What Is Commercial Auto Insurance?

At Insurance Brokers of Arizona®, we often get asked about commercial auto insurance. This type of coverage is essential for businesses that rely on vehicles for their operations.

Let’s explore the commercial auto insurance definition and why it’s a critical component of risk management for many companies.

What Is Commercial Auto Insurance?

Definition and Purpose

Commercial auto insurance is a specialized coverage that protects businesses using vehicles in their operations. This type of insurance provides financial protection for companies in case of accidents, theft, or damage involving their vehicles. It addresses the unique risks associated with using vehicles for business purposes.

Key Differences from Personal Auto Insurance

Commercial auto insurance differs significantly from personal auto policies:

- Higher Liability Limits: Commercial policies offer increased protection, recognizing that business-related accidents can result in more substantial financial consequences.

- Broader Coverage Scope: These policies cover a wider range of scenarios, including employee use of company vehicles and specialized equipment attached to vehicles.

Types of Vehicles Covered

Commercial auto insurance covers a diverse array of vehicles used for business purposes:

- Standard cars and trucks

- Food trucks

- Delivery vans

- Construction equipment

- Box trucks

- Work vans

- Service utility trucks

Industry-Specific Considerations

Different industries have varying needs for commercial auto insurance:

- Trucking companies might require higher liability limits due to increased risks associated with long-haul transportation.

- Local businesses (e.g., florists) might need coverage for small delivery vans.

Insurance providers tailor policies to match the specific requirements of each business sector.

