounts

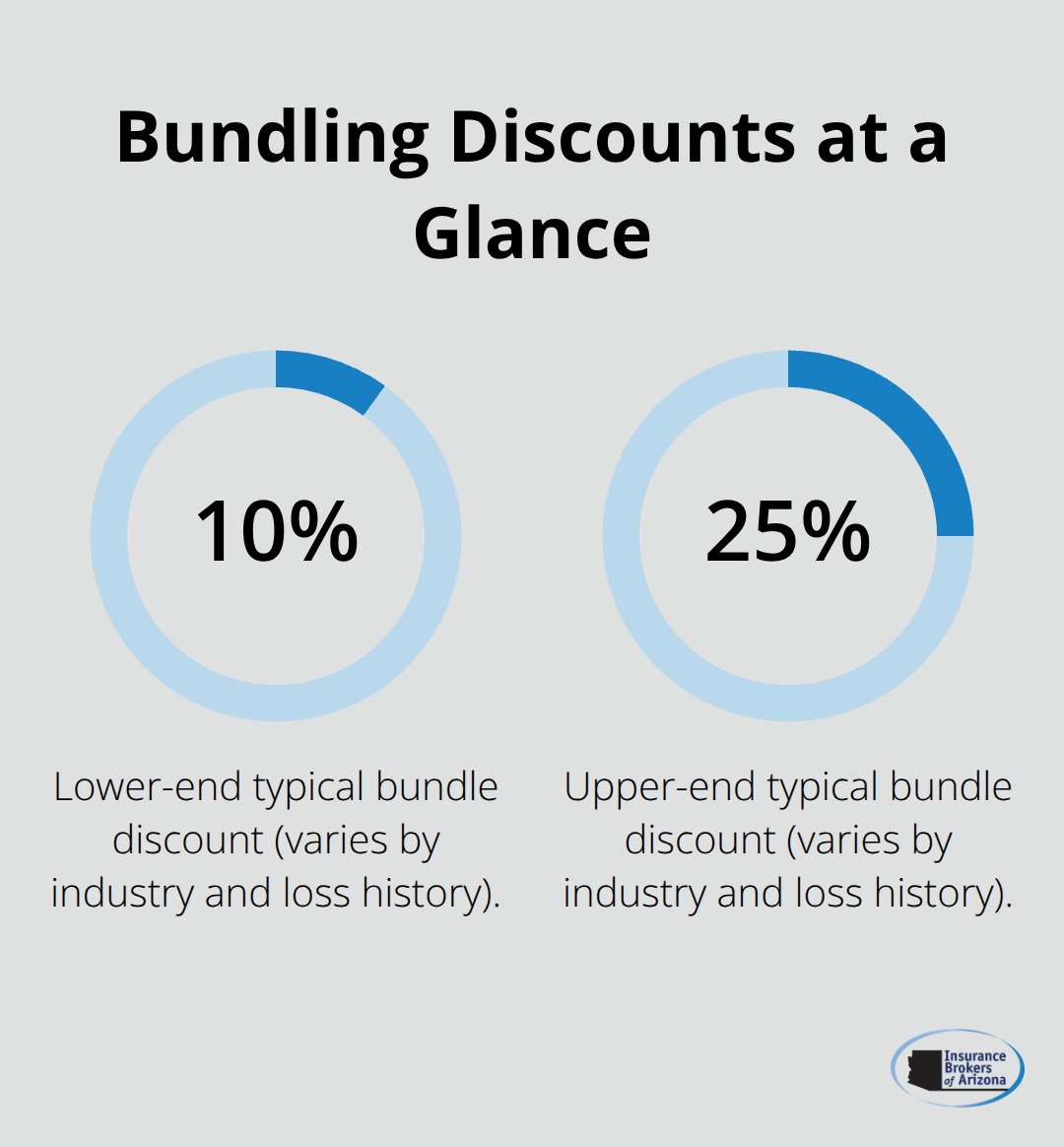

Bundling your commercial property insurance with general liability, commercial auto, and workers compensation under one policy with one carrier typically generates discounts between 10 and 25 percent (depending on your industry and claims history). Progressive reported that in 2023 new customers paid a median of $63 per month for a business owners policy that includes commercial property coverage, and bundled policies consistently outperform single-line coverage on price. A small business bundling property with general liability and commercial auto receives more favorable terms than purchasing each policy separately because the carrier reduces underwriting costs and gains visibility into your complete risk profile. Larger or more complex operations benefit from a customized Commercial Package Policy that bundles multiple coverages into one tailored program, and this approach often produces better pricing than assembling separate policies from different carriers.

Final Thoughts

Your commercial property insurance rates reflect factors you control and factors you cannot change. Location, building construction, and occupancy classification form your baseline premium, but your safety investments, maintenance discipline, and claims history determine whether you pay more or less than that baseline. The businesses that pay the lowest premiums combine accurate property valuations with documented loss prevention and strong maintenance records.

Shopping for commercial property insurance rates without professional guidance leaves money on the table. Carriers price policies differently based on their appetite for specific industries, locations, and risk profiles-one carrier might offer excellent rates for retail operations while another specializes in manufacturing. An independent broker with access to multiple carriers can match your business to the carriers most likely to offer competitive pricing for your specific situation, and we at Insurance Brokers of Arizona® work with over 40 carriers to find options that fit your risk profile and budget.

Getting an accurate quote requires you to provide complete information about your property, operations, claims history, and safety measures. The more detailed your information, the more accurate your quote and the better positioned you are to negotiate. Contact Insurance Brokers of Arizona® to discuss your commercial property insurance needs and find what your business should actually be paying.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.