Average General Liability Insurance Cost: A Complete Guide

General liability insurance is a cornerstone of business protection, but understanding its costs can be challenging. At Insurance Brokers of Arizona®, we often field questions about the average general liability insurance cost for different industries and business types.

This comprehensive guide will break down the factors influencing these costs and provide practical insights to help you manage your premiums effectively.

What Drives General Liability Insurance Costs?

General liability insurance costs vary widely depending on several key factors. Let’s explore the main drivers of general liability insurance costs to help you better understand and manage your coverage expenses.

Business Size and Revenue

The size of your business and its annual revenue significantly impact your general liability insurance costs. Larger companies with higher revenues typically face higher premiums due to increased exposure to potential claims. A small local shop with annual revenue of $100,000 might pay around $500 per year for general liability insurance, while a medium-sized business with $1 million in revenue could see premiums closer to $2,000 annually.

Industry and Risk Level

Your industry and associated risk level heavily influence your insurance costs. High-risk industries like construction or manufacturing often face higher premiums due to the increased likelihood of accidents or injuries at job sites. A construction company might pay $3,000 to $5,000 annually for general liability insurance, while a low-risk business (such as a consulting firm) might only pay $500 to $1,000 per year.

Coverage Limits and Deductibles

The coverage limits you choose and your policy’s deductible directly affect your premiums. Higher coverage limits provide more protection but come with higher costs. Similarly, opting for a higher deductible can lower your premiums but increases your out-of-pocket expenses in the event of a claim. Increasing your coverage limit from $1 million to $2 million might raise your annual premium by $200 to $500, depending on other factors.

Location and Claims History

Your business location and claims history also impact your insurance costs. Businesses in urban areas or regions prone to natural disasters often face higher premiums due to increased risk exposure. Additionally, a history of claims can significantly raise your insurance costs. A business with no prior claims might pay 20% to 30% less for coverage compared to a similar business with multiple recent claims.

Understanding these factors can help you make informed decisions about your general liability insurance coverage. Insurance professionals can assess your specific risk factors and find the most cost-effective coverage options. A careful consideration of these elements can help you secure the right coverage at the best possible rate for your business.

Now that we’ve covered the main factors affecting general liability insurance costs, let’s take a closer look at how these costs vary across different industries.

How Much Does General Liability Insurance Cost Across Industries?

General liability insurance costs vary significantly across different industries due to their unique risk profiles. This chapter explores the average costs for key sectors to provide a better understanding of what you might expect to pay.

Construction and Contracting

The construction industry faces some of the highest general liability insurance costs due to the inherent risks involved in their work. Construction companies pay an average of $1,700 annually for general liability coverage. However, this can range from $800 to $3,000 depending on the specific type of contracting work.

A residential remodeling contractor might pay less than a commercial high-rise builder due to the difference in project scale and associated risks. Roofing contractors often face even higher premiums (sometimes exceeding $5,000 annually) due to the high risk of falls and property damage.

Industry data shows the average general liability claim for small businesses is around $75,000, a sum that could devastate a business without proper coverage.

Retail and E-commerce

Retail businesses, both brick-and-mortar and e-commerce, generally face lower risks compared to construction, which reflects in their insurance costs. The average annual premium for retailers is approximately $700. However, this varies based on factors such as store size, foot traffic, and product type.

A small boutique clothing store might pay as little as $400 per year, while a large electronics retailer with multiple locations could pay upwards of $1,500 annually. E-commerce businesses often enjoy lower premiums (averaging around $500 per year) due to reduced risks associated with physical storefronts.

Professional Services

Professional service providers, such as consultants, accountants, and marketing agencies, typically benefit from some of the lowest general liability insurance rates. The average annual premium for these businesses ranges from $500 to $800.

This lower cost primarily results from the reduced risk of physical injury or property damage in office-based work environments. However, professional services often require additional coverage, such as professional liability insurance, which can increase overall insurance costs.

Hospitality and Food Service

Restaurants, bars, and hotels face higher-than-average general liability insurance costs due to frequent customer interaction and the potential for food-related illnesses. The average annual premium for businesses in this sector ranges from $1,000 to $2,000.

A small café might pay on the lower end of this range, while a large restaurant with a bar could see premiums closer to $3,000 or more. Factors such as alcohol sales, delivery services, and live entertainment can significantly impact insurance costs in this industry.

These industry averages serve as starting points, but every business is unique. Your specific circumstances will ultimately determine your insurance costs. The next chapter will explore effective strategies to lower your general liability insurance premiums, helping you find the most cost-effective coverage for your business.