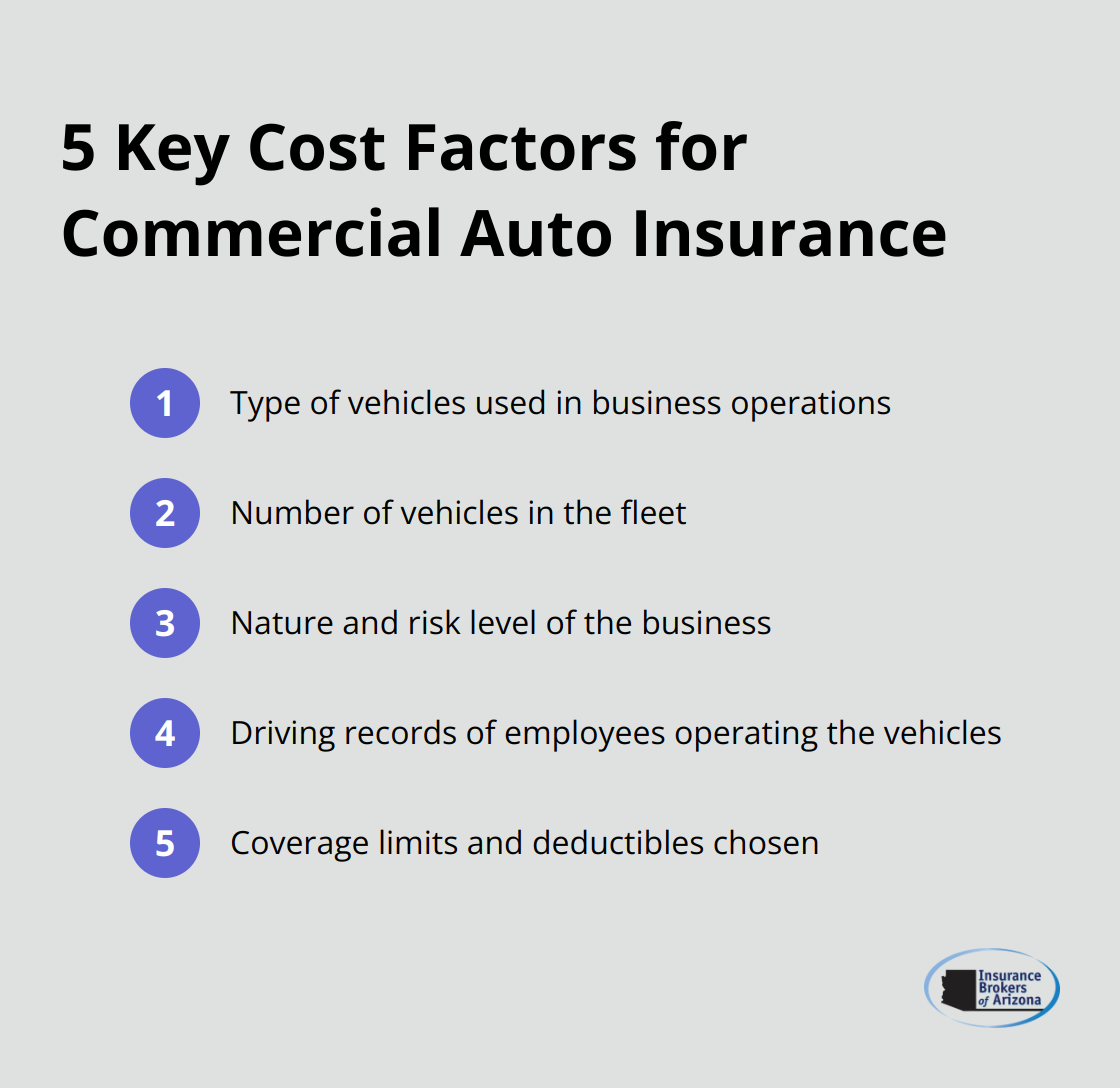

Cost Factors

The cost of commercial auto insurance varies based on several factors:

- Type and number of vehicles

- Nature of the business

- Driving records of employees

Premiums can range from $600 to over $15,000 annually per vehicle. While costs may seem high, investing in adequate coverage is essential for protecting business assets and reputation.

As we move forward, let’s examine the key components that make up a comprehensive commercial auto insurance policy.

What Does Commercial Auto Insurance Cover?

Liability Protection

Commercial auto insurance provides essential liability coverage for businesses. This protection shields your company if one of your vehicles causes injury to others or damages their property. In 2024, property damage claims averaged $16,000, while bodily injury claims reached $58,000. These figures highlight the need for adequate coverage.

Vehicle Protection

Your policy should protect your business vehicles. Collision coverage pays for damage to your vehicle in an accident, regardless of fault. Comprehensive coverage protects against non-collision incidents like theft, vandalism, or natural disasters. The average comprehensive claim in 2024 was $1,800, illustrating potential out-of-pocket costs without this coverage.

Uninsured Motorist Protection

About 12% of drivers in Arizona lack insurance. Uninsured/underinsured motorist coverage protects your business if one of these drivers hits your vehicle. This coverage proves valuable, as the average cost of an uninsured motorist claim in 2024 reached $28,000.

Medical Coverage

Medical payments or personal injury protection (PIP) coverage helps pay for medical expenses resulting from an accident, regardless of fault. This can be particularly valuable in states with no-fault insurance laws. In 2024, the average PIP claim amounted to $5,000.

Tailored Coverage Options

When selecting coverage, consider your business’s specific needs. A landscaping company with a fleet of trucks will have different requirements than a real estate agency with a single company car. Insurance providers (like Insurance Brokers of Arizona®) specialize in customizing policies to match unique risk profiles.

