Auto Insurance Without a License: Is It Possible?

Getting auto insurance without a driver’s license might sound impossible, but several legitimate options exist. Many people face this situation due to suspended licenses, medical conditions, or other circumstances.

We at Insurance Brokers of Arizona® help clients navigate these complex insurance scenarios daily. The key lies in understanding which coverage types work for unlicensed drivers and how to structure policies properly.

Auto Insurance Without a License: Legal Requirements and Exceptions

State-by-State Variations in Insurance Laws

Insurance requirements differ dramatically across states, which creates confusion for unlicensed drivers who seek coverage. California requires proof of insurance to register any vehicle, which makes it one of the most accommodating states for unlicensed drivers. Arizona mandates liability coverage but allows foreign licenses and alternative identification for policy applications. Florida permits non-owner policies for unlicensed individuals, while Texas requires at least one licensed driver on standard policies.

Circumstances Where Unlicensed Drivers Need Coverage

Vehicle ownership without driving privileges creates legitimate insurance needs. Parents who purchase cars for teenage children with permits need coverage before the license arrives. Medical conditions that prevent license renewal still require protection for owned vehicles. Suspended license holders must maintain coverage to avoid lapses that increase future premiums by 20-40% (according to insurance industry data). Foreign nationals who live in the US temporarily often own vehicles while they obtain local licenses. Classic car collectors frequently maintain comprehensive coverage on non-driven vehicles to protect against theft and damage.

Legal Penalties for Driving Without Insurance

Driving without insurance carries severe consequences that exceed most policy costs. Arizona fines reach $750 for first offenses, plus license suspension and vehicle impoundment fees that exceed $1,200. California imposes $100-200 base fines that balloon to $500-900 with court costs. Florida charges $150-500 for first violations and doubles penalties for repeat offenses. These penalties make coverage financially smart even for non-driving vehicle owners. SR-22 filing requirements after violations add $25-50 annually to premiums for three years.

These legal complexities highlight why unlicensed drivers need specialized insurance solutions that address their unique circumstances.

How to Get Auto Insurance Without a Valid Driver’s License

Most insurance companies issue policies to unlicensed drivers through three specific approaches that bypass standard license requirements. These methods provide legitimate coverage while addressing the unique challenges unlicensed drivers face.

Named Driver Policies and Excluded Driver Coverage

Named driver policies allow unlicensed vehicle owners to designate a licensed person as the primary driver. This approach shifts risk assessment to that person’s record rather than the unlicensed owner. The unlicensed owner pays premiums but cannot legally drive the vehicle under any circumstances.