How to Reduce Your General Liability Insurance Costs

General liability insurance is a necessary expense for businesses, but you can take steps to lower your premiums. Here are some effective strategies to consider:

Implement a Comprehensive Risk Management Plan

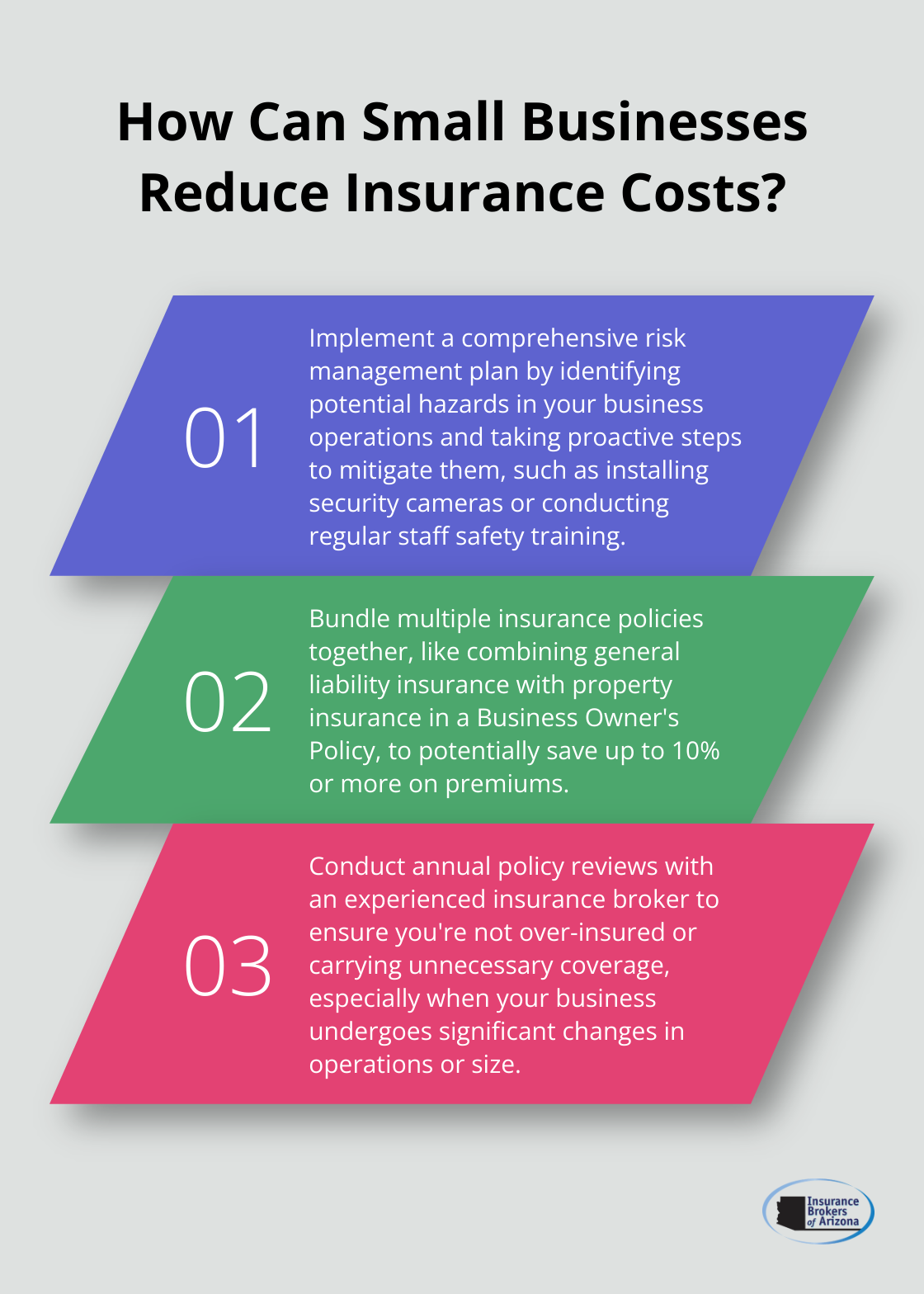

One of the most impactful ways to lower your general liability insurance costs is to implement a robust risk management plan. This involves identifying potential hazards in your business operations and taking proactive steps to mitigate them. For example, a retail store could install security cameras and implement regular staff training on customer safety, potentially reducing the likelihood of slip-and-fall accidents or theft incidents.