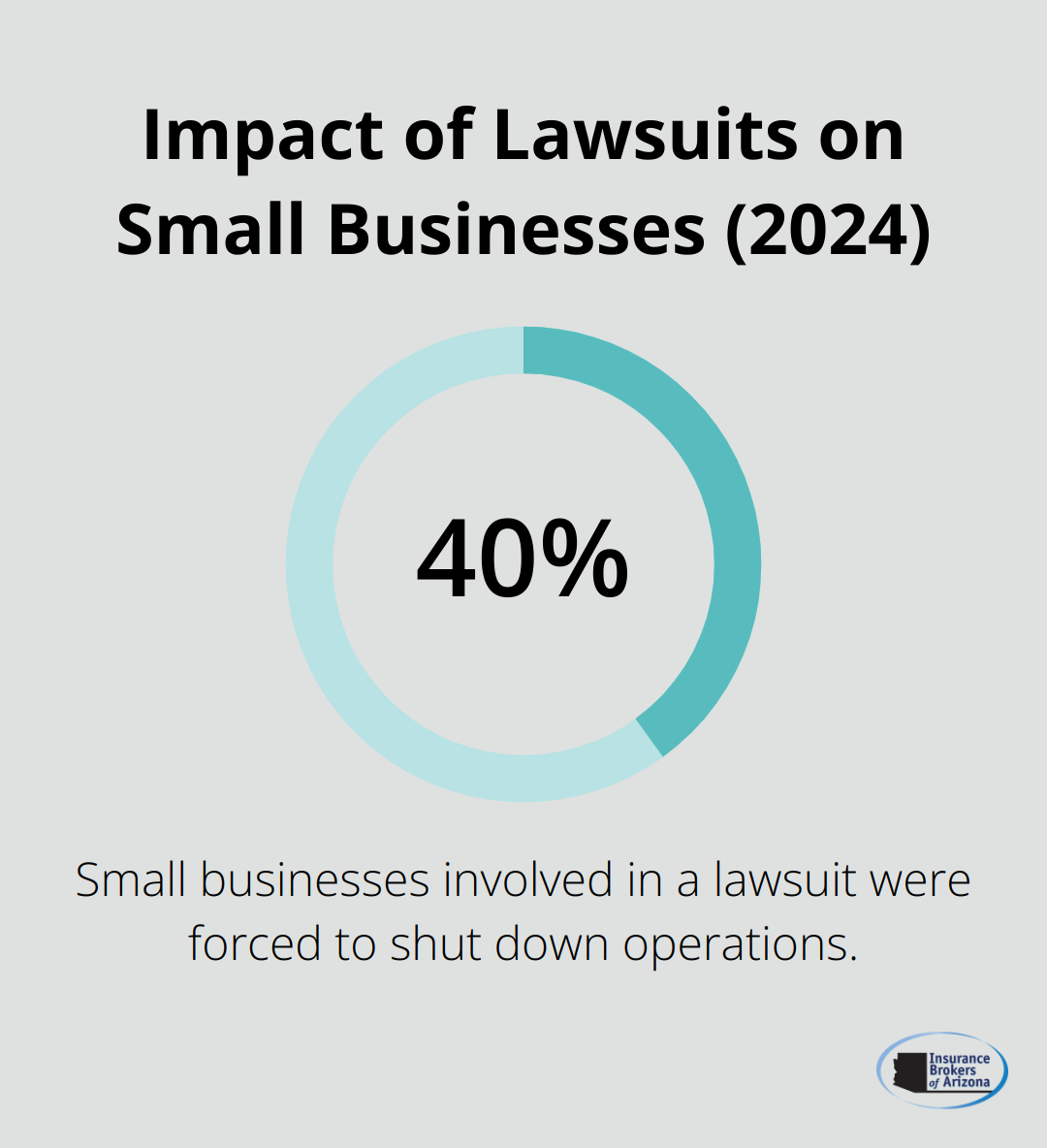

Proper commercial auto insurance can make the difference between surviving a financial setback and closing your doors. In 2024, 40% of small businesses involved in a lawsuit were forced to shut down operations.

Now that we’ve covered the main components of commercial auto insurance, let’s explore who needs this vital coverage and why it’s so important for certain industries.

