Finding the Cheapest Home and Auto Insurance Bundle

Home and auto insurance bundles can slash your premiums by 5% to 25% compared to separate policies. Most major carriers offer these multi-policy discounts, but finding the cheapest home and auto insurance requires strategic comparison shopping.

We at Insurance Brokers of Arizona® see clients save hundreds annually by bundling smartly. The key lies in comparing coverage options while maintaining adequate protection levels.

How Bundle Discounts Actually Work

Insurance companies combine your auto and home policies under one carrier to trigger automatic multi-policy discounts. This arrangement benefits insurers because they prefer customers with multiple policies, which reduces their acquisition costs and increases customer retention rates. The discount applies to your base premium before other savings, which makes it a powerful cost-reduction tool.

Real Savings Numbers From Major Carriers

State Farm leads with bundle savings up to $1,356 annually, while American Family offers the highest percentage discount at 40%. Progressive reports average savings of $1,086 for new bundled customers compared to $946 for standalone auto policies. Auto-Owners provides the cheapest bundled rates at $1,878 annually despite offering only 10% discounts.

USAA restricts eligibility to military families but delivers consistent 10% savings. Amica reaches 30% discounts but charges higher base auto rates. These numbers come from NerdWallet analysis of nearly 2 billion rates across all states (covering over 700 insurers).

How Carriers Calculate Your Bundle Discount

Most insurers apply the multi-policy discount to your home insurance premium first, then calculate additional discounts. Some companies like Progressive automatically apply discounts when you add policies, which streamlines the process. The percentage varies based on your coverage limits, deductible amounts, and claim history.

Carriers also factor in your credit score and location when they determine final rates. Higher dwelling coverage amounts typically qualify for larger percentage discounts (up to the carrier’s maximum threshold).

Additional Bundle Benefits Beyond Price

Single deductible policies eliminate confusion when one incident damages both your car and home. Paperless billing discounts stack with bundle savings for additional reductions. Some insurers extend options to RV, boat, and motorcycle coverage for even greater savings.

The simplified claims process through one carrier reduces paperwork and speeds settlements when disasters strike both properties simultaneously. Now that you understand how bundle discounts work, the next step involves smart comparison tactics to find the lowest rates.

How to Compare Bundle Quotes Effectively

Effective bundle comparison requires identical coverage limits across all carriers to avoid misleading price differences. Start with your current coverage amounts as the baseline, then request quotes for $250,000/$500,000/$100,000 auto liability limits and dwelling coverage that matches your home’s replacement cost. Many shoppers accept whatever coverage amounts carriers suggest, which creates apples-to-oranges comparisons that hide true cost differences.

Direct Carrier Websites Deliver Better Results Than Third-Party Tools

Skip insurance comparison websites that collect your information and sell it to multiple carriers. These platforms rarely show actual bundle prices and often display teaser rates that increase during the application process. Visit carrier websites directly or call their customer service lines for accurate bundle quotes instead.

State Farm, Progressive, and Allstate provide instant online quotes that include multi-policy discounts, while USAA requires military verification before it shows rates. This direct approach takes more time but delivers precise prices without unwanted sales calls from multiple agents.