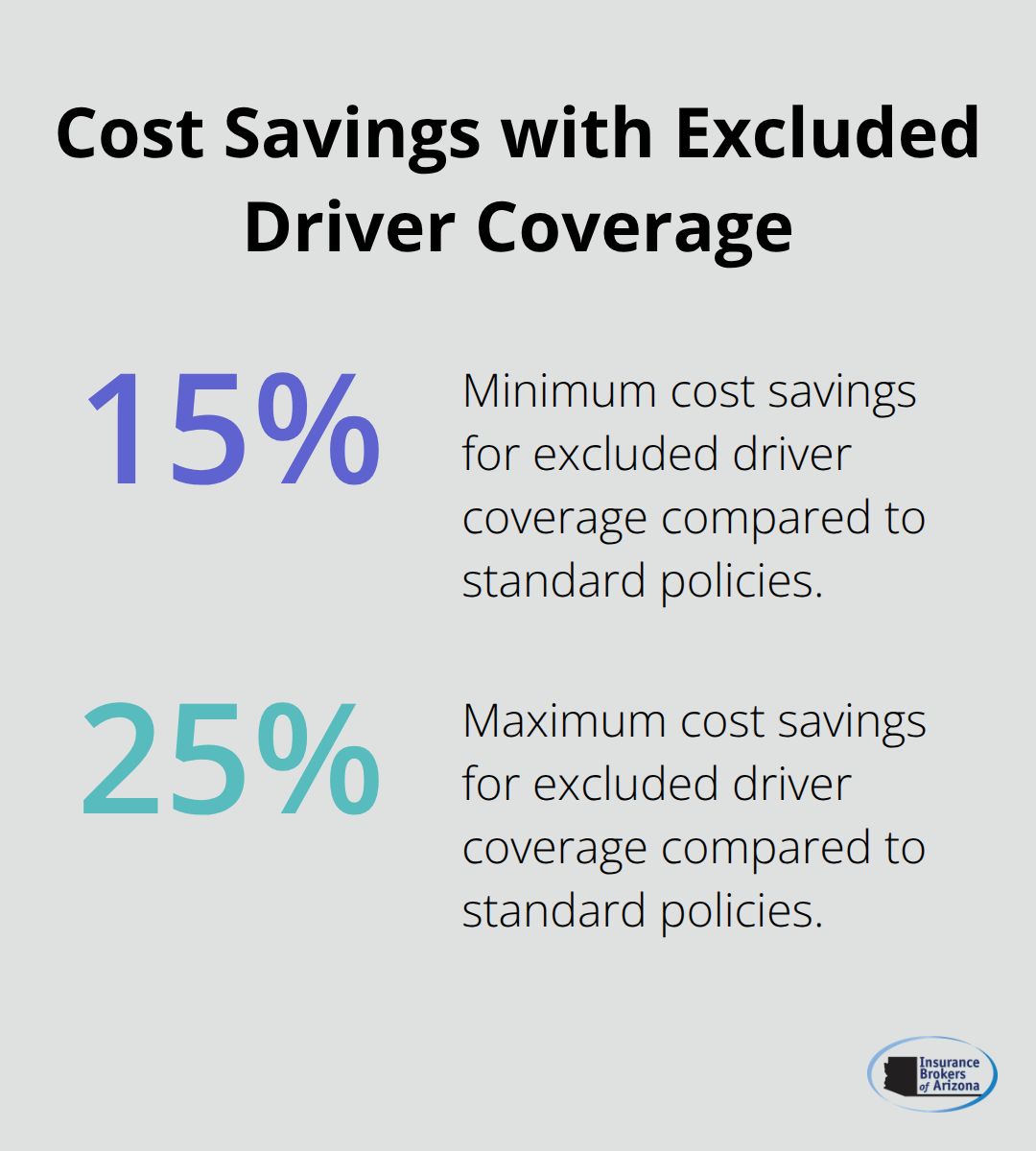

Excluded driver coverage takes the opposite approach. The unlicensed owner maintains the policy but signs exclusion forms that void coverage if they drive. This option costs 15-25% less than standard policies (according to industry data from major carriers like State Farm and Progressive). The savings come from the insurer’s reduced liability exposure.

Parental or Guardian Policy Options

Parents can purchase comprehensive policies for teenage children who hold learner’s permits but lack full licenses. This strategy works well when the teen owns the vehicle but cannot legally drive alone. The parent becomes the primary policyholder while the teen gets listed as an additional driver once licensed.

Insurance companies like USAA report that continuous coverage through this method reduces premiums by 10-15% compared to fresh coverage after license acquisition. The unbroken coverage history demonstrates responsibility to insurers and prevents rate penalties for coverage gaps.

Working with Insurance Agents for Special Situations

Standard online applications reject unlicensed applicants automatically. This makes experienced agents essential for success in these situations. Agents at companies like A-MAX, Kemper, and The Hartford specialize in non-standard policies and maintain relationships with carriers that accept unlicensed drivers.

These professionals structure policies correctly and often secure coverage that online platforms cannot provide. Contact multiple agents because acceptance criteria vary significantly between carriers. Rates can differ by 30-50% for identical coverage depending on the insurer’s risk assessment methods.

These coverage strategies provide the foundation for protection, but unlicensed drivers often need specialized policy types that address specific situations beyond standard auto insurance.

Alternative Coverage Options for Unlicensed Drivers

Non-Owner Car Insurance Policies

Non-owner car insurance provides liability coverage for people who drive occasionally but own no vehicle. This policy type costs 40-60% less than standard coverage according to Progressive data, with annual premiums that range from $200-500 nationwide. The coverage follows you when you drive borrowed or rental cars and fills gaps in the owner’s policy. Arizona residents can purchase non-owner policies through carriers like State Farm and Geico, though applications require phone contact rather than online submission.

This option works perfectly for suspended license holders who need SR-22 certificates while they maintain continuous coverage.

Comprehensive-Only Protection for Parked Vehicles

Storage insurance covers parked vehicles through comprehensive-only policies that exclude liability and collision coverage. This approach reduces premiums by 70-80% compared to full coverage while it protects against theft, vandalism, fire, and weather damage. Classic car owners frequently use this strategy and pay $100-300 annually instead of $1,200-2,000 for full coverage. The policy maintains continuous coverage history and prevents rate increases when you regain your license. Most major insurers offer this option, though you must specify the vehicle remains garaged and undriveable.

SR-22 Requirements for License Reinstatement

SR-22 certificates cost $25-50 annually and prove financial responsibility to state agencies after violations. Arizona requires three years of continuous SR-22 coverage for DUI convictions and major violations. The certificate attaches to any active policy, whether standard auto insurance or non-owner coverage. Lapses in SR-22 coverage restart the three-year requirement and trigger additional license suspension periods. Direct Auto and Acceptance Insurance specialize in SR-22 policies for high-risk drivers and often accept clients that standard carriers reject. The certificate transfers between insurers if you switch companies, but you must maintain unbroken coverage for license reinstatement eligibility.

Final Thoughts

Auto insurance without a driver’s license exists through multiple pathways that address different circumstances. Named driver policies work when someone else operates your vehicle regularly. Excluded driver coverage reduces costs for vehicle owners who never drive, while non-owner policies provide liability protection for occasional drivers without vehicles.

Continuous coverage prevents rate increases that range from 20-40% when you regain your license. Insurance gaps signal risk to carriers and trigger higher premiums that persist for years. Any policy type preserves your coverage history and demonstrates financial responsibility to future insurers.

The path forward depends on your specific situation and needs. Suspended license holders should prioritize SR-22 compliance and continuous coverage, while vehicle owners need comprehensive protection regardless of their status. We at Insurance Brokers of Arizona® help clients find coverage solutions for these unique situations and secure competitive rates through our network of carriers.