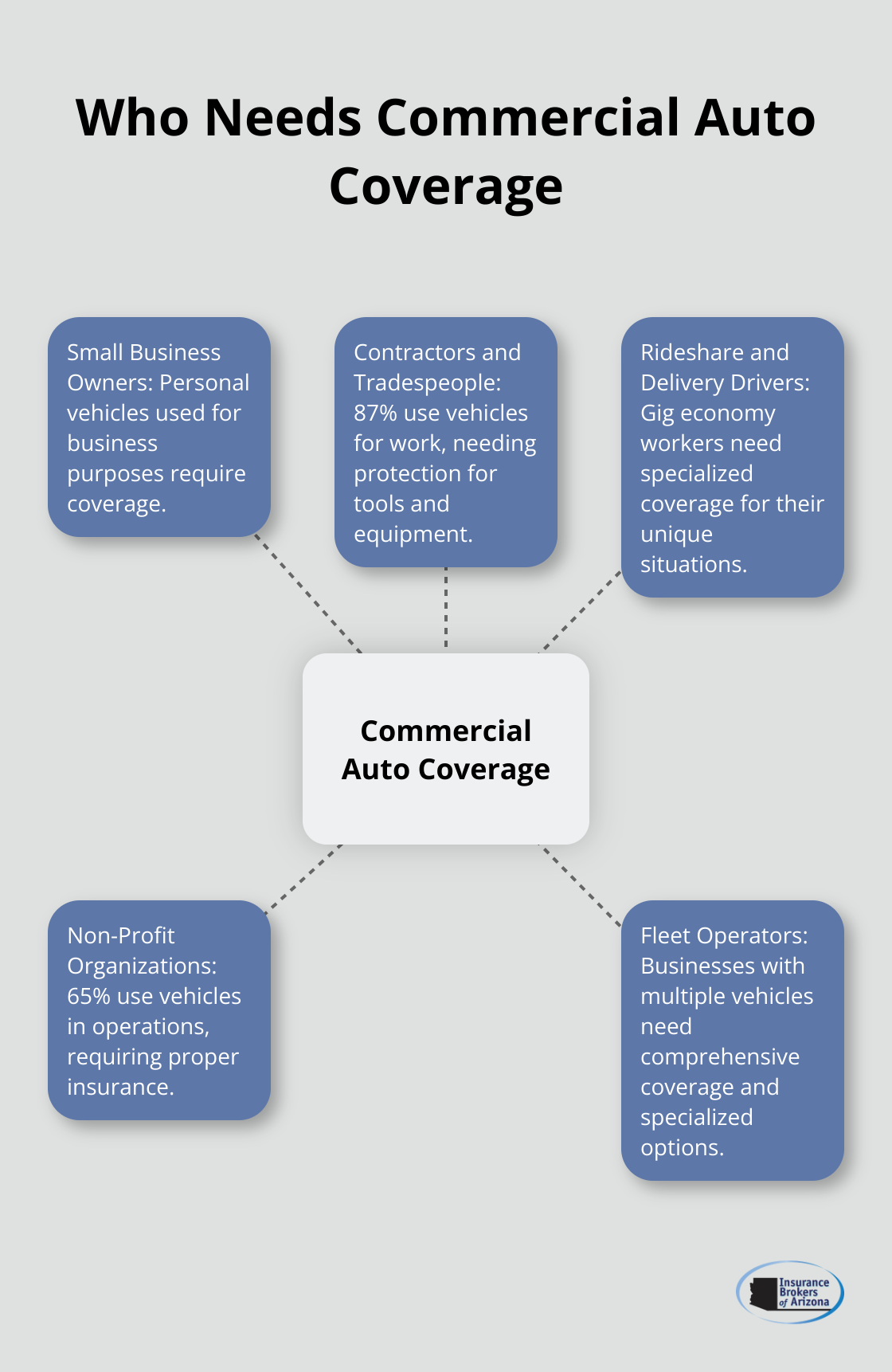

Who Needs Commercial Auto Coverage

Small Business Owners

Many small business owners don’t realize they need commercial auto insurance. If you use your personal vehicle for business, your personal auto policy might not cover you in an accident. This leaves you exposed to financial risk. A local florist who makes deliveries in their personal van should have commercial auto insurance to protect against potential liabilities.

Contractors and Tradespeople

Contractors and tradespeople often transport tools, equipment, and materials to job sites. These professionals need commercial auto insurance to cover their vehicles and valuable items. A survey by the National Association of Home Builders found that 87% of contractors use their vehicles for work purposes (highlighting the widespread need for this coverage in the construction industry).

Rideshare and Delivery Drivers

The gig economy has created a new category of workers who need commercial auto insurance. Rideshare drivers (for companies like Uber and Lyft) and food delivery drivers (for services like DoorDash and Grubhub) often fall into a coverage gap between personal and commercial auto insurance. Some insurance companies offer hybrid policies to address this specific need, but these drivers must understand their coverage requirements.

Non-Profit Organizations

Non-profit organizations that use vehicles for their operations also need commercial auto insurance. This includes organizations that transport clients, deliver goods, or use vehicles for fundraising events. A study by the National Center for Charitable Statistics found that 65% of non-profits use vehicles in their operations, which underscores the importance of proper coverage in this sector.

Fleet Operators

Businesses with multiple vehicles, from small local companies to large corporations, need comprehensive commercial auto insurance. Fleet operators face unique risks and require specialized coverage options. These can include fleet tracking systems, driver safety programs, and tailored liability limits based on the size and type of vehicles in the fleet.

Final Thoughts

Commercial auto insurance protects businesses that rely on vehicles. This specialized coverage shields against risks such as accidents, property damage, and medical expenses. The commercial auto insurance definition encompasses a wide range of factors, including industry-specific needs, vehicle types, and operational scope.

We at Insurance Brokers of Arizona® tailor commercial auto insurance policies to meet the specific needs of businesses across various industries. Our partnerships with over 40 carriers allow us to offer competitive options for our clients. We focus on understanding your business and crafting a policy that provides comprehensive protection.

To evaluate your commercial auto insurance needs, assess your vehicle usage, potential risks, and current coverage gaps. Consider the types of vehicles you operate, your business activities, and your employees’ driving records. This information will prepare you to discuss your needs with an insurance professional and secure the right coverage for your business.