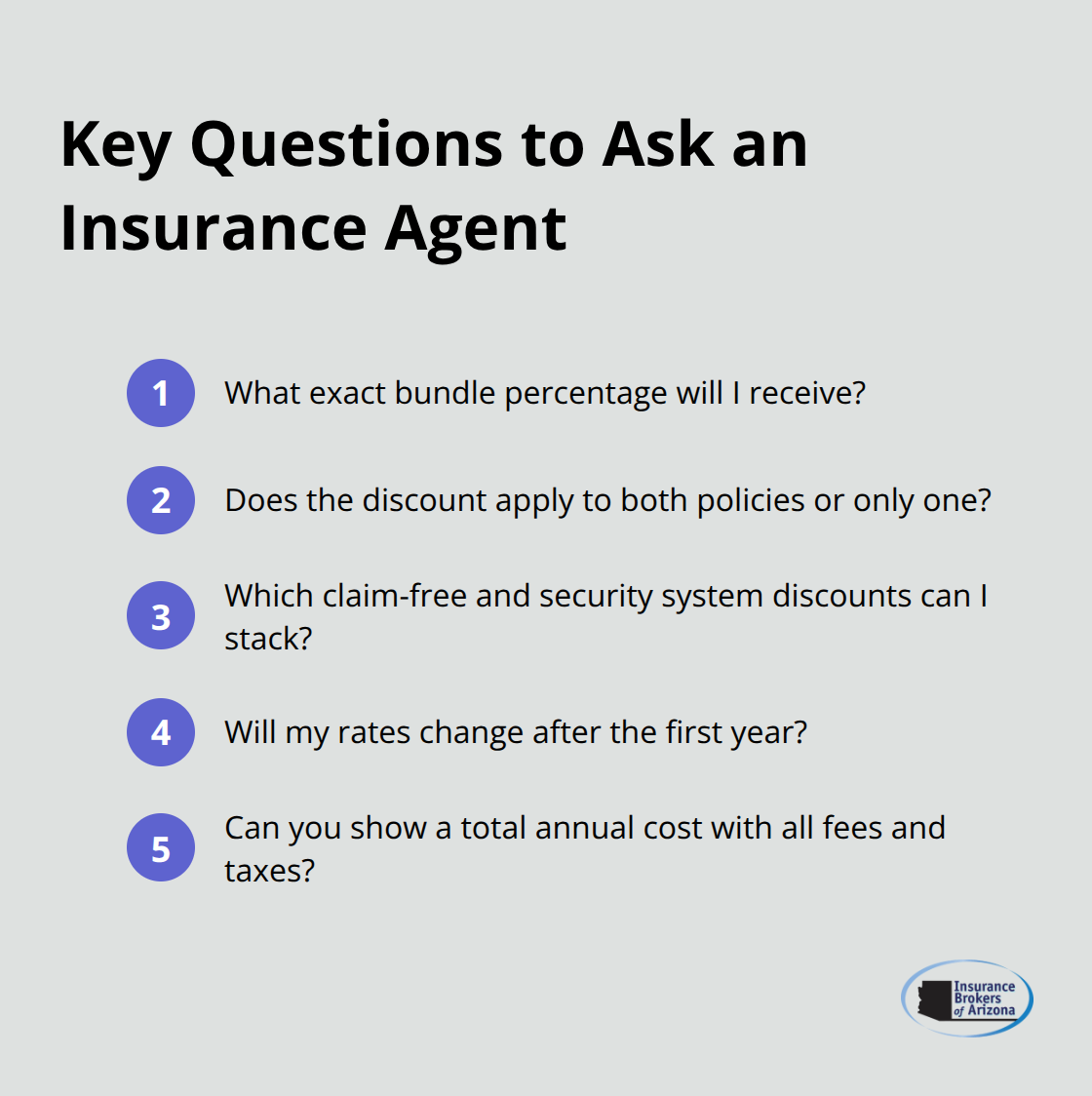

Essential Questions for Agent Consultations

Independent agents can access multiple carriers simultaneously, but you must ask pointed questions to get meaningful comparisons. Request the exact percentage discount for bundling and whether it applies to both policies or just one. Ask about claim-free discounts, security system reductions, and whether rates increase after the first year.

Most importantly, demand to see the total annual cost breakdown that includes all fees and taxes. Agents often emphasize monthly payments that obscure higher annual costs or exclude processing fees (which add $50 to $100 yearly).

Coverage Verification Steps That Matter

Compare identical deductible amounts across all quotes to maintain consistency. Verify that each carrier includes the same optional coverages like rental car reimbursement and roadside assistance. Check whether home policies include replacement cost coverage rather than actual cash value, which can create significant gaps in protection.

Document each carrier’s complaint ratio through the National Association of Insurance Commissioners database. Companies with lower complaint ratios typically provide better claims service when you need it most. These verification steps prevent costly surprises after you purchase coverage and help identify which strategies will reduce your premiums further.

Top Strategies for Lowering Bundle Premiums

Higher deductibles from $500 to $1,000 typically reduce home insurance premiums by 25% and auto premiums by 15% according to the Insurance Information Institute. This strategy works because higher deductibles transfer more risk to you, which insurers reward with lower monthly payments. The math favors this approach if you can afford the higher out-of-pocket costs during claims.

Most homeowners save $200 to $400 annually when they double their deductibles, while auto policyholders reduce premiums by $100 to $300 yearly. The savings compound when you apply higher deductibles to both policies in your bundle.

Security Systems Slash Home Insurance Rates

Monitored burglar alarms reduce home insurance premiums by 5% to 20% with most carriers. Fire detection systems connected to central monitoring stations qualify for additional discounts of 10% to 15%. State Farm and Allstate offer the highest security discounts, while USAA provides smaller reductions but maintains lower base rates.

Anti-theft devices in vehicles generate auto insurance discounts of 5% to 15%, with comprehensive coverage seeing the largest reductions. Modern car alarms and GPS tracking systems qualify for these discounts with most major carriers.

Credit Scores Drive Premium Calculations

Credit scores above 750 unlock the lowest rates from most insurers in states that allow credit-based pricing. Scores below 650 can increase premiums by 50% or more compared to excellent credit customers. This factor affects both home and auto insurance rates significantly.

Paying bills on time and reducing credit card balances improves your insurance rates within 6 to 12 months. The impact varies by state (California, Hawaii, and Massachusetts prohibit credit scoring for auto insurance).

Clean Records Maximize Discounts

Three years without accidents eliminates surcharges completely from most carriers. Single violations can increase rates by 20% to 40% depending on severity and the specific carrier’s guidelines. Traffic tickets affect rates for three to five years, while major violations like DUI impact premiums for up to seven years.

Defensive driving courses reduce auto premiums by 5% to 10% in many states and can help offset recent violations. Some carriers offer accident forgiveness programs that prevent rate increases after your first at-fault claim.

Final Thoughts

The cheapest home and auto insurance bundle demands systematic comparison across multiple carriers with identical coverage limits. Gather quotes from at least three major insurers and verify each quote includes the same deductibles, liability limits, and optional coverages. Document the exact bundle discount percentage and total annual costs (including all fees).

Bundles work best for customers with clean records, good credit scores, and standard coverage needs. Separate policies sometimes cost less than bundles when one carrier excels at auto insurance while another dominates home coverage. Military families should always check USAA first, while customers with recent violations might find better rates through specialized carriers.

We at Insurance Brokers of Arizona® compare bundle options across multiple reputable carriers that individual shoppers cannot access directly. Our partnerships help identify coverage gaps that online tools miss and match your specific needs with competitive options. Insurance Brokers of Arizona® provides personalized service that delivers the most suitable coverage for your situation.