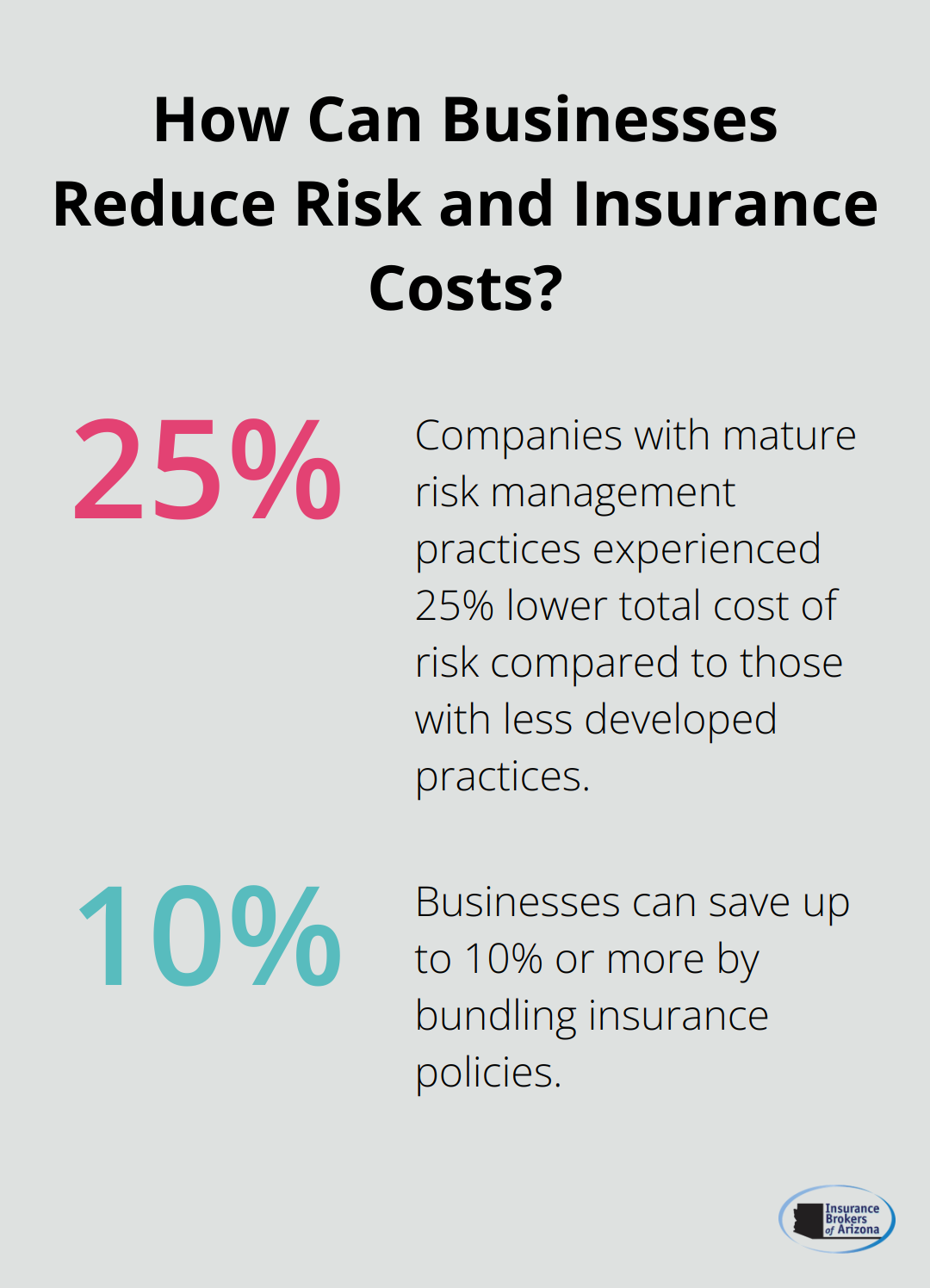

A study by the Risk Management Society (RIMS) found that companies with mature risk management practices experienced 25% lower total cost of risk compared to those with less developed practices. This reduction in risk directly translates to lower insurance premiums.

Consider Policy Bundling

Many insurance providers offer discounts when you bundle multiple policies together. For instance, combining your general liability insurance with property insurance in a Business Owner’s Policy (BOP) can lead to significant savings. According to the Insurance Information Institute, businesses can save up to 10% or more by bundling policies.

Adjust Your Deductible

Opting for a higher deductible can substantially lower your premium costs. For example, increasing your deductible from $500 to $1,000 could potentially reduce your annual premium by 10-20%. However, it’s important to ensure that you can comfortably afford the higher out-of-pocket expense in the event of a claim.

Conduct Regular Policy Reviews

Insurance needs change as your business evolves. Regular policy reviews ensure that you’re not over-insured or carrying unnecessary coverage. For instance, a company that has shifted from in-person to primarily online operations might be able to reduce certain aspects of their liability coverage.

The Insurance Information Institute recommends reviewing your policy at least once a year (or whenever your business undergoes significant changes). During these reviews, it’s beneficial to work with an experienced insurance broker who can identify potential areas for cost savings without leaving you underinsured.

Work with an Experienced Insurance Broker

An experienced insurance broker can help you navigate the complex world of insurance and find the most cost-effective solution for your specific business needs. They can help you understand your coverage options, identify potential risks, and negotiate with insurance providers on your behalf.

Insurance Brokers of Arizona®, for example, offers personalized insurance products and works with over 40 reputable carriers to provide competitive options for businesses. Their focus on tailoring coverage to specific needs and securing the best rates can help you find the right balance between cost and coverage.

Final Thoughts

Understanding the average general liability insurance cost helps businesses make informed decisions about their coverage. Numerous factors influence these costs, including business size, revenue, industry risk, and location. Tailored coverage proves essential, as every business faces unique risks and needs.

An experienced insurance broker can provide significant benefits when navigating general liability insurance complexities. Insurance Brokers of Arizona® offers personalized insurance products and partners with reputable carriers to find competitive options. Our focus on customer service and securing the best rates can help you balance comprehensive coverage and cost-effectiveness.

The right general liability insurance policy protects your business from potentially devastating financial losses. It provides peace of mind, allowing you to focus on growing your business with confidence. Consider partnering with a trusted insurance professional who can guide you through finding and maintaining suitable, cost-effective coverage for your unique business needs.